Options have historically played a secondary role to spot and futures. Due to its complex nature, the asset class was traditionally dominated by “smart money” institutions and experienced investors. The dynamics of the space have since shifted in recent years – seeing retail participation surging to unprecedented levels. In the midst of the Covid-19 lockdown, stay-home millennials soon found themselves with “airdropped” fiat, turning many of them to day-trading in stocks and options on zero-commission brokerages such as Robinhood.

Speculative Memestock Options Trading

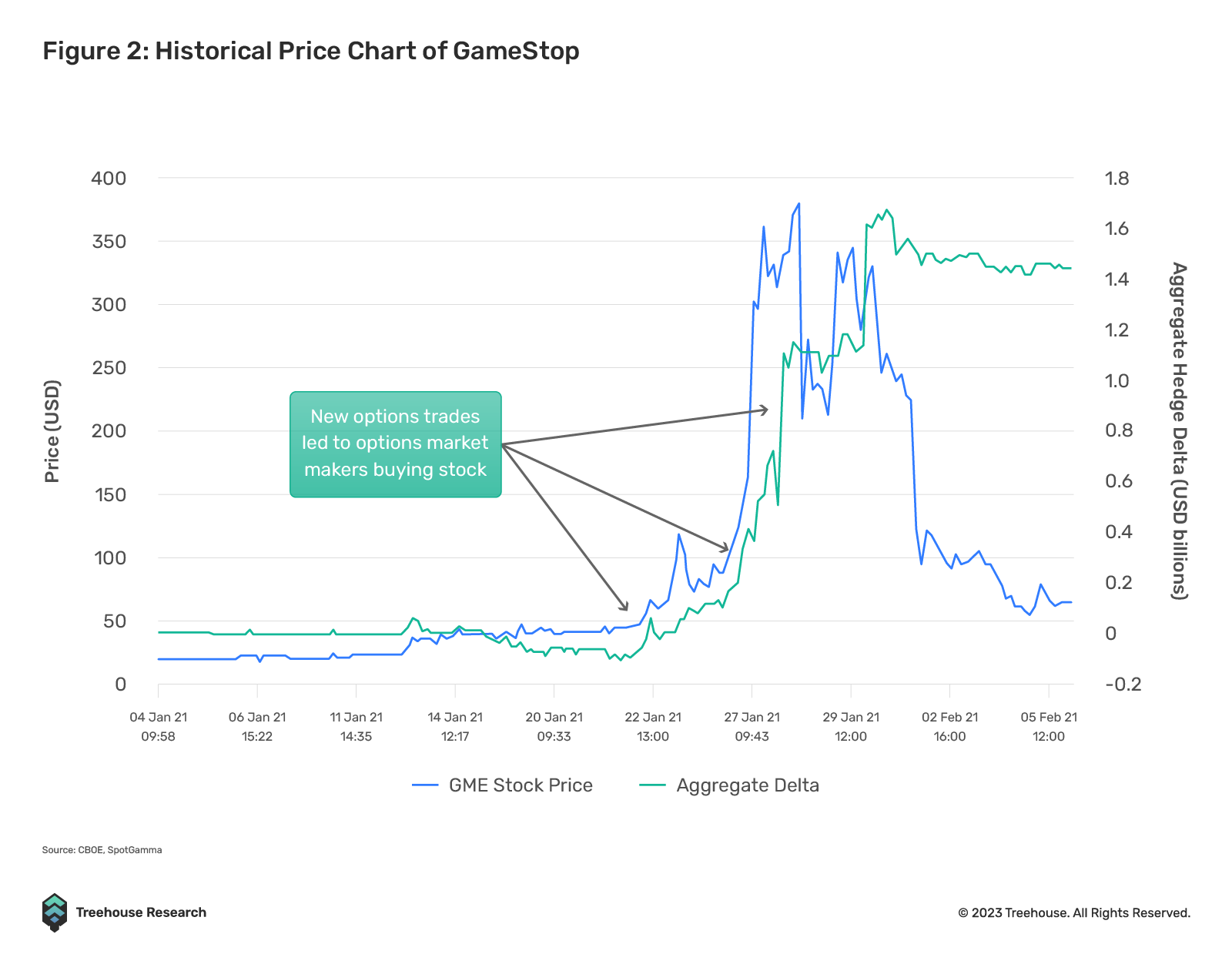

This shifting phenomenon was first broadcasted in January 2021 when “Memestocks” such as GameStop (NYSE: GME), AMC Theatres (NYSE: AMC), and Bed Bath & Beyond Inc (NYSE: BBBY) made headlines for their skyrocketing stock prices.

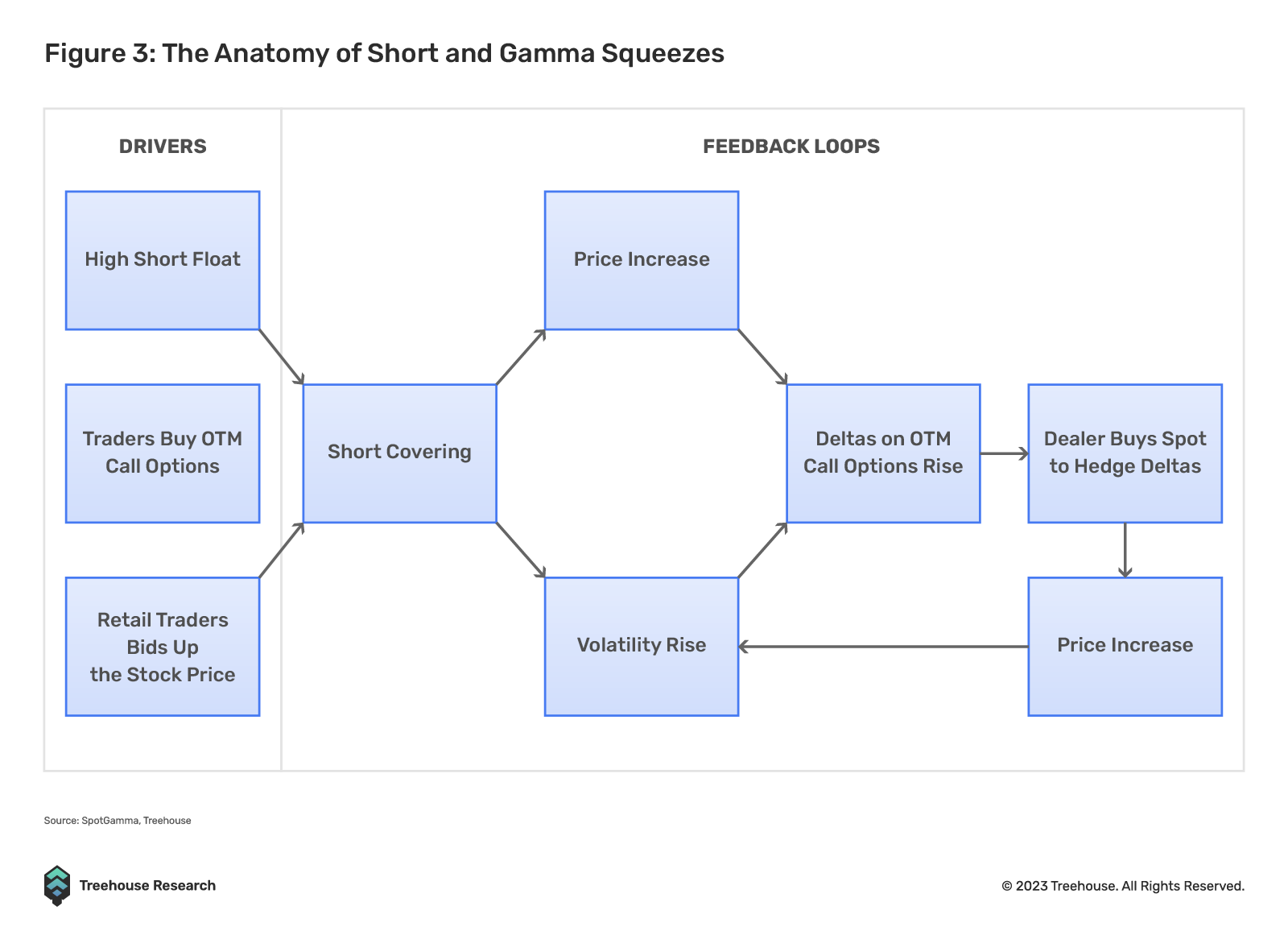

Amongst the burgeoning narratives surrounding the move were retail participants, captivated by the ideas of “Gamma Squeezes” and “Dealer’s Hedging” learnt on forums such as Reddit. Outside of the high short-float that had sparked the initial run, the meteoric rise in these memestocks was further exacerbated by outsized purchasing of calls from retail investors.

As the price and implied volatility (IV) of these memestocks rose, their corresponding out-of-the-money (OTM) options deltas increased. Dealers who sold the retail army call options were forced to buy more of the underlying stock to hedge – creating a positive feedback loop (figure 3) that dramatically drove up the prices of these memestocks.

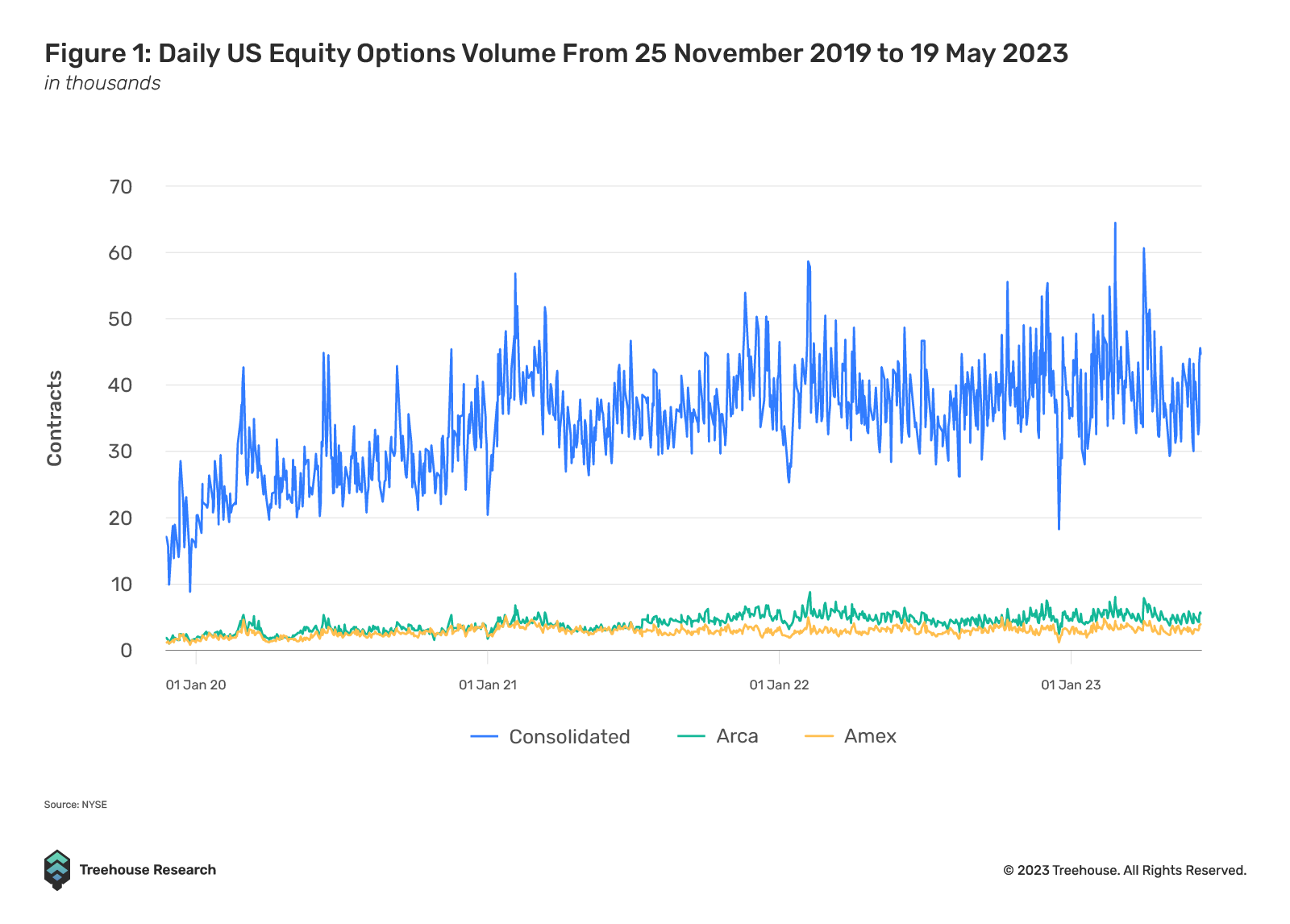

The memestock frenzy showcased the remarkable power of options to the retail investing community. With just a fraction of the underlying asset’s cost, many found that their positions could skyrocket if the timing and direction proved favorable. As a result, stock options trading volume soared in the ensuing months.

Crypto Options to the Moon?

The recent success of options in the traditional markets brought up an interesting question for us here at Treehouse – can retail interest in options be mirrored in the Cryptocurrency markets? In this two-part series, we first examine the current state of Crypto option adoption; we follow this up with a deep dive into the various models that facilitate options trading in our second article.

In our analysis, we found that the Crypto options market has seen promising growth, although it primarily remains in the hands of sophisticated and institutional traders. In contrast, retail Crypto traders have been slower to embrace the asset class, as a result of the allure of leverage offered in perpetuals trading and the limited offerings in altcoin options. As the landscape of Crypto options continues to evolve, it remains to be seen whether retail traders will seize the opportunities that options can offer.

| A New Kid On The Block – 0DTE Options Before we jump into the meat of this article, here is a fascinating appetizer to take away. 2023 has been no different than the previous years, with another trend in the options that has gained significant attention due to its low cost and remarkably large convex payout – 0DTE options. With less than a day until expiration, 0DTE options now comprise 44% of the daily trading volume for options! |

Where are we right now?

Recent Surge in Crypto Options Trading Volumes

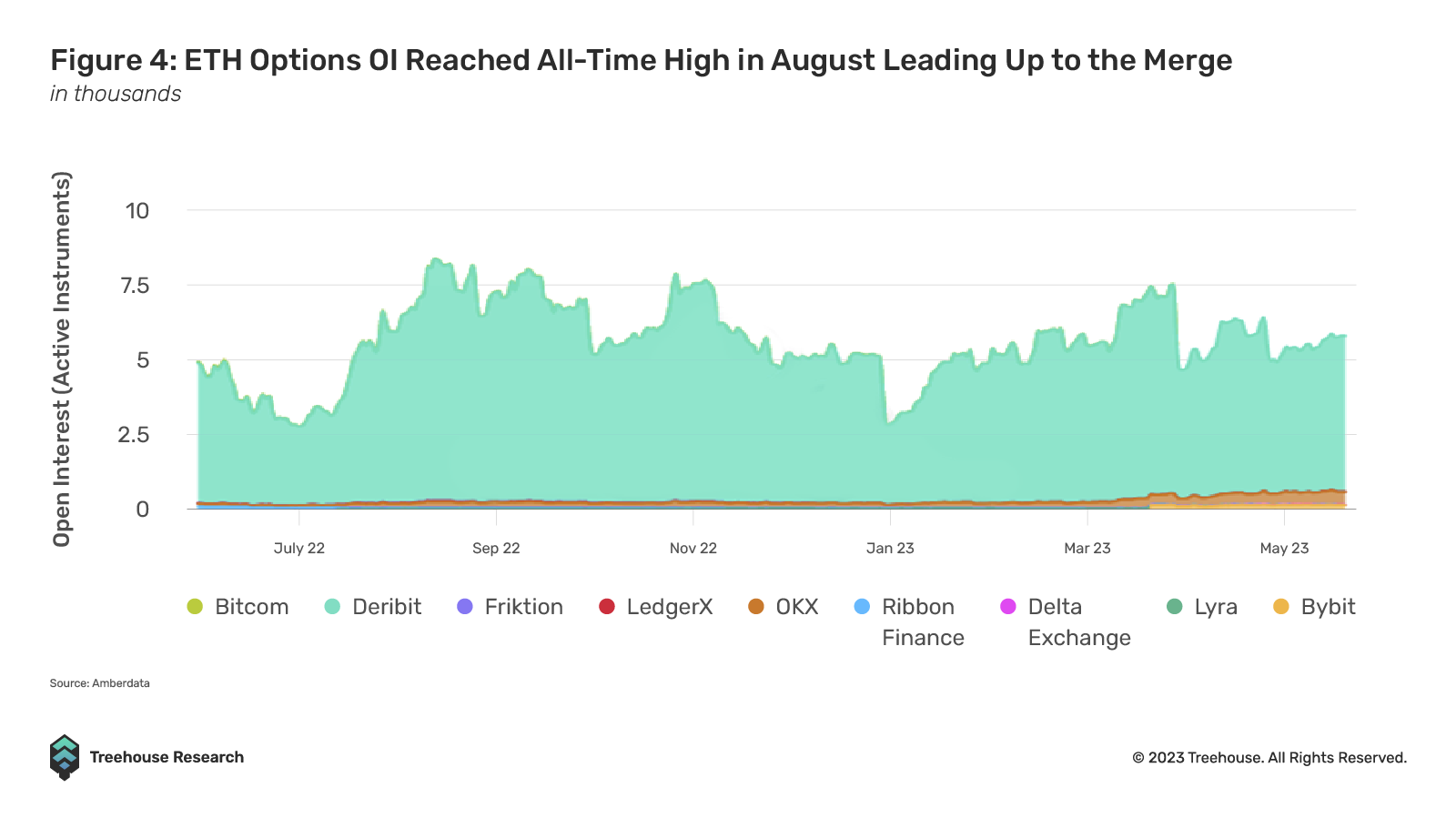

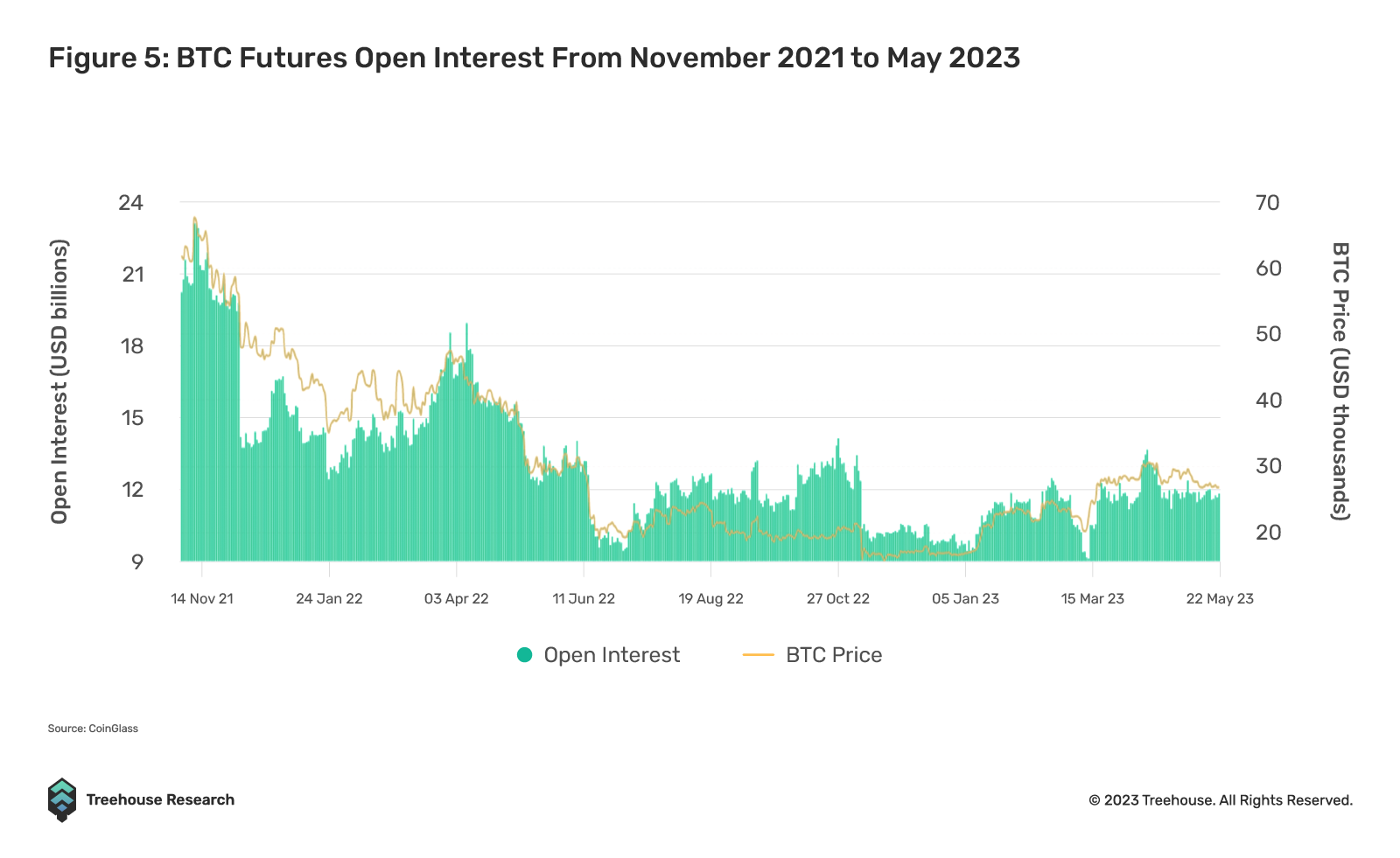

Despite the bear market, options trading in Crypto continues to gain in popularity. Volumes have been on an upward trend, reaching all-time highs as more and more institutional and sophisticated money are entering the space. Even prior to the Merge, ETH options OI peaked at an impressive $8.3 billion (excluding OTC markets), indicating a growing inclination toward utilizing options for event-based trading (figure 4). This is in stark contrast to the spot and futures market in Crypto, which has seen volume decrease as much as 50% from their highs (figure 5).

While options volume continues to grow due to institutions and sophisticated traders – there have been many strides made in both CeFi and DeFi.

CeFi Options, A Notable Uptick

CeFi Options continues to see growing adoption due to factors over the past year such as:

- The addition of Options trading to exchanges such as Binance, OKX and Bybit, opening the platform to many millions of users. These three exchanges alone contribute to over $115B in daily trading volume on derivatives, constituting just over 90% of the overall market share amongst centralized exchanges.

- Deribit’s introduction of block and combo trading catered to the specific needs of institutional clients, including larger trade sizes and multi-legged trades.

- The set up of dedicated options desk by large prominent market makers like QCP Capital and Wintermute, providing liquidity, over-the-counter (OTC) flow trading, and exotic options

- TradFi exchange groups such as the Chicago Mercantile Exchange Group (CME) that launched ETH options. CME now also offers daily expirations on BTC and ETH options to meet the expanding needs of its clients.

DeFi Options, Development Despite Initial Sluggishness

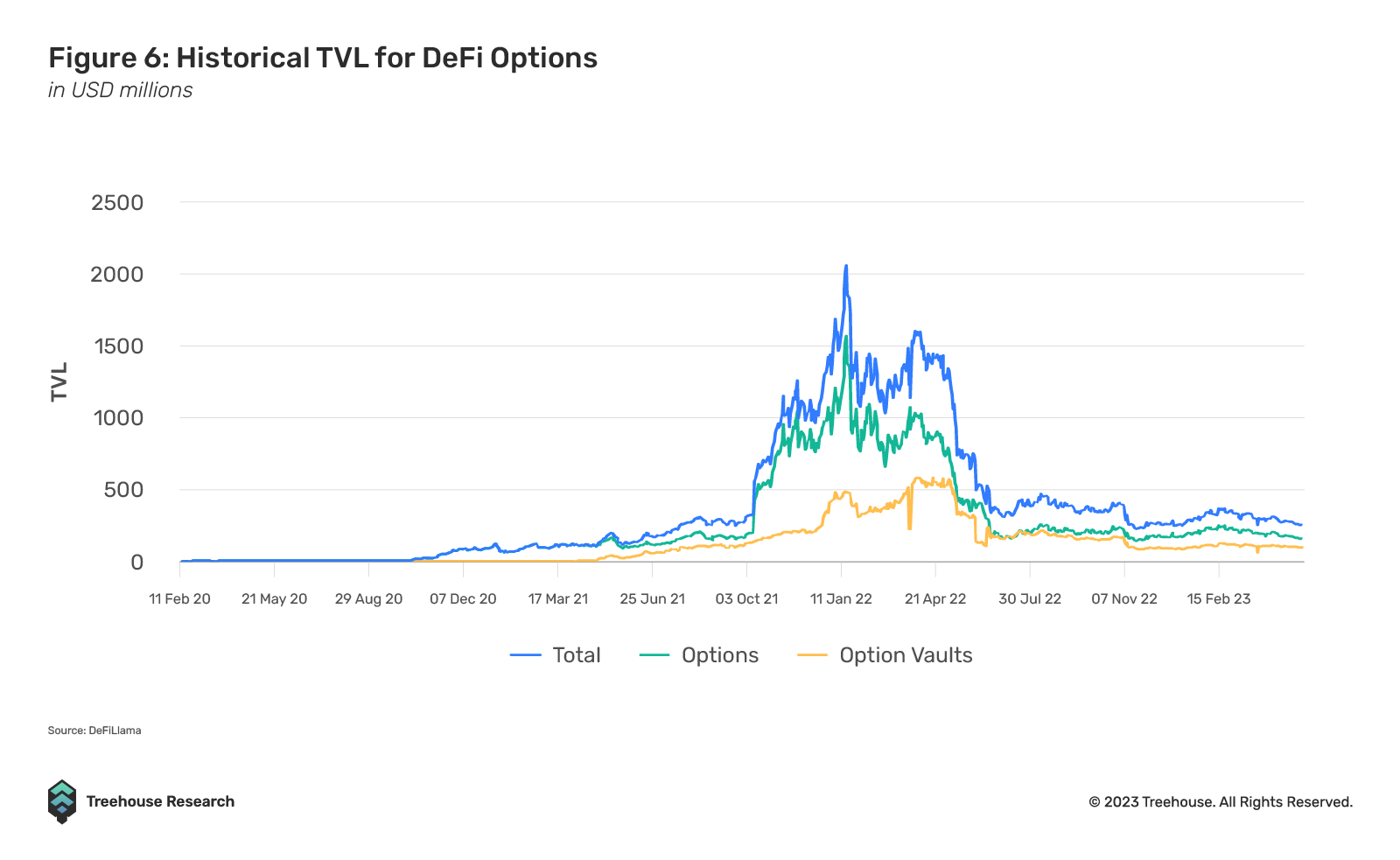

Prior to 2021, options were primarily traded on centralized exchanges such as Deribit. The options landscape changed when Ribbon Finance pioneered Decentralized Option Vaults (DOVs), opening up a new way for retail to participate in DeFi Options. Since then, DeFi options protocols have seen a general increase in interest. In January 2022, TVL across all DeFi options protocol hit a high of $2.06B, up from just $67M the year before, a rise of nearly 30X.

In our previous Insights article, “DeFi Option Vaults: Options Democratized”, we discussed how DOVs have been a popular way to bootstrap investors into the fray of Crypto options. These DeFi instruments provided simple automated strategies for investors for their first foray into the world of options trading. Since their launch in 2021, Ribbon has done more than $13.55B in notional volume alongside Opyn, driving 90% of the total option volume on-chain. Now, more and more protocols are innovating for on-chain investors to trade options with the likes of Premia, Lyra, and Dopex.

Furthermore, there has been a growing influx of TradFi experts entering DeFi with the intention to build derivatives infrastructure. More specifically, these TradFi experts often hail from the derivatives or structured products desk. Given their prior experience with derivatives trading in large TradFi firms, it is only natural this would be their entryway into the DeFi landscape.

Overall, the developments observed in trading volumes and the evolving landscape of both CeFi and DeFi options indicate a burgeoning recognition of the significance and untapped potential that options offer within the Cryptocurrency space.

The Emergence of Volatility Trading in Crypto Options

Harvesting Variance Risk Premium – A Way to Generate Yield

Due to the onset of the bear market in early 2022, ‘easy’ trading opportunities like DeFi yield farming and cash futures arbitrage have diminished. Hence, attention in Crypto options specifically moved to yield-generating structured products such as call overwriting and put underwriting. After the Terra-LUNA crash in May 2022, vanilla selling of volatility to harvest variance risk premium (VRP) became a profitable endeavor. For the most part, realized volatility (RV) underperformed implied volatility (IV) on average during those few months. That led to more and more traders entering the options space in order to capitalize on the variance risk premium (VRP).

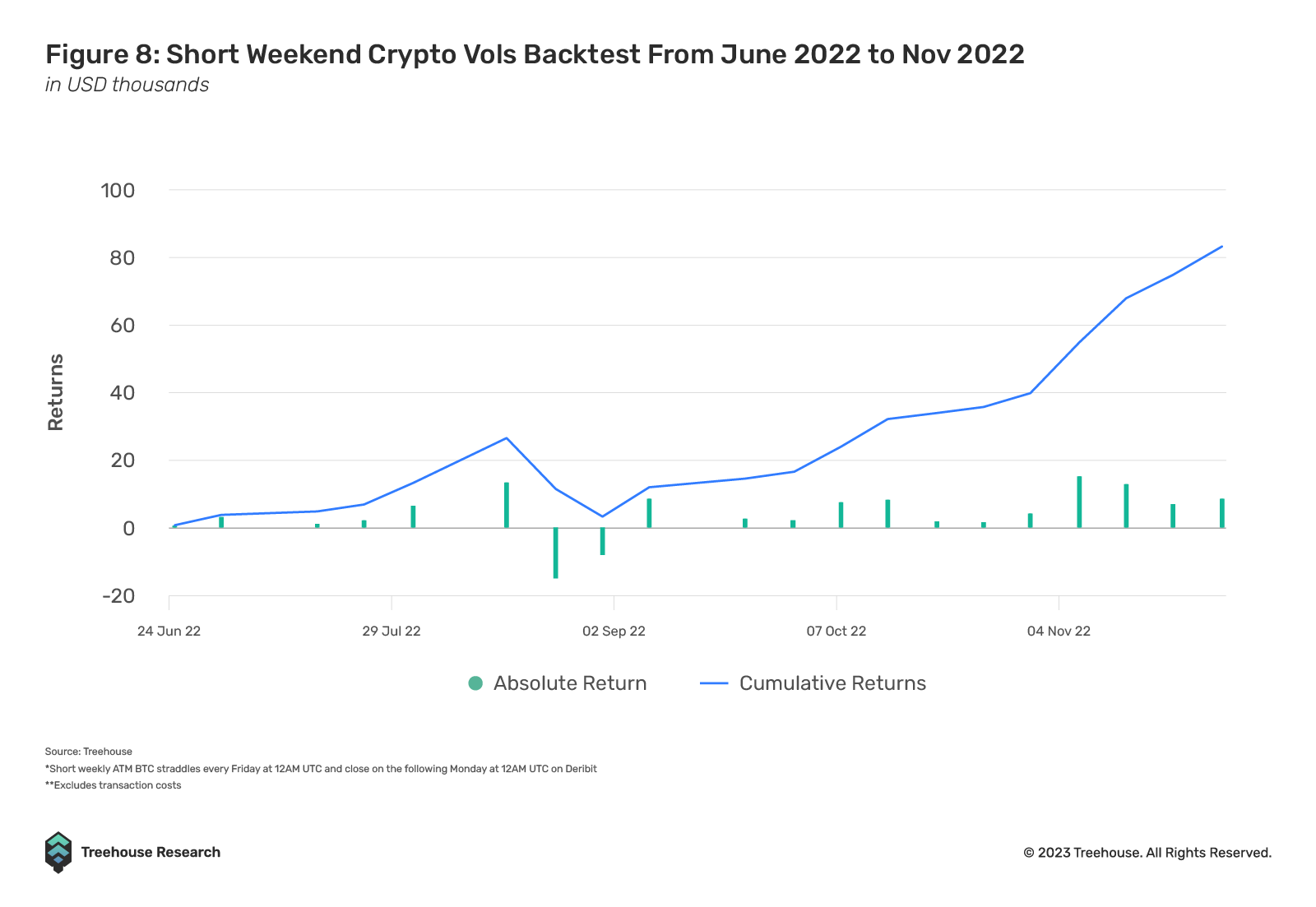

| Harvesting the Variance Risk Premium To capture the variance risk premium (VRP), traders can employ various strategies. One such approach involves selling at-the-money (ATM) straddles or strangles, allowing them to collect theta through time decay and vega through the subsequent decrease in IV. Additionally, traders can explore the concept of seasonality within the volatility complex to identify lucrative opportunities. For instance, they can leverage the low RV observed during weekends to initiate short volatility trades. Furthermore, traders have the opportunity to engage in front-running the flows of decentralized option vaults (DOVs), allowing them to sell volatility just prior to the auctions of options, which typically take place on Fridays (figure 8). |

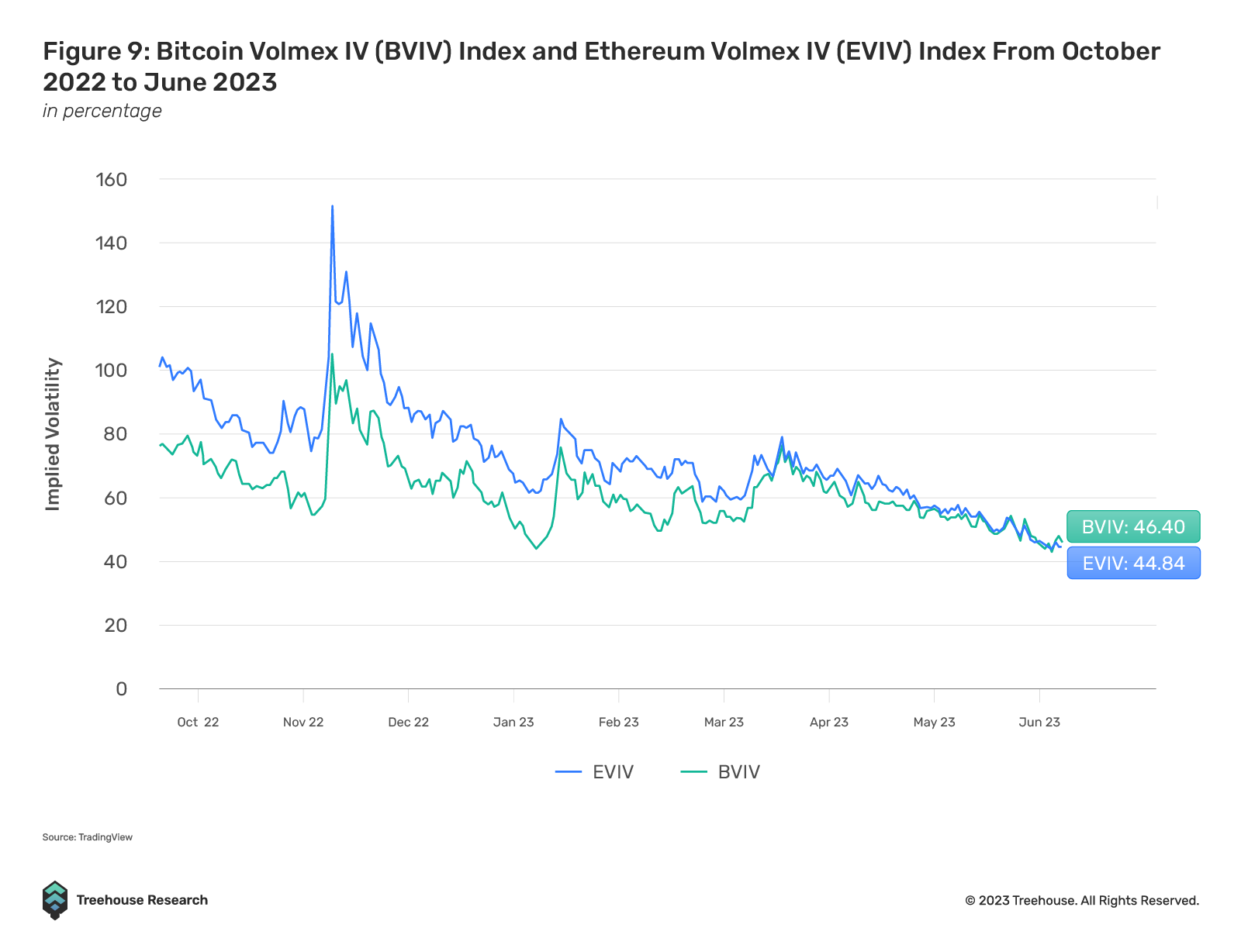

Crypto Volatility Reaches All-Time Lows

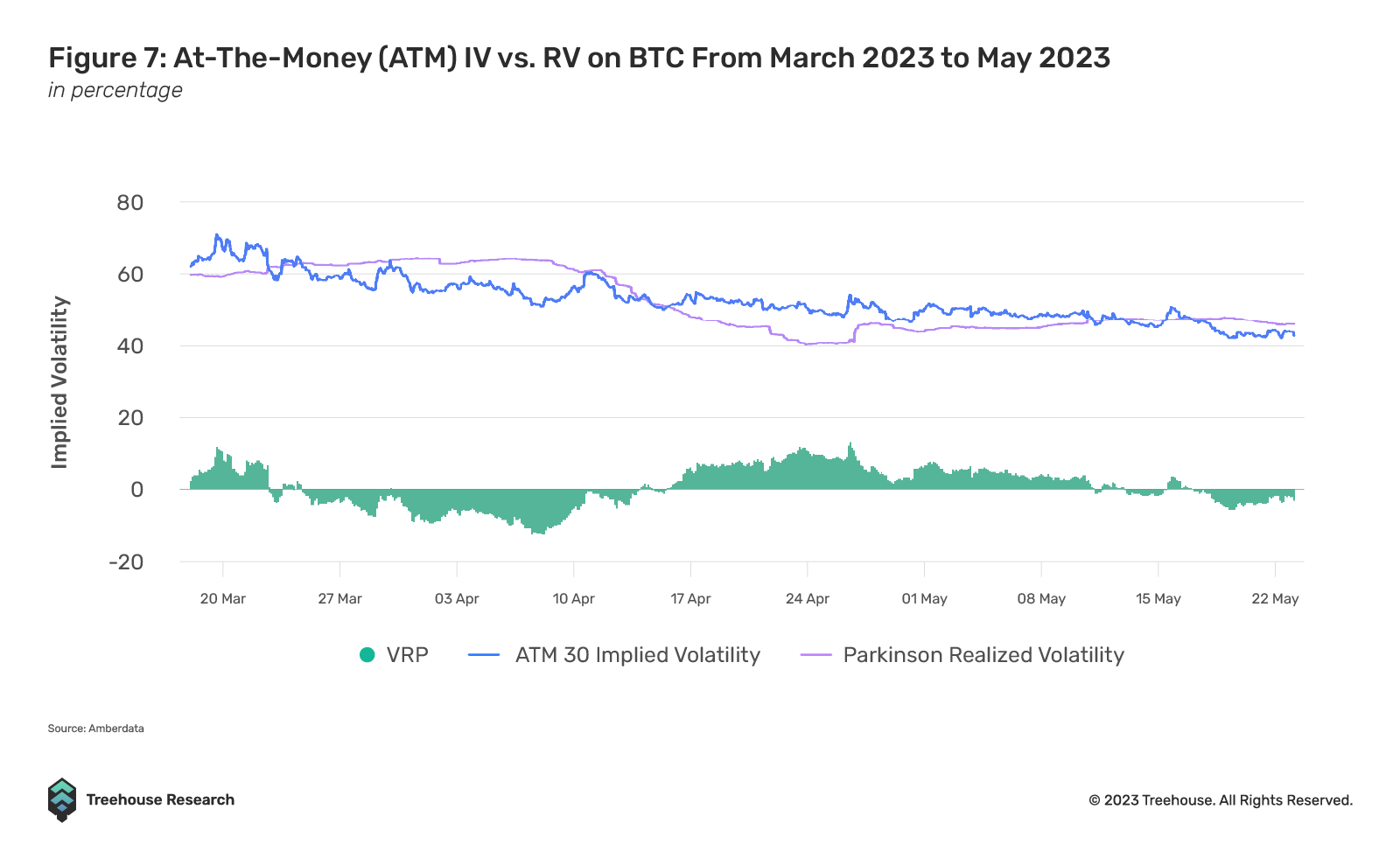

Since the beginning of 2023 however, selling volatility has become a tough gig due to a decline in overall implied volatility (IV), increasing the difficulty of harvesting the variance risk premium (VRP). Implied volatility has consistently decreased throughout this period, reaching historic lows of 46.40% and 44.84% for BTC and ETH, respectively (figure 9). Despite that, this phase of subdued volatility has opened up opportunities for traders to purchase longer-dated convexity in hopes of profiting from a volatility resurgence.

In DeFi, the opportunities available to express such trades lie in protocols like Volmex and Squeeth by Opyn. Both protocols allow users to buy or sell volatility directly via volatility-linked structured products. This will be explored further in part two of our options series when we delve deeper into the mechanism of these protocols.

Despite the emergence of volatility trading in the Crypto options space, options traders are represented only by the most experienced and knowledgeable of traders. Many of these traders are now exploring alternative strategies that go beyond directional biases, as commonly seen in the delta-one space.

Will Retail Traders Catch onto Options?

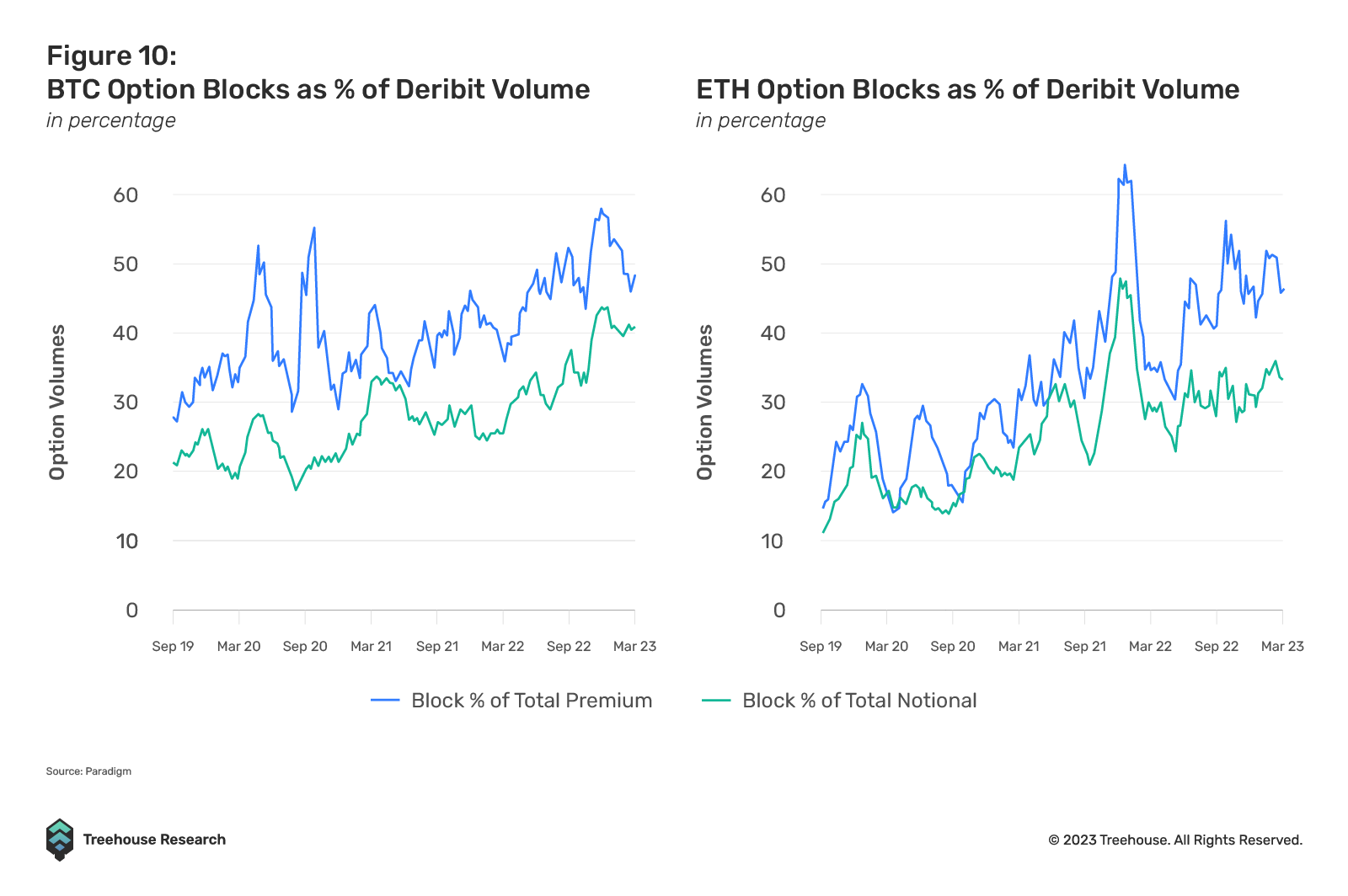

The Crypto options market remains predominantly driven by institutions and sophisticated traders. This becomes evident when we examine the growing presence of OTC market makers and the increasing block volume observed on centralized exchanges. Paradigm, a prominent institutional liquidity network for crypto derivatives reports that the proportion of block activity relative to the total option volume traded on Deribit has consistently risen from 2022 and continues to do so in 2023 (figure 10), highlighting the growing participation of institutional investors.

On the other hand, retail traders/investors have yet to make their mark in the Crypto options space. This becomes apparent given the fact that more than 90% of total Crypto options traded are on centralized entities such as Deribit and Paradigm, while only a fraction resides on DEXes.

There are two key factors impeding the adoption of crypto options among retail traders.

The Abundance of Leverage in Other Crypto Instruments

The first to consider is the contrasting availability of leverage between TradFi and the Crypto market. In TradFi markets, obtaining leverage is often a challenging endeavor. While some stock brokerages offer margin trading, the leverage factor tends to be significantly lower when compared to Crypto exchanges. The primary way to access substantial leverage in TradFi is through trading Contracts for Differences (CFDs), which are restricted in certain jurisdictions. As a result, risk-seeking investors often turn to options, particularly on zero-commission brokerages like Robinhood.

In contrast, the Crypto market offers abundant leverage opportunities. Numerous CEXs provide leverage of up to 50x on perpetual contracts, eliminating the necessity for retail traders to explore options for leverage.

The Lack of Altcoin Options in Crypto

The lack of altcoin options is another factor to consider, as current prominent option exchanges only offer deep liquidity for ETH and BTC options, which may be misaligned with the actual level of volatility within the Crypto market. For instance, lesser-known Cryptocurrencies and meme coins can easily double in a matter of hours, making options on these tokens appealing to risk-seeking individuals alongside perpetuals contracts.

Currently, it is still uncertain whether Crypto options will gain popularity amongst the retail community. Are retail traders inclined to navigate higher-order aspects such as volatility and skew? Do they truly require options for their pronounced convex payout when perpetuals and futures already fulfill their leverage needs at a significantly lower cost?

While institutions and sophisticated traders have embraced Crypto options extensively, it is clear that retail investors and traders have not yet displayed a strong inclination to incorporate them into their portfolio of instruments.

In part two of our series, we do a deep dive into the various decentralized finance models that enable Crypto options trades whilst spotlighting the emerging hurdles that impede the broad acceptance of on-chain options. Stay tuned to find out whether on-chain options have what it takes to usurp their CeFi counterparts. Meanwhile, subscribe to Treehouse Daily to get daily updates on the derivatives landscape, on-chain movements, technical analysis, and more! Keep your eyes peeled and do not miss out on this insightful exploration!

Disclaimer

This publication is provided for informational and entertainment purposes only. Nothing contained in this publication constitutes financial advice, trading advice, or any other advice, nor does it constitute an offer to buy or sell securities or any other assets or participate in any particular trading strategy. This publication does not take into account your personal investment objectives, financial situation, or needs. Treehouse does not warrant that the information provided in this publication is up-to-date or accurate.

Hyperion by Treehouse reimagines workflows for digital asset traders and investors looking for actionable market and portfolio data. Contact us if you are interested! Otherwise, check out Treehouse Academy, Insights, and Treehouse Daily for in-depth research.