Introduction

2022 will be remembered as one of cryptocurrency’s defining moments. Its exuberance reached an all-time high after an impeccable 2021 market performance. At every turn, digital asset influencers were shilling the next big thing. Celebrities were acting like real-money managers, with Kim Kardashian getting fined for misleading the public. One of my favorite quotes from 2017 is, “When your cab driver starts talking about Bitcoin (BTC), it is time to sell.” Though the poor performance of crypto in 2022 is not solely attributed to market mania, greed had a huge role to play.

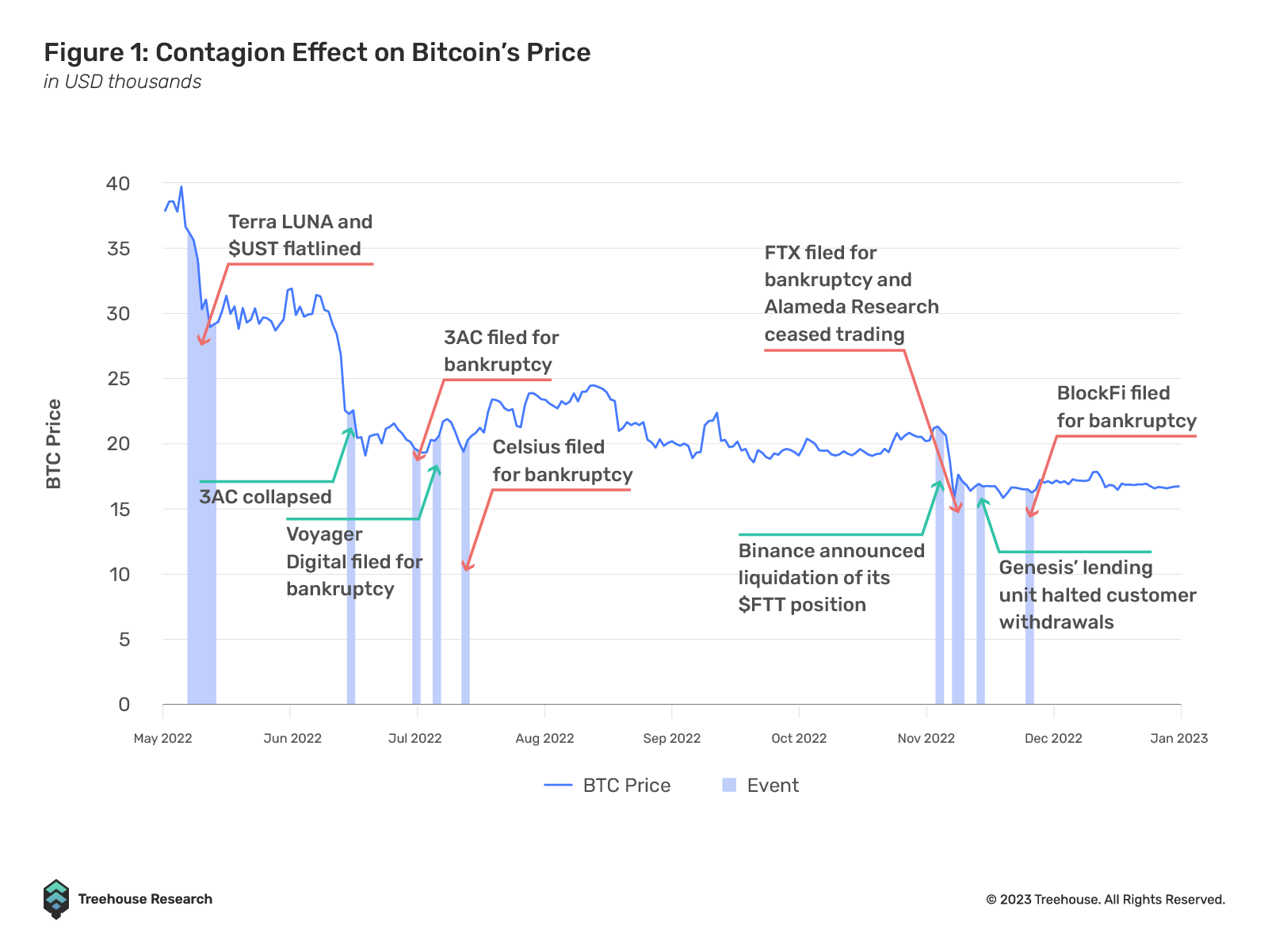

The biggest story in 2022 for crypto has to be the collapse of the most prominent players and the countless resulting casualties. These collapses, each regarded as a black swan event, have become a recurring theme in crypto, with many fearing how deep the contagion effect has spread. Contagion was one of the main themes in 2022, as each collapse sparked a domino effect that led to where we are today.

Collapses, Crashes, and Contagion

UST and LUNA’s Crash: The Beginning of the End

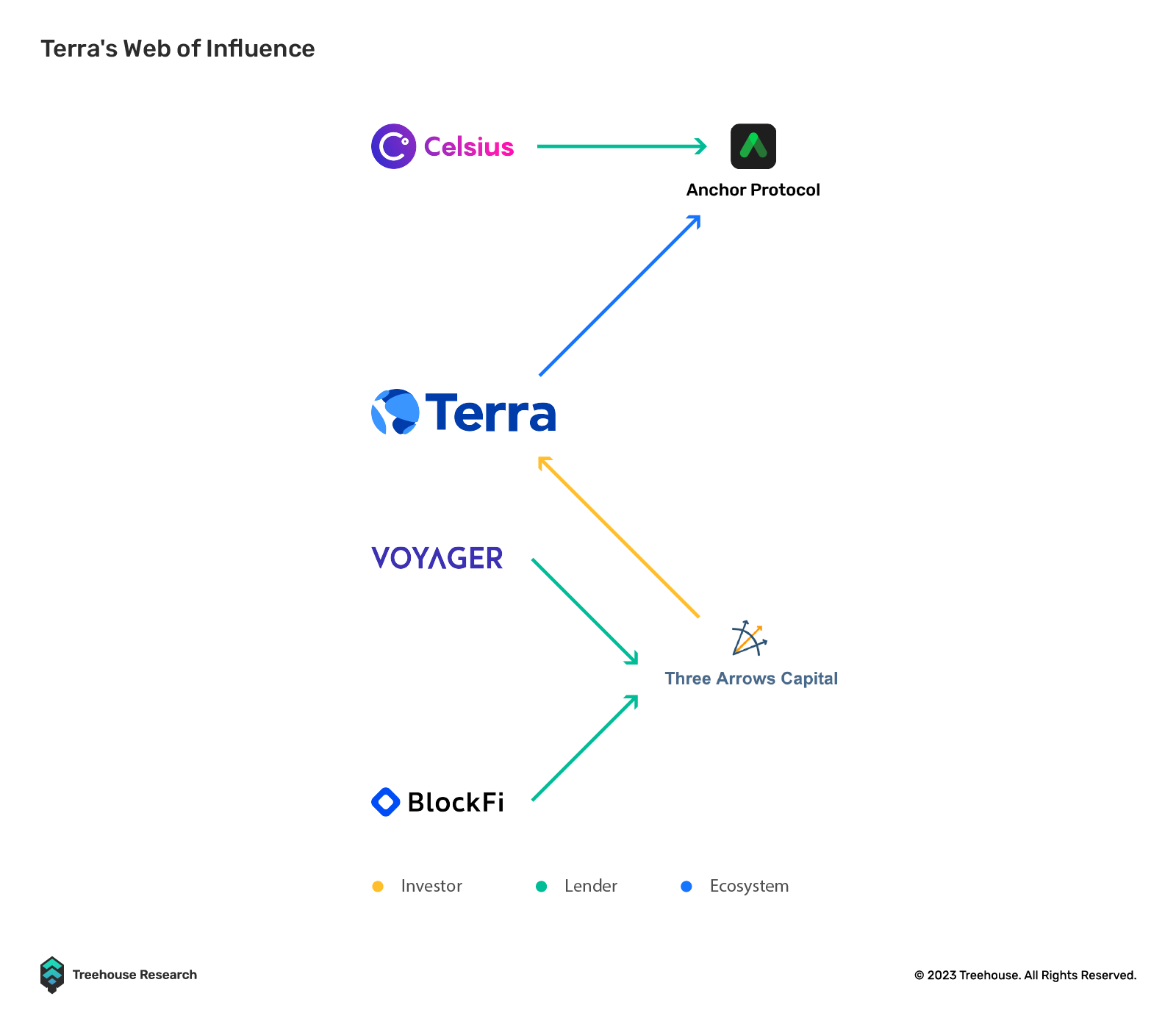

LUNA was one of the brightest stars in 2021. The team had created an algorithmic stablecoin, UST, pegged to the US dollar. Unlike USDT, USDC, or DAI, UST was capital efficient and free from centralization. However, it had one major flaw: its design meant that the stablecoin was susceptible to a death spiral in the event of a bank run. This was exactly what happened.

On 7 May 2022, the Terra team withdrew a large amount of UST from a trading pool on Curve Finance. The moment they made that withdrawal, an unknown whale sold US$85M UST for US$85M USDC on Curve Finance, pushing UST slightly below its peg. Before this, the crypto market had already been dropping due to risk-off sentiments. Individuals and institutions with UST exposure also pulled their assets out of Anchor Protocol when UST started losing its peg. US$9B of the US$14B UST on Anchor was withdrawn within 48 hours of UST losing its peg, causing UST to significantly lose its peg.

Read more about the UST depeg here.

On 13 May 2022, both LUNA and UST flatlined, leading to an accumulative loss of US$40B. Terra’s downfall kickstarted a wave of contagion that left many in its wake. We just did not know it then.

Three Arrows Capital’s (3AC’s) Collapse

Like Terraform Labs, 3AC was also widely known in the crypto space. Back in March 2022, the fund managed north of US$10B in assets. Unfortunately, the firm made huge losses on its leveraged bets and defaulted about US$3.5B worth of loans to various creditors.

The firm had accumulated a significant number of GBTC shares and borrowed more capital after GBTC’s premium evaporated. The founders used their reputation within the crypto space to borrow funds from various centralized lenders on an undercollateralized basis.

On 15 June 2022, BlockFi liquidated 3AC’s margin loans, leading to the collapse of 3AC. 3AC could not pay off its margin loans and had used borrowed funds to invest in risky assets such as LUNA, which crashed to $0. As a result, 3AC filed for Chapter 15 bankruptcy.

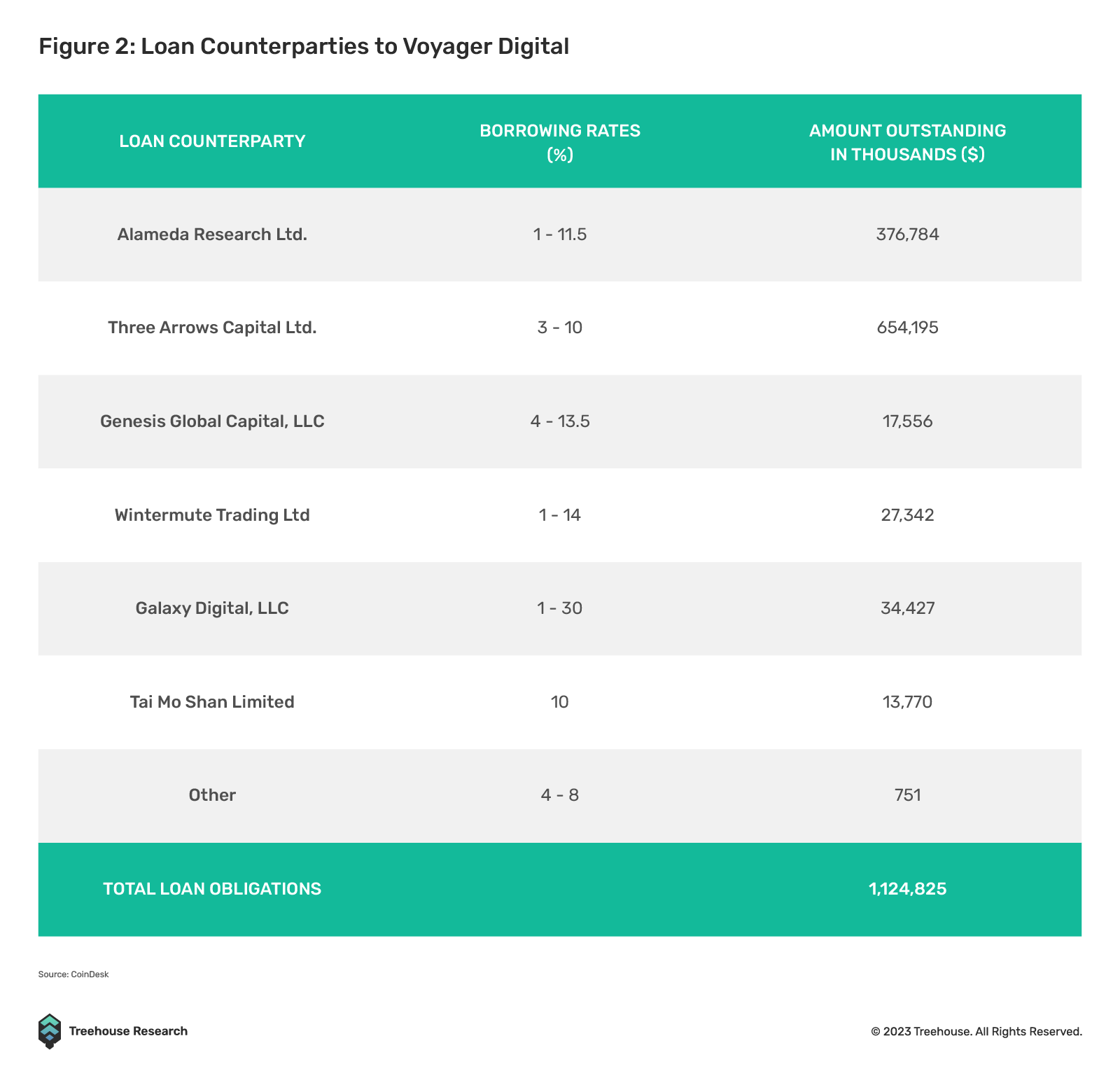

Voyager Digital

With the collapse of 3AC, Voyager was also impacted. In late June, Voyager made multiple demands for repayment from 3AC but did not receive an answer. On 12 June 2022, Celsius, another crypto lender, froze customer withdrawals. As a result, Voyager received an “influx of customer withdrawals”. On 23 June 2022, Voyager lowered daily withdrawal limits from US$23K to US$10K, and on 1 July 2022, it froze all customer withdrawals. On 6 July 2022, Voyager filed for Chapter 11 bankruptcy.

Initially, FTX U.S. won the bid to acquire Voyager for US$1.4B in a US bankruptcy auction. However, after FTX declared bankruptcy, Binance U.S. won the bid to acquire Voyager for US$1.022B.

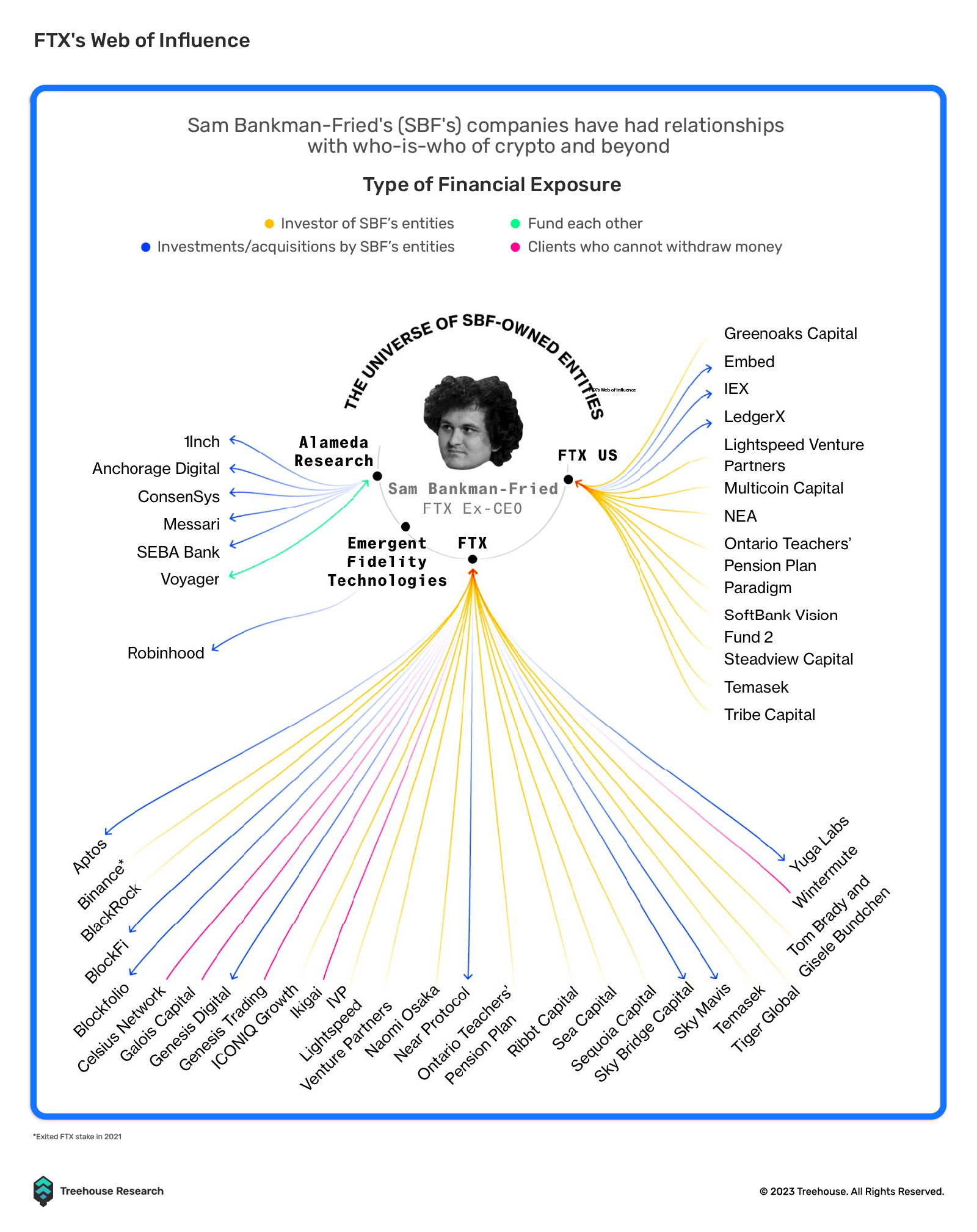

FTX

Perhaps the most surprising of all, FTX was also not spared by the downturn in crypto markets. The fall of FTX quickly unfolded over eight days in November 2022. The trigger was a CoinDesk report on 2 November 2022 that quickly led to a dispute with Changpeng Zhao, Binance’s CEO.

On 6 November 2022, Binance, the world’s largest centralized crypto exchange, stated that it would liquidate its entire investment in FTT tokens—roughly 23M FTT tokens worth US$529M, leaving Alameda’s solvency in question. Despite Sam Bankman-Fried’s reassurances, FTX faced liquidity issues after customers withdrew US$6B from the exchange to be safe. Their fears materialized as FTX soon halted withdrawals. On 8 November 2022, Binance stated that it had signed a non-binding letter of intent (LOI) to acquire FTX (not including FTX U.S.) for an undisclosed price.

The prospect of rescue was short-lived as Binance pulled out of the transaction the next day. The exchange said on 9 November 2022 that it decided to terminate the FTX acquisition after corporate due diligence uncovered concerns regarding the mismanagement of client assets, among other problems.

FTX filed for Chapter 11 bankruptcy protection the following day, indicating that around 130 of its connected entities were also involved in the process. According to the bankruptcy documents, FTX had both assets and liabilities in the US$10B to US$50B range.

The Year Ahead

The events of 2022 left the industry with valuable lessons and solidified the importance of decentralized systems. As the new year begins, Treehouse Research would like to share our outlook for the year in the traditional finance (TradFi) and crypto space.

US Inflation, Recession Hide-And-Seek, the Fed and What They Mean for the Markets

1. US inflation might have peaked but could remain sticky

US Consumer Price Index (CPI) had shot to its highest in 40 years before abating from an intra-year high. The real concern, however, lies with how long inflation will remain above the Fed’s target. While the reopening of China might fill the gaps in supply chains and global productivity, a new norm of the labor market driven by COVID-19’s legacy of remote working and deglobalization means labor shortage is likely to stay. For example, US manufacturers struggle to find sufficient trained and skilled local workers without paying higher costs than those paid to Chinese workers. On the other hand, the Biden government’s environmental, social, and governance (ESG) policies prevent farmers from using synthetic fertilizers, exerting a further toll on the global food supply which is already made fragile by the Ukraine war.

2. The Fed’s path is a tale between officials’ words and the market’s pricing

Fed Funds futures are currently pricing in zero easing until July with negligible probability of cutting rates for the rest of 2023 until the Federal Open Market Committee’s (FOMC’s) December meeting, which has ~10.6% implied probability of a rate cut. The market is essentially pricing in the Fed’s swift action after a recession hits within the first half of this year, which could be a key mispricing as officials might be willing to let the economy slow down longer than expected to squeeze out sticky inflationary pressures.

3. Growth outlook is key to market sequencing this year

A US recession is almost entirely priced in by the US Treasury Yield Curve, as the 3M/10Y yield curve and near-term forward spread (3M spot yield versus 18M forward 3M yield) both joined negative territory following the 2s10s inversion. 3M/10Y yield curve is used in New York Fed’s recession probability model, while the near-term forward spread is quoted by Powell as the Fed’s choice of recession risk measure.

Growth trajectory out of the US recession, both US domestically and internationally, matters to how global assets perform. The sequencing of asset bottoming and rebounding usually starts with US rates, which already saw a 10-year benchmark yield down by 50bps since November-wide, followed by EM rates, SPX, cyclical, and HY credit. As USD strength has consolidated, risky assets are now reassessing their risk premiums and will likely respect the usual route of performance rotation.

Geopolitics, Wars, US-China Decoupling, and Asia’s Own Problem

1. Russia-Ukraine war lingers

The Russian invasion revitalized an increasingly centrifugal North Atlantic Treaty Organization (NATO) and intensified geopolitical rifts between circles of friends. A prolonged war between two main agricultural and energy producers not only feeds down inflationary pressure, but also forces everyone else to take a side, speeding up deglobalization.

2. US and its allies step up containment on China, which needs to find a new breakout

The US is leading its allies to contain China’s access to “hard technology”—chip-making machinery, industry design software, and talent access to US education in sensitive fields of studies. Meanwhile, Chinese consumer product companies will likely survive as US investors also benefit from the tremendous consumer market in China – think Alibaba, Tencent, Tiktok, and so on.

One potential Chinese breakout from US containment is crypto. After the miner purge and crypto trading ban in mainland China, more clues are indicating that the country is experimenting with opening up its mass retail markets to crypto via Hong Kong SAR. New retail exchange licensing schemes, crypto futures-linked ETFs, and a proactive regulator, all suggest Hong Kong and China might step up their reach in the retail crypto trading business.

3. Opportunities in other emerging markets (EM) countries

Supply chain diversification benefits up-and-coming EM countries with an ample young population. With more jobs coming from China to these countries, the young generation can get upskilled and earn more, which leads to untapped retail potential in both consumption and investment. Crypto assets could be on top of the new traders’ lists due to their low entry barrier compared to TradFi assets.

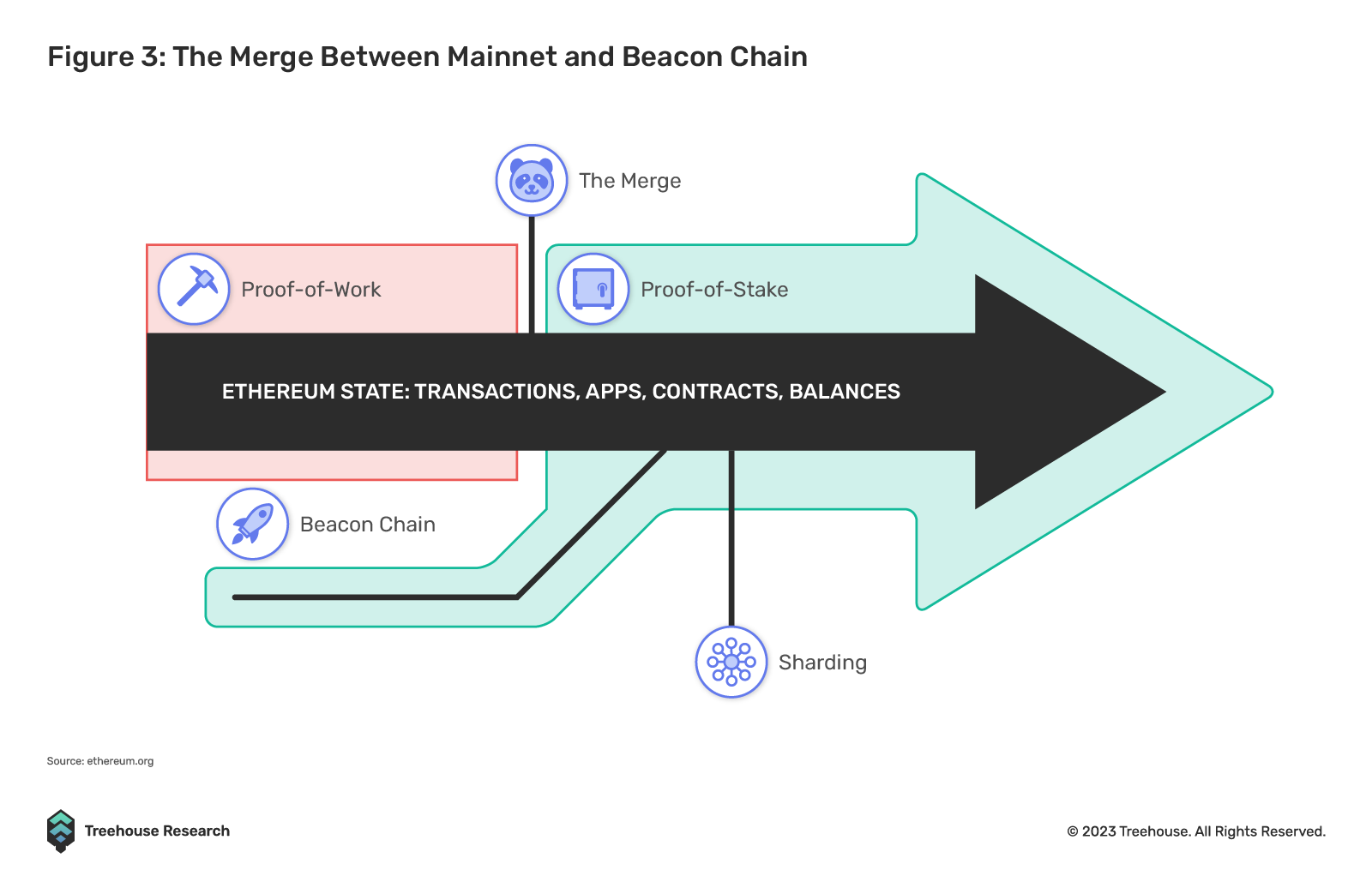

After The Merge

The widely anticipated Merge finally took place on 15 September 2022. It was one of the most monumental achievements in crypto history as Ethereum transited from Proof-of-Work (PoW) to Proof-of-Stake (PoS) consensus mechanism.

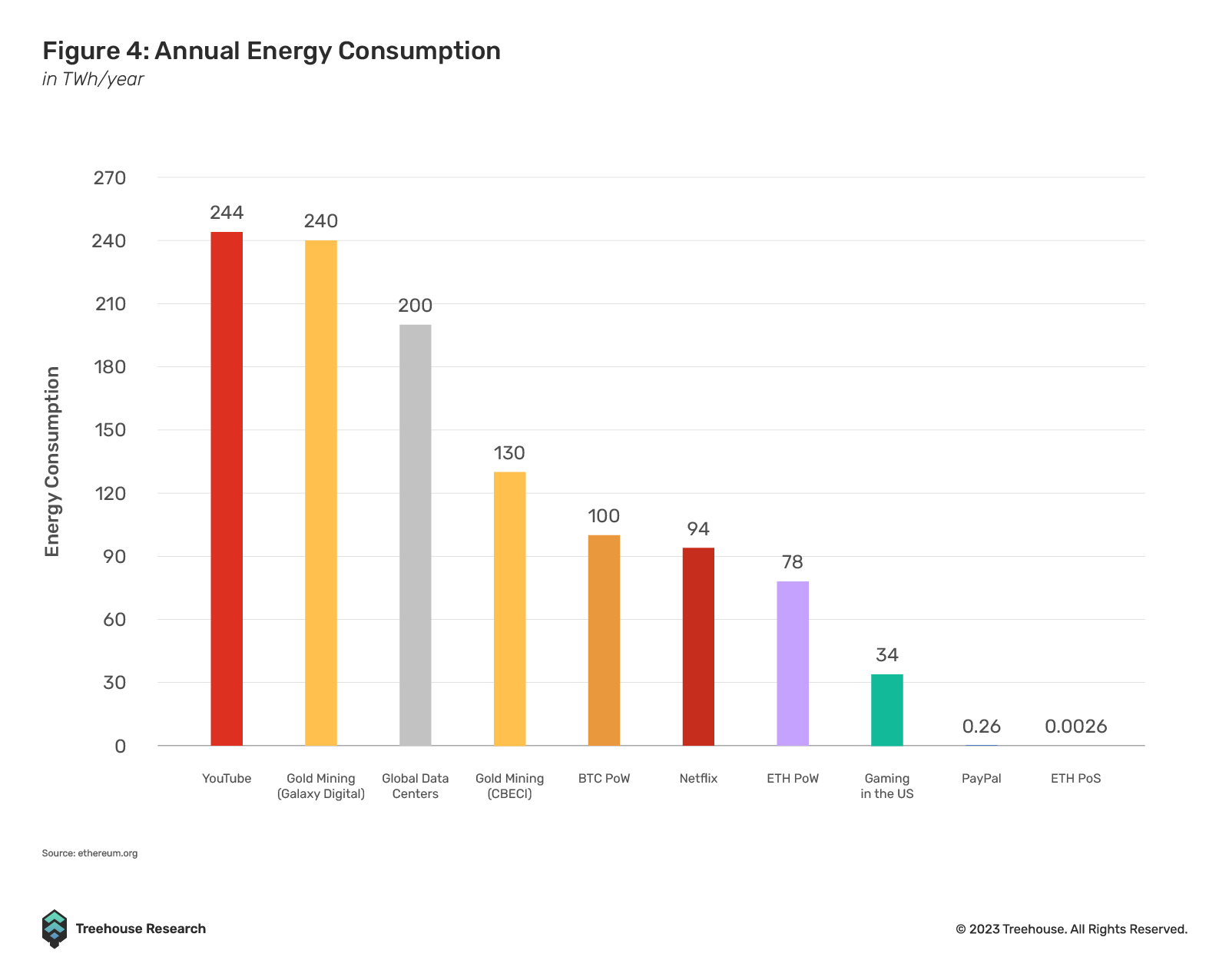

Despite the tall order, the Merge was completed without technical hiccups. This transition meant that the energy consumption needed to maintain the network will no longer be an environmental concern as PoS does not require energy-intensive mining rigs for its consensus mechanism, unlike PoW. The energy usage fell by over 99.95% and is estimated to be 1% that of PayPal.

Moreover, the Merge has enabled Ether (ETH) to become a deflationary asset as the rewards paid under the PoS consensus mechanism fell. In fact, there were periods where high demand for the network resulted in more ETH being burned than created. Since the Merge, ETH supply has only increased by 3.8K, compared to 1.2M if it had remained under PoW consensus (assuming an issuance rate of 13.5K ETH per day). Considering ETH’s current value, this means that over US$1.4B of selling pressure was eliminated because of the Merge.

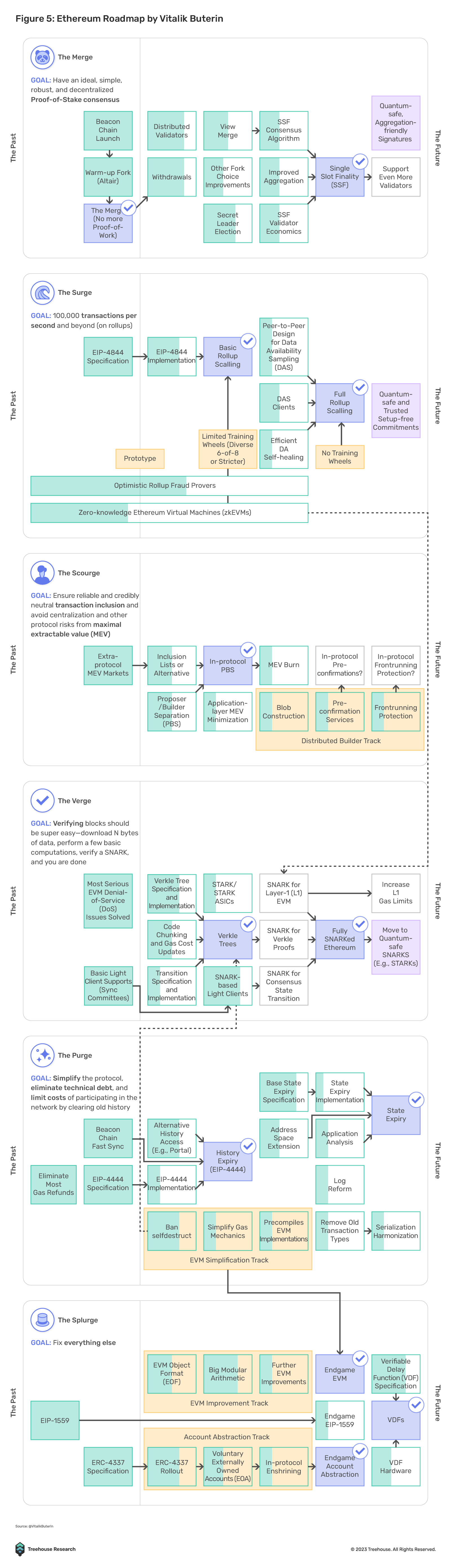

The Merge did not drastically change the end-user experience, where gas fees remain relatively high compared to other networks. The Merge, however, set the stage for future scalability upgrades. Aside from the Shanghai upgrades, there is more to look forward to as laid out by Vitalik in his tweet.

The next major upgrade is the introduction of EIP-4844, also known as Proto-Danksharding. The aim is to reach 100K transactions per second (TPS), where an initial form of “blobs” will be implemented to replace the current calldata format that rollups use to post transaction data back to Ethereum. This will likely be the next monumental milestone for Ethereum, as it will significantly reduce gas fees for rollups. This would be made possible as data will be stored more efficiently using large fixed-size “blobs” and the need to store data permanently on Ethereum will be removed. Once EIP-4844 is finalized, Ethereum will then be able to focus on Danksharding, which seeks to introduce data availability sampling.

Other EIPs to note include the following:

- EIP-3651: Warm COINBASE

- EIP-4488: Transaction calldata gas cost reduction with total calldata limit

- EIP-1153: Transient storage opcodes

- EIP-4444: Bound Historical Data in Execution Clients

- EIP-4337: Account Abstraction Using Alt Mempool

LSD Market Shakes Up as Shanghai Upgrade Nears

Liquid staking saw a huge increase in interest as The Merge emerged and materialized. Proof-of-Stake (PoS) compromised DeFi liquidity as token holders were limited to choosing between staking yield or liquidity provision. Liquid staking derivatives (LSD) solve this dilemma by enabling token holders to do both simultaneously. LSD protocols issue a liquid synthetic token that is closely pegged to the underlying token whenever a user deposits the underlying token.

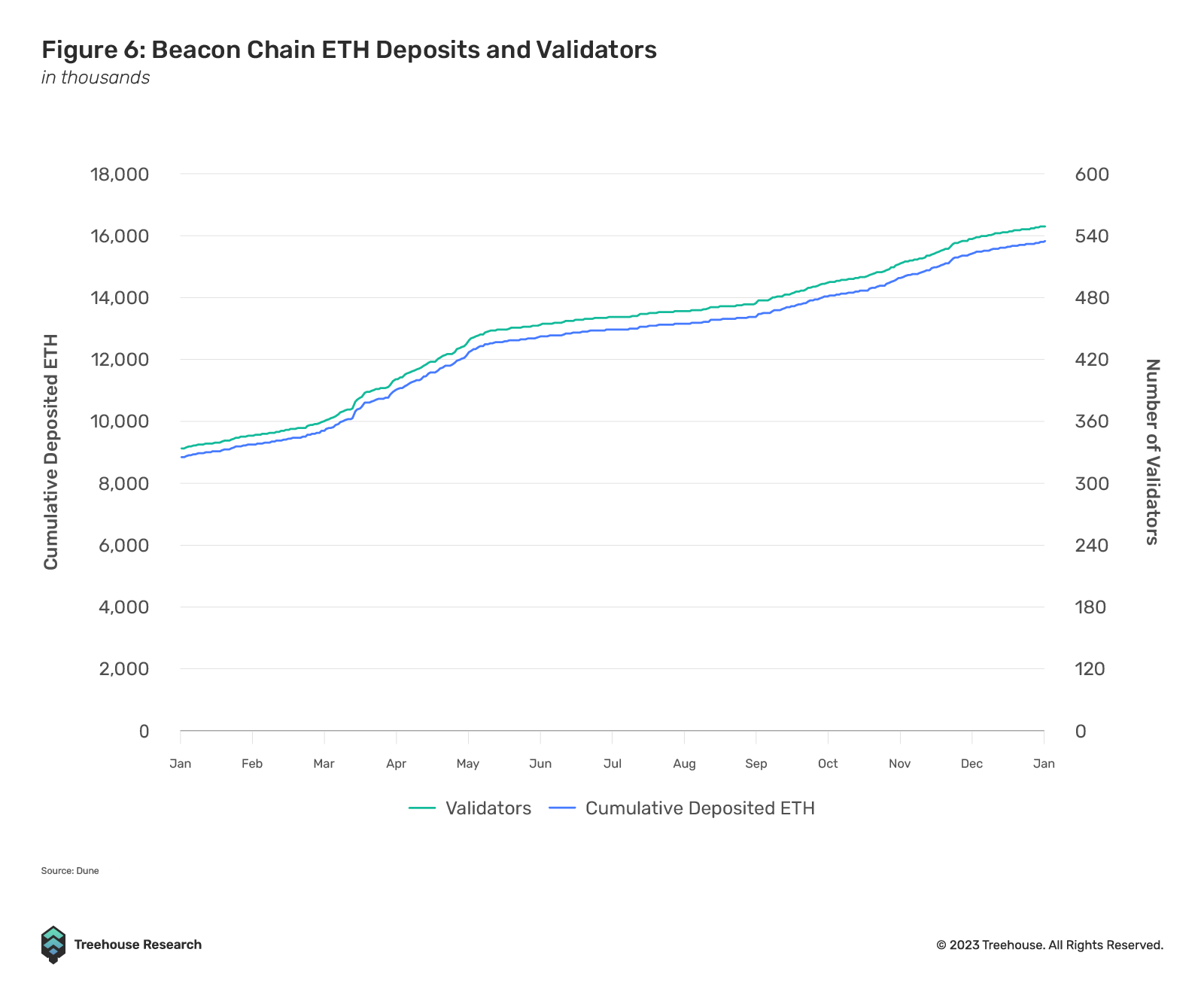

In December 2020, Ethereum’s Beacon Chain went live. This chain was the sandbox environment where new PoS consensus logic could be tested before Ethereum Mainnet merged with the Beacon Chain to transit to PoS. The Ethereum LSD market took off significantly through 2022 as the amount of ETH staked increased by 79.1% in 2022. In fact, there was an increase of 15.4% post Merge, from 15 September 2022 to 31 December 2022.

Lido, which also launched in December 2020, capitalized on its first-mover advantage to dominate the market. Other competitors include Coinbase’s cbETH and Rocket Pool’s rETH.

Despite its promising utility, Ethereum’s LSD market went through a rough patch. stETH (Lido’s LSD) depeg caused panic in the markets as stETH was used as collateral in various protocols. This sparked fear of a potential liquidation cascade as many monitored liquidation levels.

LSD is prevalent not only in the Ethereum network but also in other PoS networks. Lido, for example, is also present on Solana, though its market share is low as compared to Marinade. Other notable players include Benqi on Avalanche, Ankr on BNB chain, Stader on Polygon, Acala on Polkadot, Meta Pool on Near, and Stride on Cosmos.

Despite the huge attention it has received, ETH’s stake rate reached 13% by the end of 2022. This is currently below the average stake rate of other PoS networks1 at 60%.

One major event to watch is the Shanghai network upgrade, which will enable users to withdraw staked ETH on the Beacon Chain from December 2020. Once the Shanghai upgrade is completed, it will de-risk staking and potentially lead to more users staking their ETH. The upgrade is set to take place between March-April 2023.

If Ethereum’s stake rate matches that of other PoS networks, that would amount to an untapped market of about US$57M. There is still huge room for growth within the liquid staking sector, which could potentially be further boosted by more DeFi protocols accepting LSDs as collaterals.

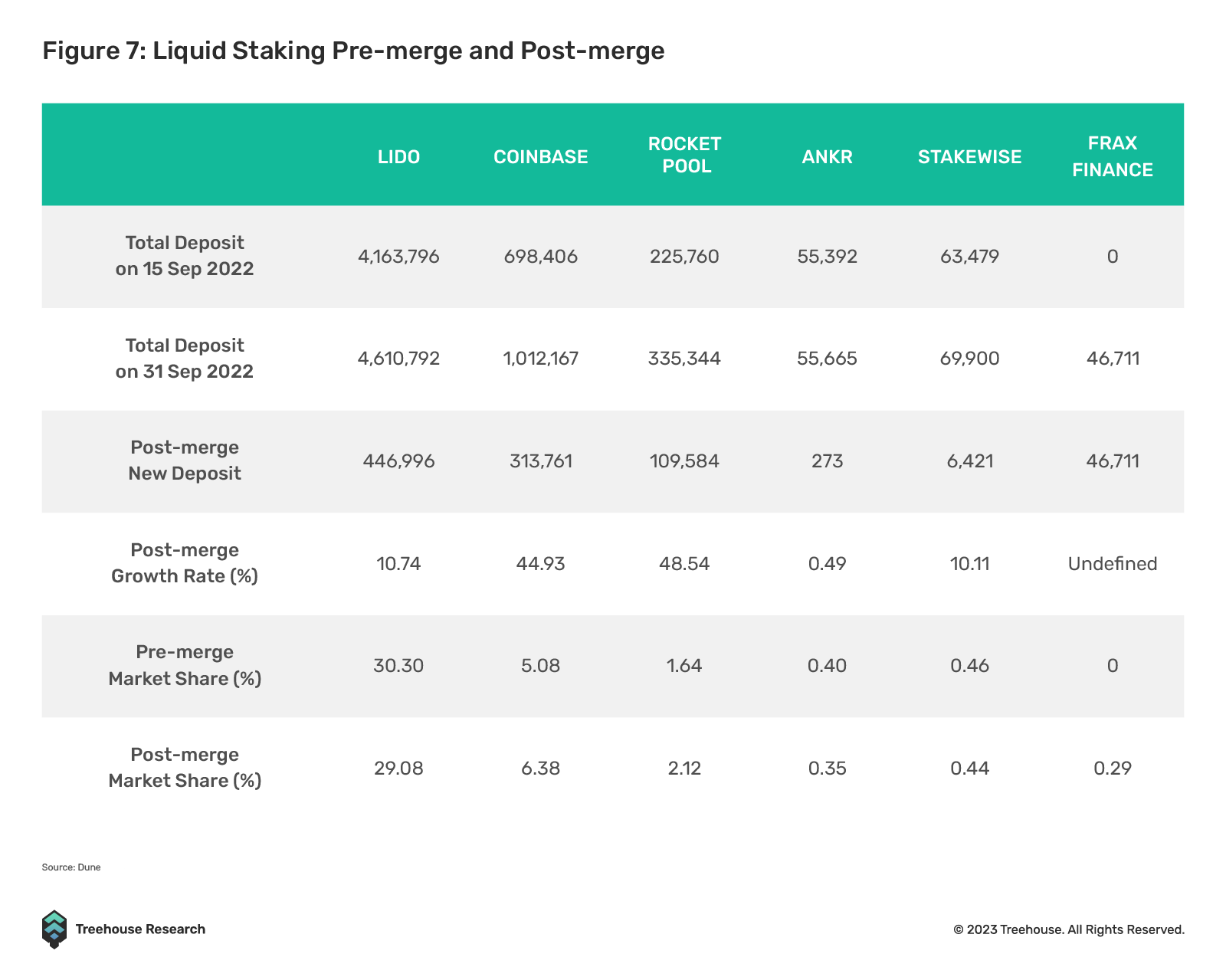

While Lido currently reigns supreme, it is facing strong competition from centralized exchanges (CEXs) like Coinbase and other non-custodial protocols like Rocket Pool, Stakewise, and Frax.

Despite attracting the most number of ETH deposits post-Merge, Lido’s market share has decreased from 30.3% to 29% due to Coinbase’s and Rocket Pool’s growing presence.

Coinbase, in particular, has managed to amass a huge number of deposits despite entering the LSD market only in June 2022. The likely reason is that Coinbase capitalizes on its vast resources and user base to gain a competitive edge against others.

Post-Shanghai, it is clear that other product features besides liquidity will lead to a larger market share. Beyond Lido and Coinbase, several other protocols are seeking to compete for ETH liquid staking, such as Swell, Liquid Collective, Tranchess, and possibly, Binance. The LSD market will likely become more fragmented, buoyed by a surge in demand once withdrawals are enabled.

L2s Rides On Their Momentum While Alt L1s Take a Backseat

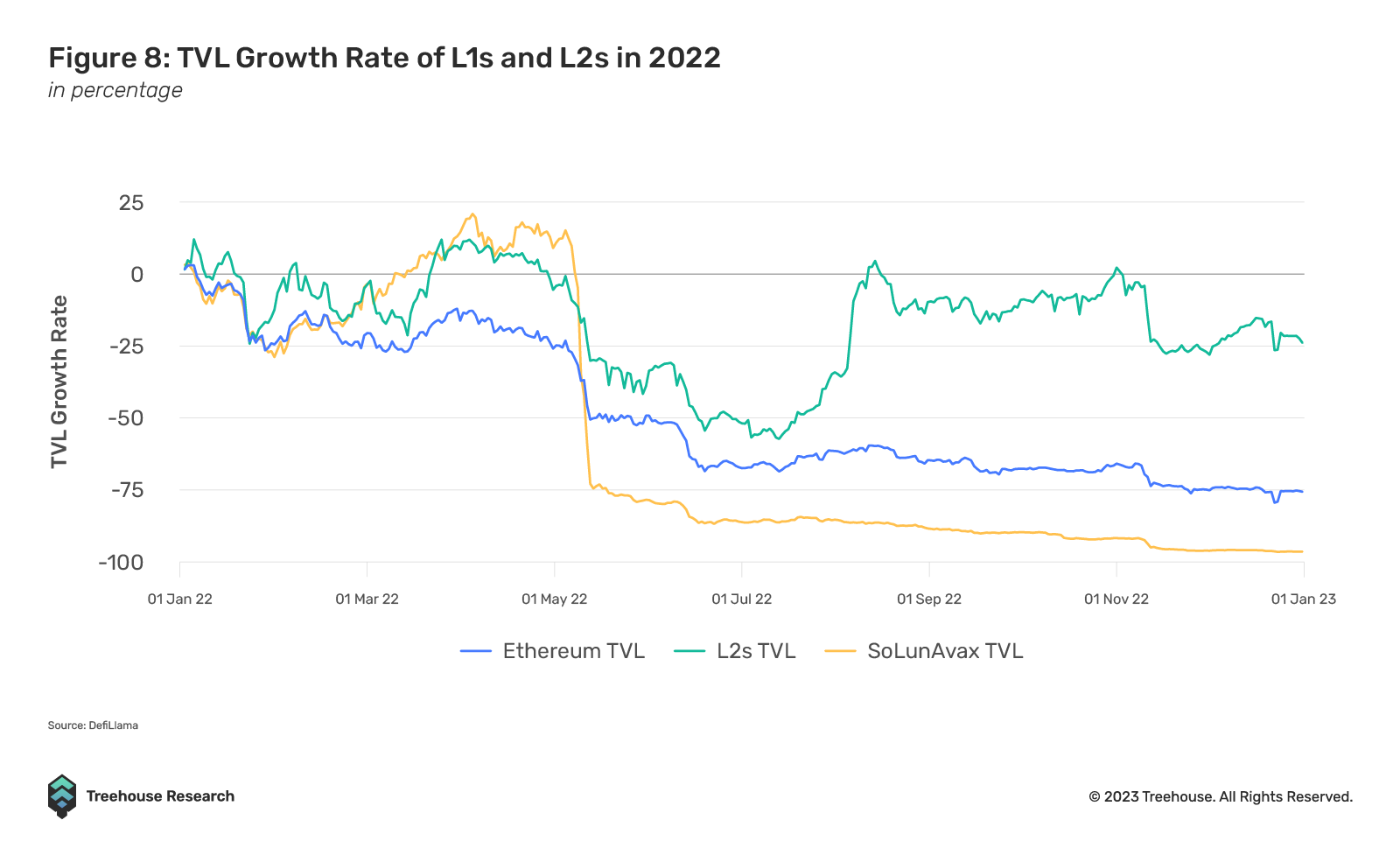

If 2021 was the year of Layer-1s (L1s), 2022 was the year where focus was switched back to the Ethereum ecosystem, particularly the Layer-2s (L2s).

The infamous “SoLunAvax” is no longer a force to be reckoned with. All three L1s, Solana, Terra, and Avalanche, were once dubbed “Ethereum killers”, but Solana and Terra’s LUNA have become a shell of what they once were, dragged down by idiosyncratic risks. Terra’s ecosystem saw a wipe out of more than US$20B in capital with UST’s death spiral. Meanwhile, Solana’s total value locked (TVL) has fallen off a cliff, dropping 96% from US$12B to less than half a billion. This is due to performance shortcomings and close affiliations with FTX and Alameda. Solana Foundation had huge exposure to FTX, including cash equivalents, FTT tokens, FTX stocks, and SRM tokens. Serum, Solana’s central limit order book, became defunct. In addition, newer alt L1s such as Aptos and Sui joined the fray to challenge Solana’s “key advantages”. Lastly, Avalanche, the “best” of the three, had a drop in TVL from US$12B to US$1B. Avalanche’s drop in TVL was primarily due to the downfall of 3AC, as the hedge fund was one of their biggest advocators. This led to a fall in investments and activities.

Meanwhile, we saw L2 networks flip ETH in terms of aggregate TPS, with Optimism and Arbitrum leading the charge. Arbitrum One was largely the most dominant L2 for most of 2022 in terms of TVL, except when Optimism briefly overtook Arbitrum One from August-October with the launch of its OP incentives on Aave V3.

Arbitrum activity accelerated after the Nitro upgrade since it led to faster and cheaper transactions on Arbitrum. Its ecosystem saw many unique apps originating from Arbitrum, including prolific dApps such as GMX, Dopex, and Rage Trade. Offchain Labs, the team behind Arbitrum, released Arbitrum Nova which is tailored to applications that require high transaction throughput and low fees. Unlike Optimism, Arbitrum has yet to release its tokens, official airdrop campaign, and incentive programs. These will likely spur further on-chain activities and development, solidifying its top spot among L2s.

Zero-Knowledge Ethereum Virtual Machines (zkEVMs) are also ones to watch as they quietly emerge with their ongoing development. These players include Polygon, Scroll, Matter Labs, ConsenSys, and Taiko. We have seen some of them deployed on testnets, but none of them are live on mainnet yet. Once they go live, it will likely shake up the current dynamics of L2s, as zk rollups promise a better experience than optimistic rollups in terms of cost, security, and privacy.

As we have seen in the past, user adoption tends to rise and fall with incentives programs as mercenary capital flocks from alt L1s to L2s whenever there are sizable yield opportunities. Since November 2022, Arbitrum’s TVL has remained resilient against other chains as users continue interacting with its ecosystem in hopes of gaining a large portion of ARBI airdrop.

Despite alt L1s falling out of favor in 2022, Aptos and Sui have a large war chest from their private fundraising. Aptos has not lived up to the hype it received when the network went live in October. All of its promising features have proved to be disappointing, with its network averaging at 7.7 TPS and peaking at 2,107 TPS, a far cry from the promised 160K TPS. Aptos developers refuted its TPS criticism, attributing it to insufficient activity to test the chain’s limits. However, if Aptos and, subsequently, Sui can live up to their promises, they can undoubtedly challenge Ethereum and L2s once more with their huge war chest.

Acceleration of Real-World Asset (RWA) Investments and Tokenization

Even with all the technological advancements in the crypto space during 2022, DeFi and crypto ecosystems remain isolated from traditional markets. DeFi products have yet to garner any widespread or tangible use cases outside of crypto, despite the increased number of product offerings and sophistication in the digital asset space. Although there have been sectors that have shown promising results during their foray into more traditionally structured instruments like DeFi credit, these sectors were plagued by their close correlation to major crypto players like FTX in 2022. Despite financial conditions remaining tight in 2023, we believe DeFi protocols will seek to diversify their risks by investing in more RWAs. As protocols attempt to tokenize RWAs in various ways, new on-chain financial primitives will be created.

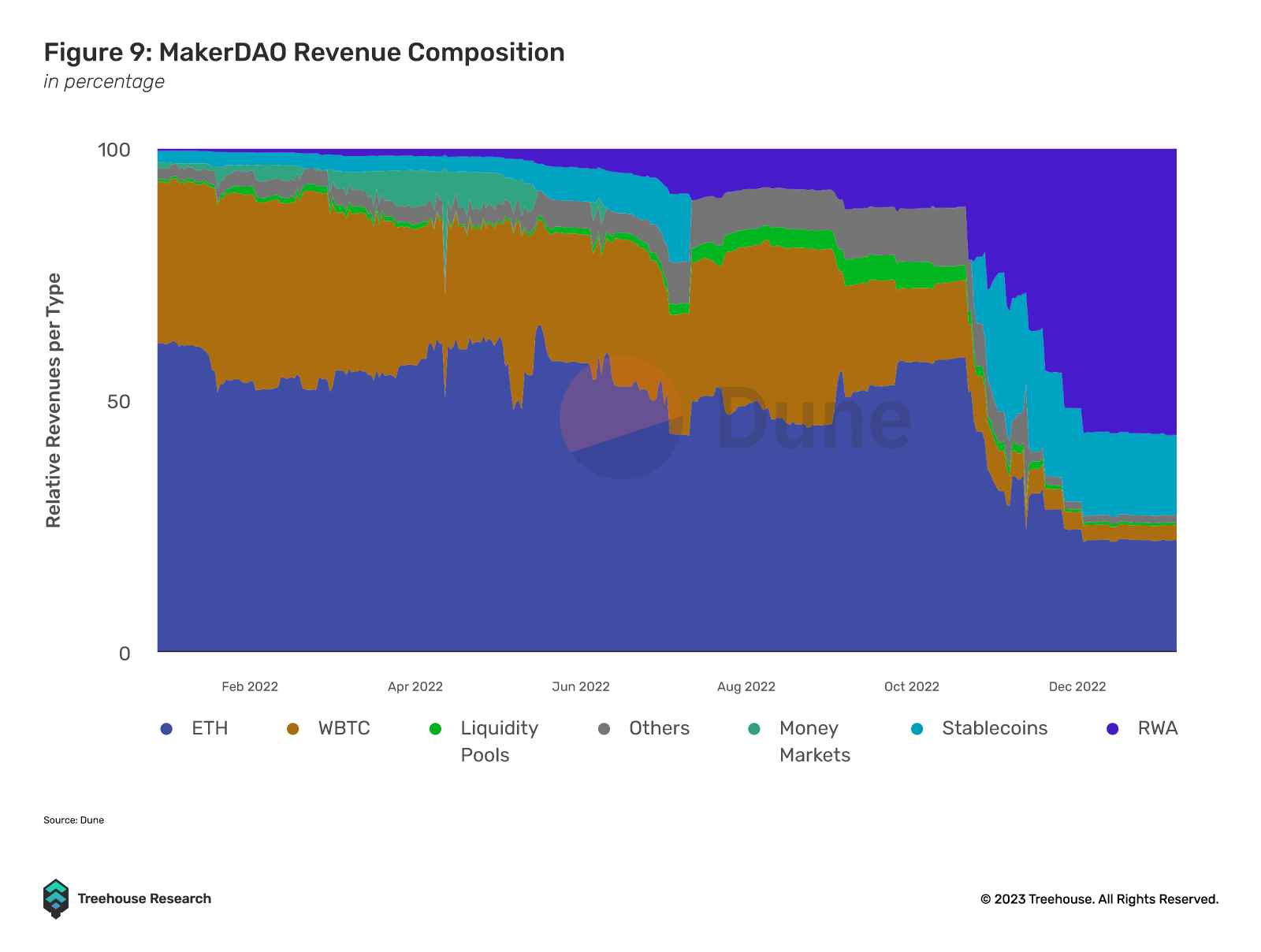

In 2023, more DeFi players will likely look to bring RWA on-chain to access more forms of yield and increase their revenue. As yields and volume dried up across DeFi in 2022, protocols seeking ways to diversify their sources of yield looked to RWAs, with MakerDAO being one of the first protocols to implement traditional instruments in their revenue strategy. MakerDAO has notably passed the proposal MIP65, which sought to allocate US$500M DAI to liquid US Treasuries.

The implementation of RWA into MakerDAO’s suite of treasury strategies has been successful thus far, with RWA now making up more than 50% of their protocol revenues, bringing in US$21.8M of annualized revenue as of 7 January 2023. It would not be surprising to see more decentralized autonomous organizations (DAOs) and DeFi protocols seek to onboard RWA as a part of their treasury management strategies. In the wake of massive events that have shaken crypto markets in 2022, it is even more likely that protocols will be on the lookout for assets that are insulated from the volatility of the crypto markets. This is to ensure consistent sources of yield that might even work as hedges against possible periods of key crypto player capitulation in the future.

Additionally, DeFi could likely explore more forms of RWA tokenization as markets realize the promise of capturing market share from these otherwise illiquid assets. Bringing illiquid assets like real estate on-chain can help increase these assets’ use cases and value propositions due to the ability to programmatically pool capital and reach investors globally.

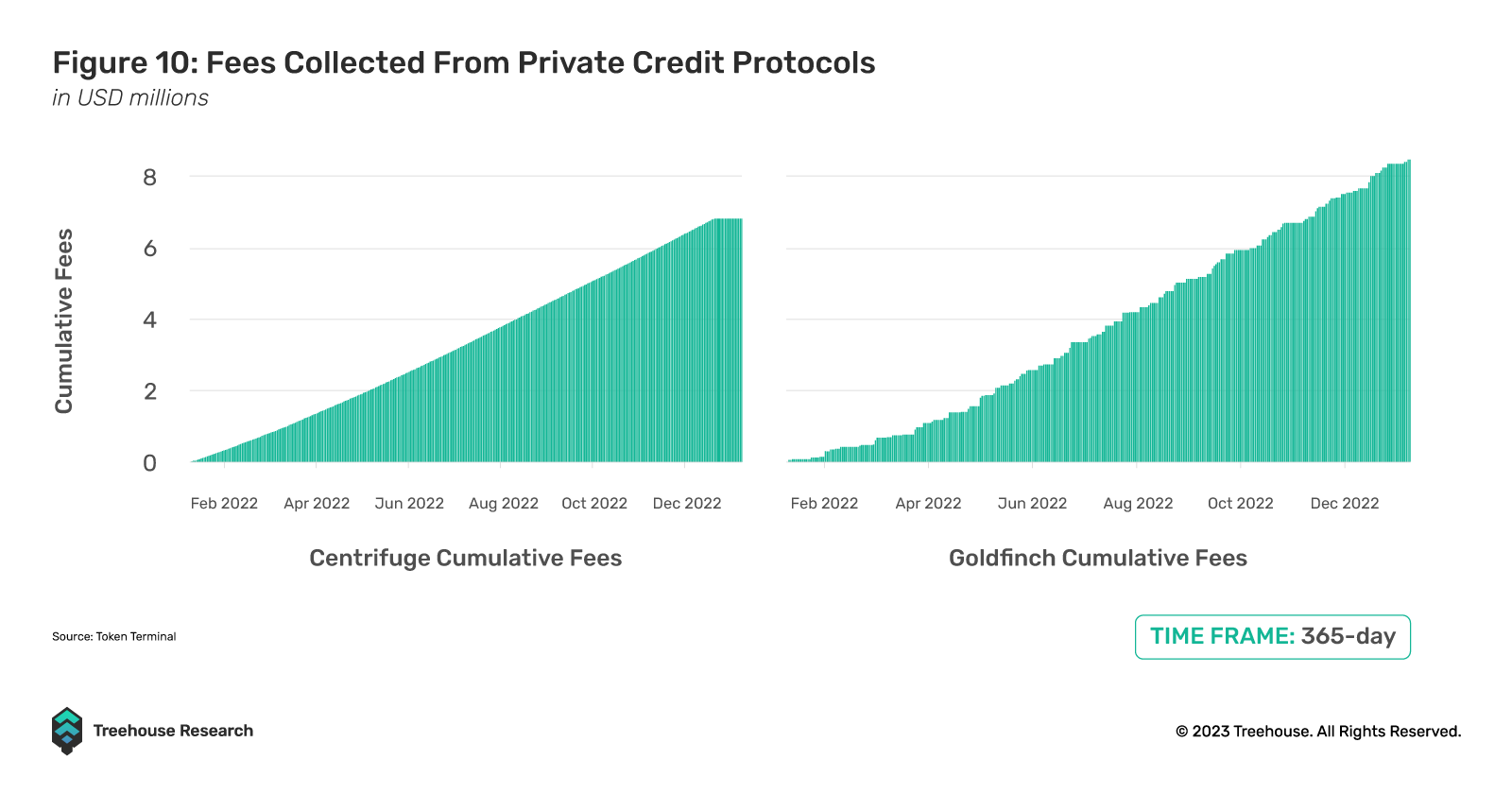

Protocols like Centrifuge and Goldfinch have generated significant lending volume and revenue this year, which is a testament to the market’s demand for stable yield from uncorrelated RWAs.

For DeFi to truly scale and compete with legacy players, RWAs must be onboarded to the blockchain. This would increase the total addressable market that DeFi can capture. If these attempts prove to be successful in 2023, they could spur the next influx of fresh liquidity and participants into the industry, though there may be legal hurdles to overcome.

Stablecoins Continued Growth and Protocol-Specific Use Cases

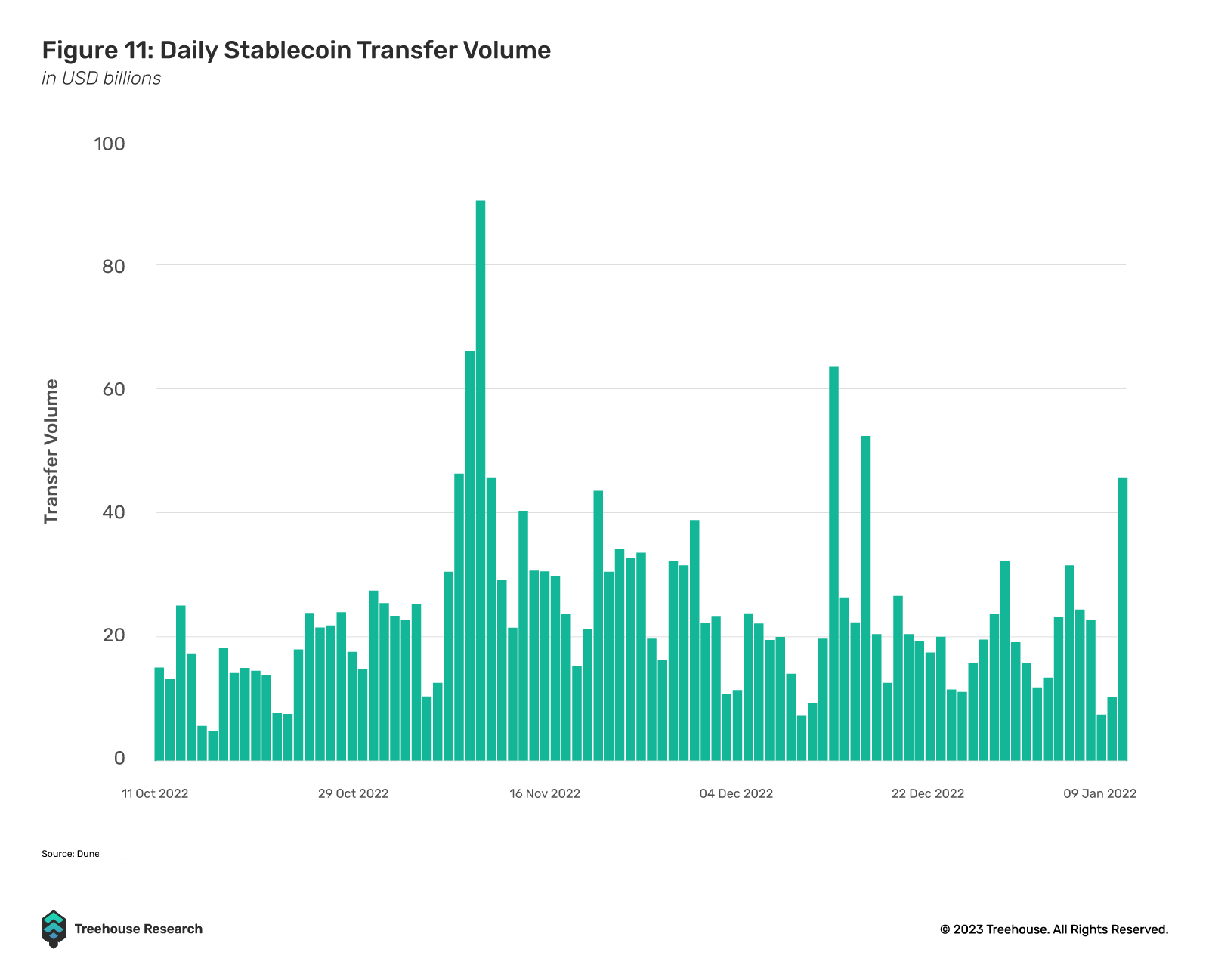

Stablecoins are undoubtedly still one of the most widespread use cases for DeFi, from forming LP pairs to lending or even cross-border transfers. Although the collapse of UST rattled investor confidence in stablecoins momentarily, the reality is that stablecoins are still being transacted at massive volumes daily, as they do not suffer from the volatile price fluctuations that normal cryptocurrencies might.

Stablecoin usage is likely to grow in 2023 due to decentralized stablecoins launched by DeFi incumbents. DeFi giants like Aave and Curve have already announced the launch of their own stablecoins GHO and crvUSD, respectively. Since these protocols are some of the most actively used DeFi protocols, we will likely see more widespread adoption of these decentralized stablecoins when they launch.

The mechanisms of these two stablecoins are designed in a manner that is complementary to the respective protocols. For example, Aave plans to allow stkAAVE holders to borrow GHO at a discount, which could help drive additional demand for their native token AAVE due to the need to purchase AAVE to access these cheaper borrowing rates. This design also helps to secure AAVE as there would be more stkAAVE in its safety module.

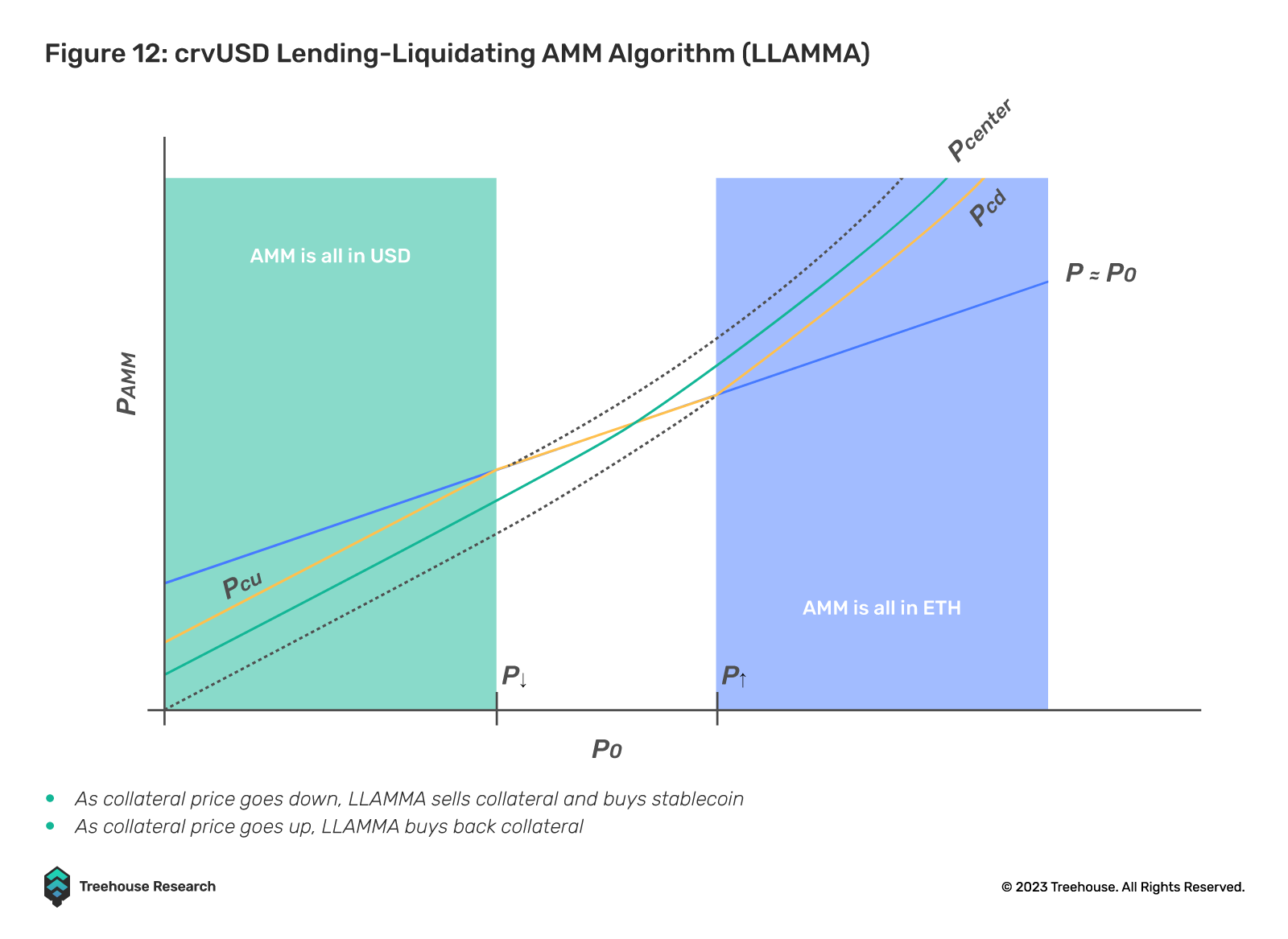

crvUSD is similarly designed to be a solution to several problems that DEXs can face. Its lending-liquidation automated market maker algorithm (LLAMMA) helps to increase trading volume due to its unique mechanisms, and it can also increase revenue for Curve through a crvUSD borrowing fee.

If the decentralized stablecoin projects by Aave and Curve are successful in 2023, we will likely see more protocols follow in their footsteps in an attempt to direct more revenue and liquidity to themselves while also increasing the utility of their native tokens. Stablecoins will be an interesting sector to take note of in 2023.

#RealYield Continues Its Dominance

Real Yield was one of the top narratives of 2022 after the collapse of LUNA wiped out multitudes and caused the DeFi crowd to reflect deeply on the merits of good tokenomics and protocol design. The DeFi crowd realized that inflationary high annual percentage yields (APYs) were unsustainable, as holders and farmers of these tokens would only be able to turn a profit if the buying pressure on their farmed tokens was large enough to offset the massive sell pressure from the emissions that were continually introduced to the market. If investors decided to pull their capital out of these protocols, illiquidity issues and massive price dumps would ensue. After LUNA collapsed, investors and farmers started searching for protocols with sustainable tokenomics models and yield.

This resulted in the birth of the phrase #RealYield, which was used to describe protocols that gave sustainable yields in the form of tokens with real value. Real Yield meant that protocols rewarded participants with a share of protocol revenue rather than emitting inflationary tokens. These rewards would typically be stablecoins, as they provided real value that would not erode in value. This represented a fundamental shift in the direction of DeFi, from high emission protocols, reminiscent of DeFi summer, to protocols that generated cash flow, more similar to TradFi businesses.

At the center of this “Real Yield” narrative were protocols like GMX, Gains Network (GNS), and Synthetix (SNX), to name a few. These protocols were considered sources of real yield as the yield paid out was derived from the protocols’ business model, which was constantly generating sustainable cash flow from activities like trading fee collection or interest payments.

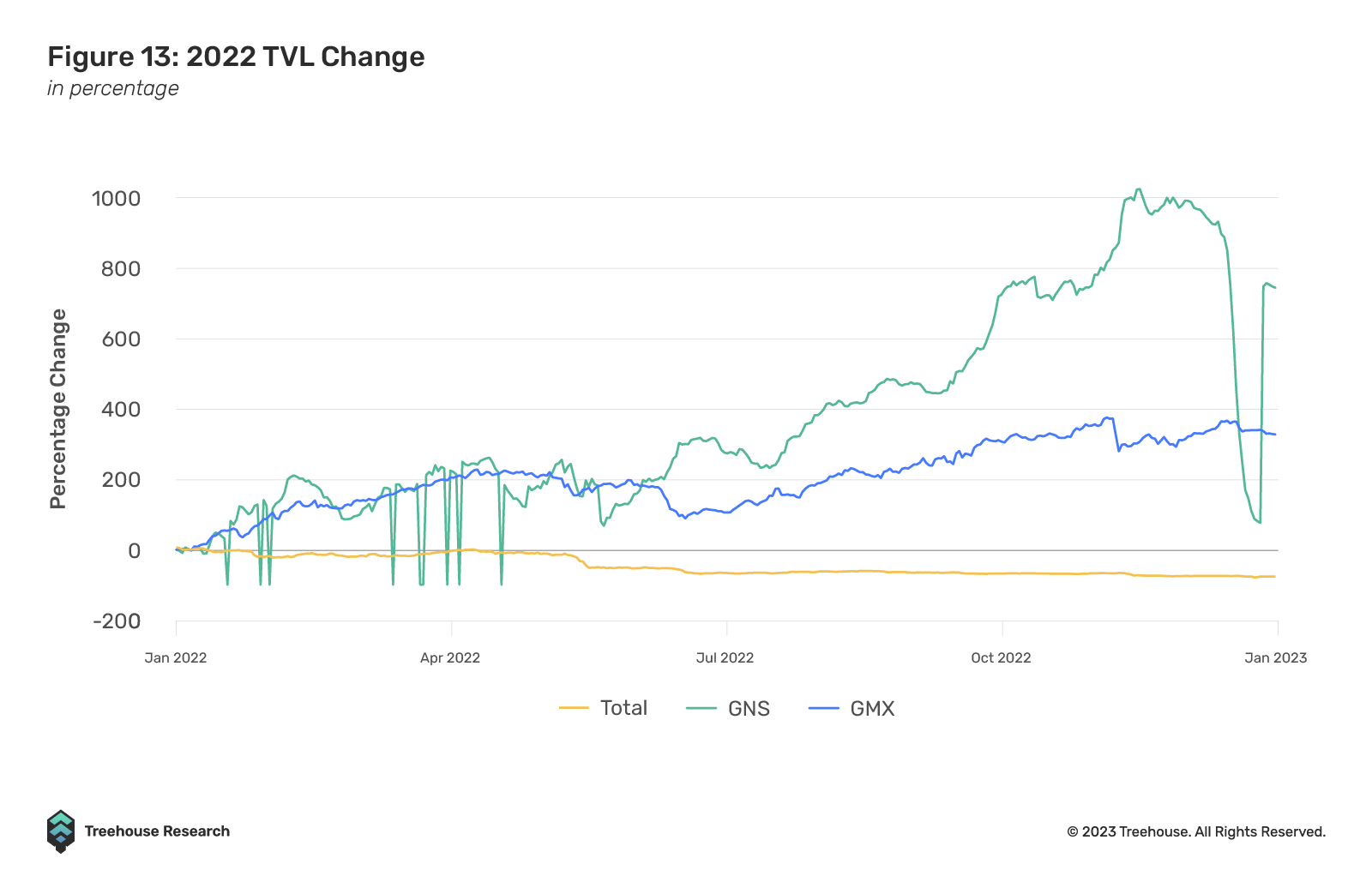

GMX and GNS, in particular, experienced massive growth throughout 2022, with their TVL growth skyrocketing despite the wider contraction in the DeFi market TVL. A reason for their popularity and outsized growth was their business model, which was running an on-chain perpetual DEX and sharing trading fees with liquidity providers (LPs). Although on-chain perpetual DEXs are not new, models like dYdX do not have any form of revenue share embedded into their native tokens, meaning that token holders cannot capitalize on the DEX’s growth.

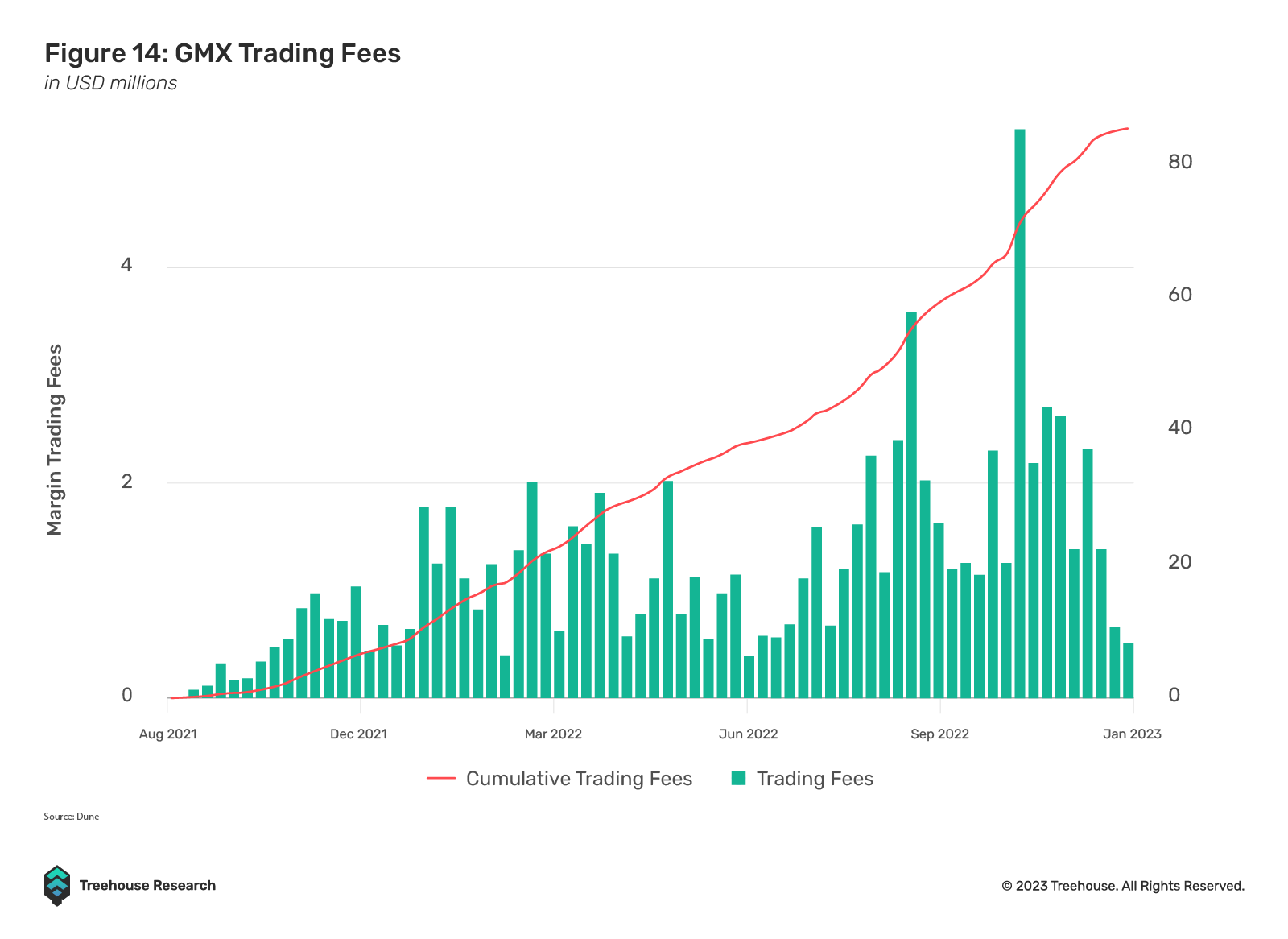

GMX

GMX, in particular, experienced massive growth, arguably bringing Arbitrum into the mainstream, and boosting on-chain activities on the L2 after the May LUNA crash. This was because of its innovative way of liquidity provision for traders in the form of GLP, which allowed LPs to earn 70% of the trading fees received by the protocol in ETH, which was considered to be extremely lucrative by many DeFi farmers.

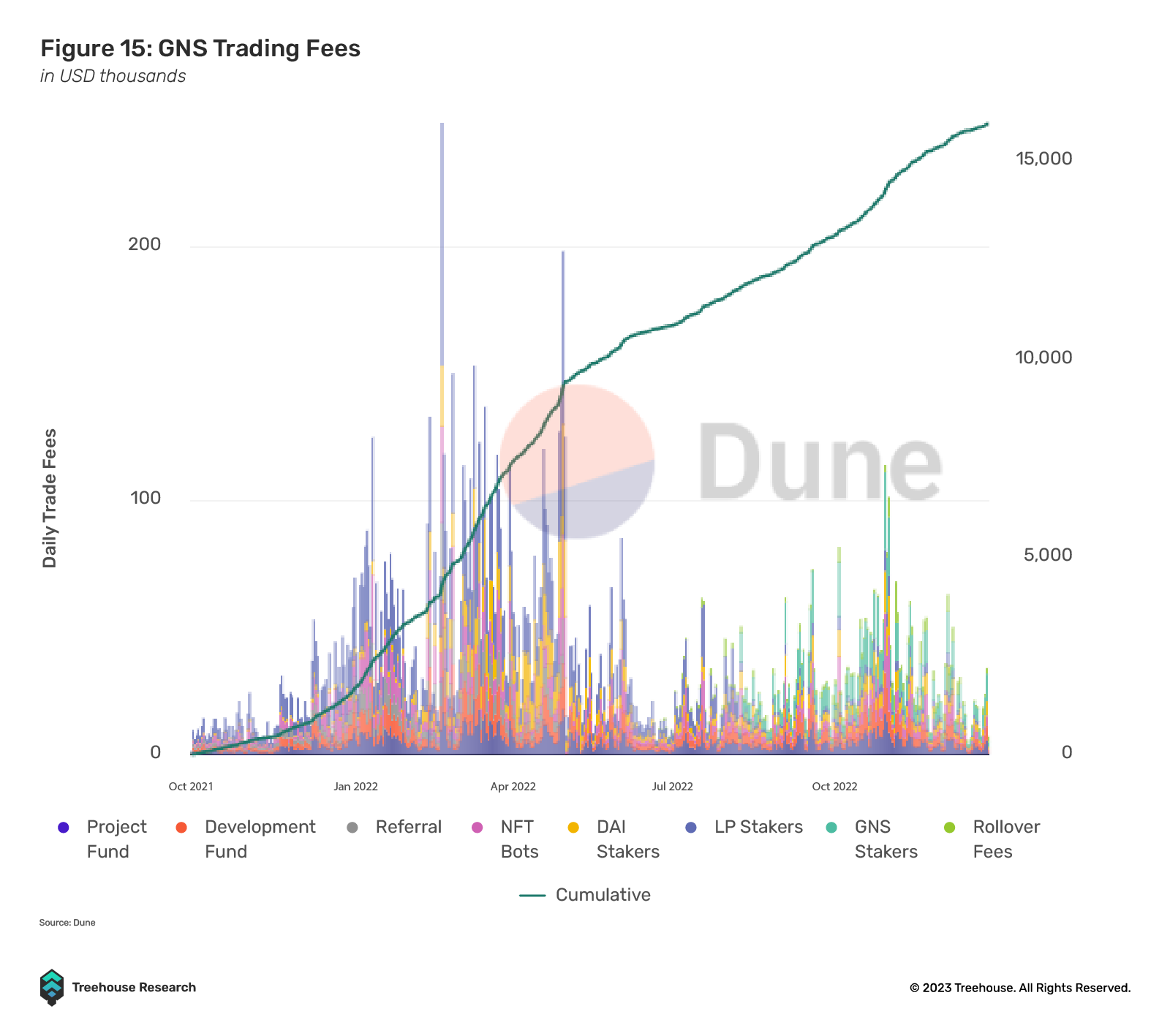

GNS

GNS, which launched on Polygon, was another heavyweight in the real yield narrative. GNS allows users to trade multiple assets, from DeFi tokens to synthetic stocks and even fiat currencies. Their liquidity provision mechanisms are similar to that of GLP, where funds are provided to a gDAI vault that provides liquidity for traders. gDAI LPs earn DAI yield from trading fees and traders who lost on trades, generating real yield for depositors.

This mechanism has helped GNS to enjoy an uptick in users and trading fees in 2022, showcasing the growth potential and demand for sustainable yield and cash flow-generating DeFi products

The #RealYield narrative was undoubtedly one of the strongest DeFi narratives in 2022 and is likely to continue into 2023. As financial conditions continue to tighten, protocols like GMX and GNS are likely to be the blueprint for any new protocols that might be built in the future. The outperformance of #RealYield protocols like GMX and GNS in terms of both price and TVL growth is a testament to the strength of protocols that can generate sustainable and consistent cash flows, and how well-designed tokenomics can drive demand for a protocol’s token.

The acceptance of RealYield by DeFi natives demonstrates a maturing DeFi space that is more skeptical of the source of yield and realistic about yield expectations. Future protocols that can consistently generate cash flow while rewarding protocol LPs sufficiently with well-thought-out tokenomics are likely to be sought after in the years to come.

Change Is the Only Constant

The crypto industry is no stranger to massive crashes and implosions, and it has gone through its fair share of ups and downs. 2022 was, however, a year that was particularly crushing and demoralizing as we saw companies that many deemed “too big to fail” bow out under the crushing weight of poor management and practices.

2023 is likely to be another year rife with macroeconomic uncertainty and tight liquidity conditions, setting itself up to be another tough year for the crypto industry. Although the industry is still reeling from the multiple black swans and implosions in 2022, it would be erroneous to say that the crypto industry, as a whole, did not make any progress in 2022. The pace of development in the crypto industry has remained steady even as it has been repeatedly faced with implosions and capital destruction. New technologies are being tried and tested every day and builders in the space are constantly looking for ideas that will bring about the “0 to 1 moment” for mass adoption of blockchain technology and DeFi.

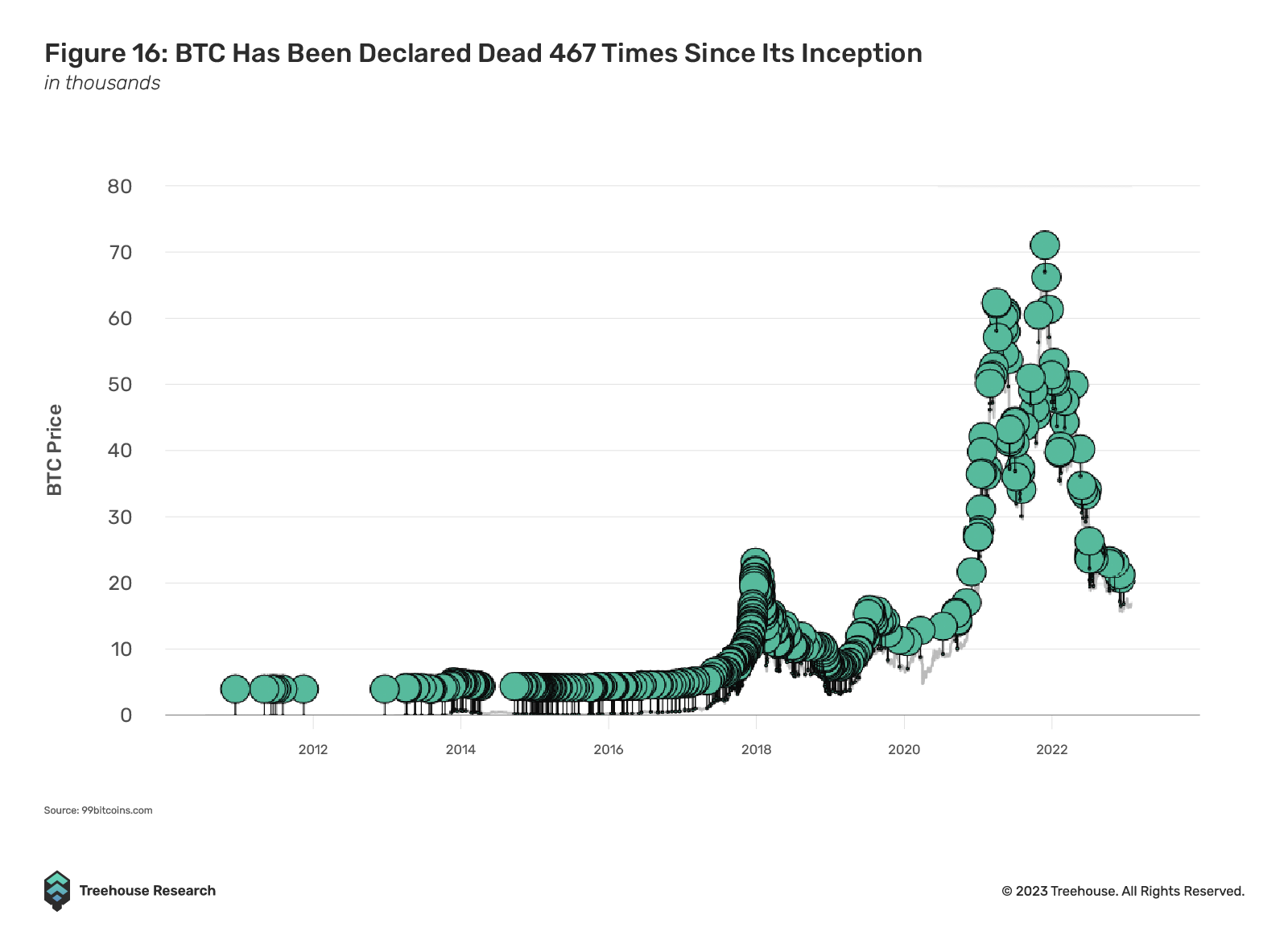

Just as the bursting of the dot-com bubble brought poorly capitalized companies to their knees, 2022 will be remembered as crypto’s dot-com moment, as industry giants fell one by one. As the industry went through its first actual economic downturn, protocols with well-thought-out mechanisms and designs thrived, while others with unsustainable designs faded into obscurity. The birth of the revolutionary FAANG tech giants only came after most speculative capital and rent-seekers were washed out of the market. Crypto seems to be following this boom and bust cycle.

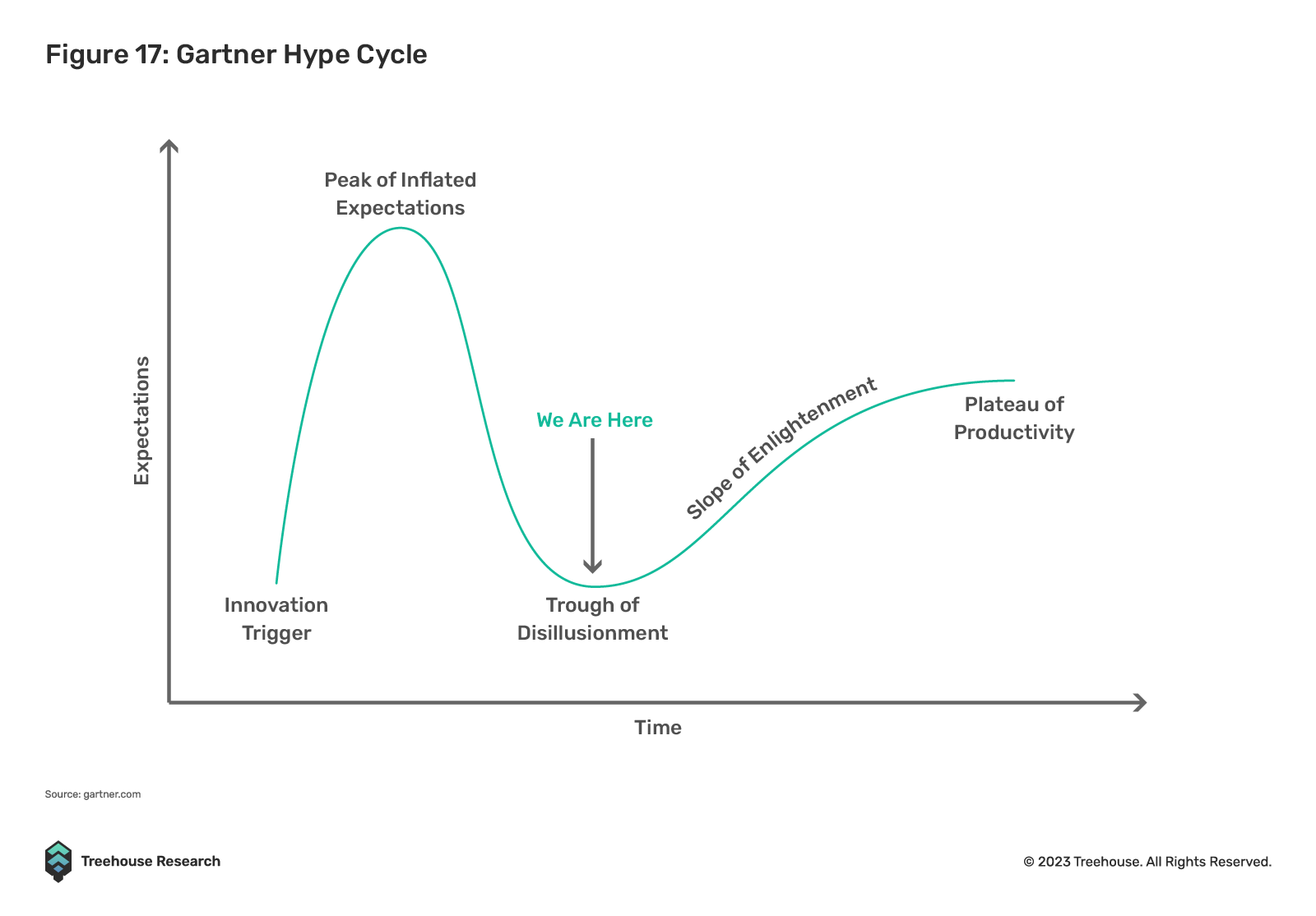

At our current point in the Gartner Hype Cycle, it is likely that many protocols will call it quits as conditions continue to worsen. However, as we weather through this bear market, protocols that continue to build and develop useful technologies will be the ones that will emerge as the key players.

Crypto and DeFi are here to stay. The relentless builders and visionaries in this industry will continue to add value to this space as it permeates into the mainstream consciousness. Crypto is inevitable and just a matter of “wen?”, not how. At Treehouse, we believe that we are building for the future of finance, and we will continue to do so regardless of the length of this dark, frigid winter. #WAGMI

Appendix

Footnote

1 Inclusive of BNB Chain, Solana, Avalanche, Polygon, Polkadot, Cosmos, Near, Tron, Cardano

Disclaimer

This publication is provided for informational and entertainment purposes only. Nothing contained in this publication constitutes financial advice, trading advice, or any other advice, nor does it constitute an offer to buy or sell securities or any other assets or participate in any particular trading strategy. This publication does not take into account your personal investment objectives, financial situation, or needs. Treehouse does not warrant that the information provided in this publication is up-to-date or accurate.

Hyperion by Treehouse reimagines workflows for digital asset traders and investors looking for actionable market and portfolio data. Contact us if you are interested! Otherwise, check out Treehouse Academy, Insights, and Treehouse Daily for in-depth research.