Written with the QCP Capital Team

Written with the QCP Capital Team

In part 1 of our The State of Crypto Options piece, we explored the institutional and retail adoption of the sector: proposing that while institutions and sophisticated traders have embraced crypto options, retail investors have yet to join the party. Things felt unfinished, so our team at Treehouse took a deeper dive, traversing the major CeFi (Centralized Finance) and DeFi (Decentralized Finance) platforms offering crypto options today.

Our objective for part 2 is to determine which of the many option models would emerge dominant and whether DeFi options possess the necessary qualities to capture market share from CeFi. This study parallels the current scenario in the perpetual space, where DeFi perp DEXes are vying with CeFi counterparts for market share. Our analysis encompasses a comprehensive examination of the advantages and limitations presented by each DeFi and CeFi option model, aiming to ascertain their respective potential for meaningful adoption.

Crypto Options: Models and Exchanges

Across CeFi and DeFi platforms today, three models are used to facilitate options trading:

(1) Central Limit Orderbook (CLOB),

(2) Single Vault AMMs, and

(3) Pooled Vault AMMs.

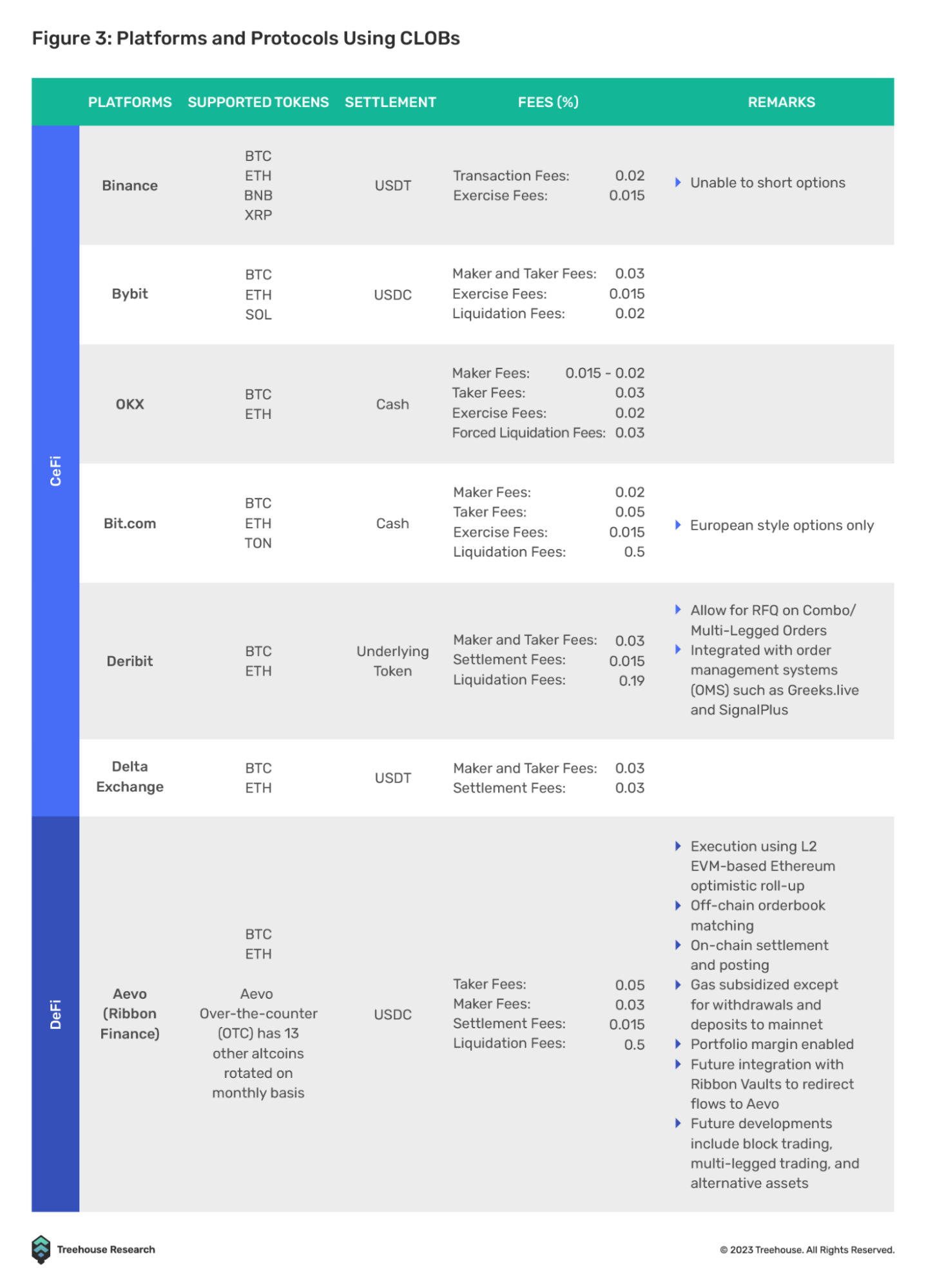

Central Limit Orderbook (CLOB)

A CLOB is a trading execution method common in equities that matches buy and sell orders based on price, time, and quantity. The main advantage of CLOB lies in its ability to consolidate orders from multiple participants, resulting in increased liquidity, a higher probability of finding a counterparty, and narrower bid-ask spreads.

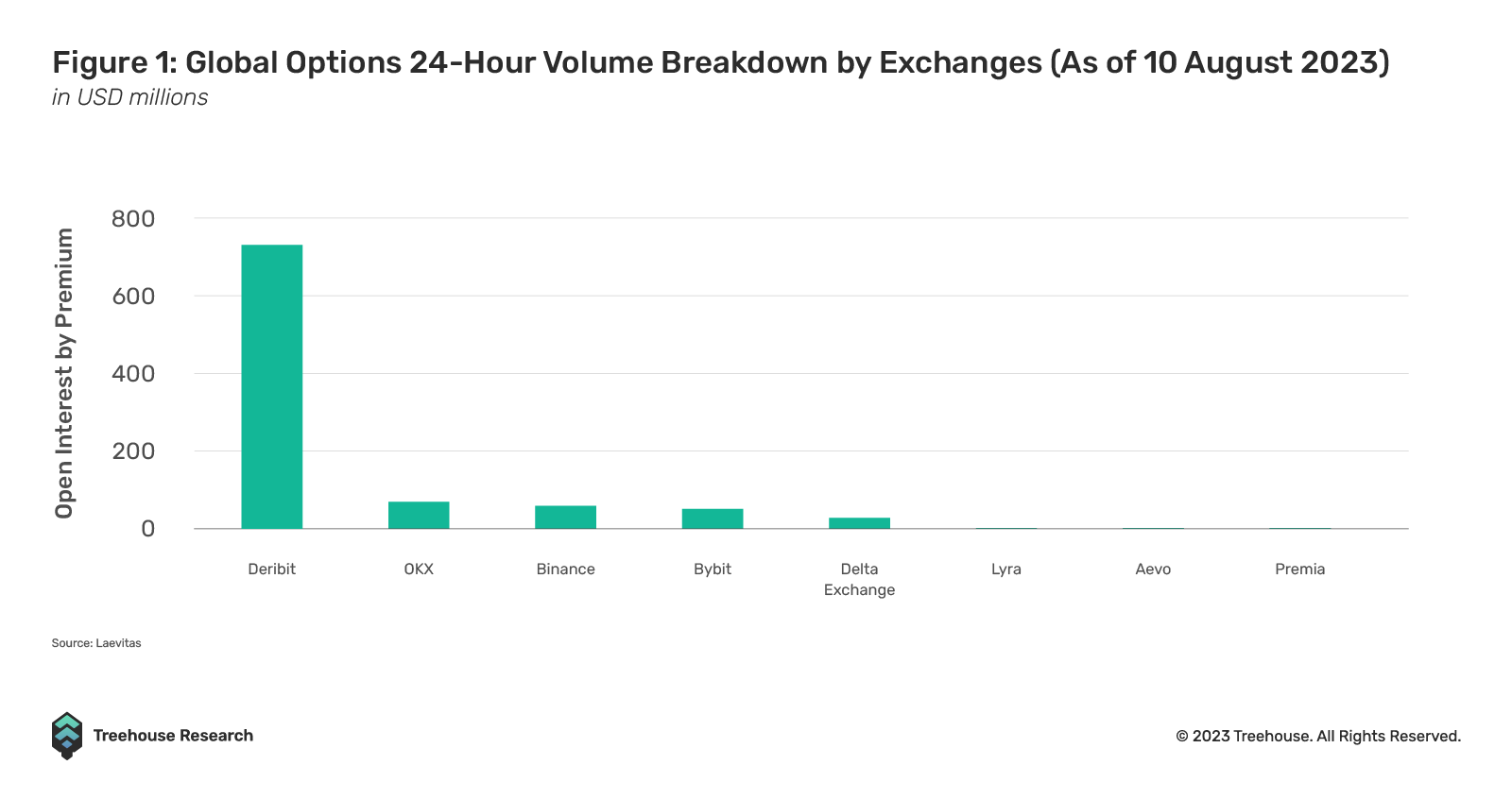

| Today, most CLOBs are used by CEXes, such as Binance and Bybit. However, Deribit accounts for over 90% of the total options volume in the space, singlehandedly dominating the crypto options realm since 2016 (Figure 1)! |

Despite the benefits of CLOB, traders are vulnerable to counterparty risks as most CLOB systems are centralized. Furthermore, traders may experience challenges executing orders during increased volatility as market makers on CLOBs have complete discretion to widen bid-ask spreads.

At present, Aevo is the only exchange that uses the CLOB model in a decentralized manner. Aevo, introduced in April 2023, stands as a DeFi options exchange established by Ribbon Finance, a prominent figure in the realm of Decentralized Options Vaults (DOVs). Since its official launch. Aevo has rapidly risen to prominence in the DeFi landscape, establishing a leading position in terms of trading volume. Notably, Aevo has pioneered an ingenious off-chain matching system that facilitates on-chain settlements. However, it is worth noting that despite these advancements, Aevo’s CLOB implementation still hinges on centralized market makers for the provision of platform liquidity. |

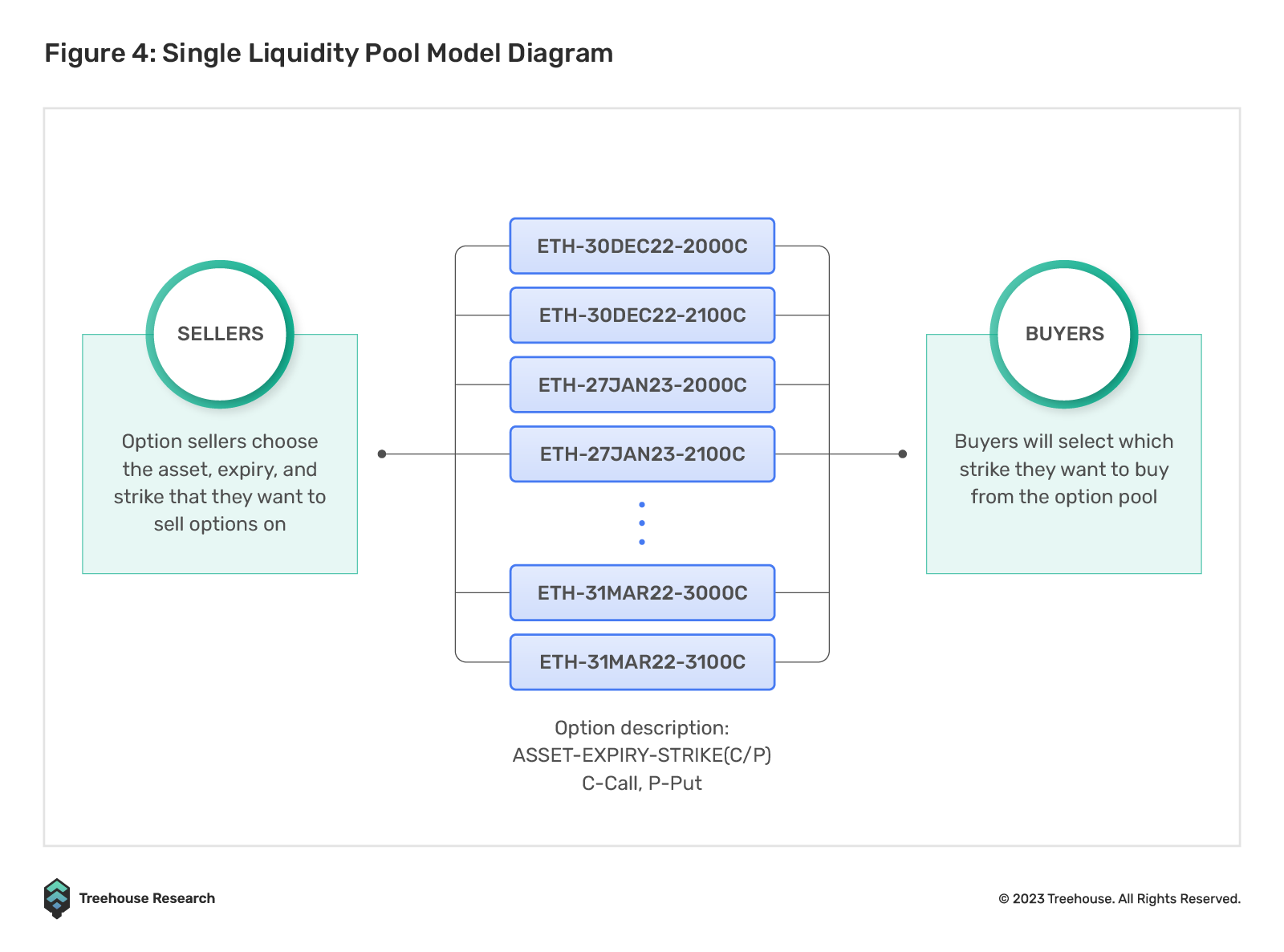

Single Vault AMMs

Single Vault AMMs work similarly to DOVs in that users deposit funds into a vault that acts as a counterparty to the option buyers. The primary distinction between Single Vault AMM and Pooled Vault AMM is that the former is limited to a single strike level and expiry, whereas the latter encompasses all available strikes and tenors.

Single Vault AMMs offer two key advantages. First, liquidity providers can manage risk by choosing their desired strike prices and expiration dates, enabling them to customize positions based on risk tolerance and market expectations.

Second, option buyers are able to enter positions without slippage since there are no bid-ask spreads and fair prices are determined based on pricing models used by the protocol. This also means that anyone with sufficient capital can purchase the entirety of available liquidity on a vault at the same price.

A major drawback to Single Vault AMMs, however, is liquidity fragmentation. Due to its design, liquidity in this model is fragmented across various strikes and tenors, leading each pool to have its unique APY, utilization rate, and supply.

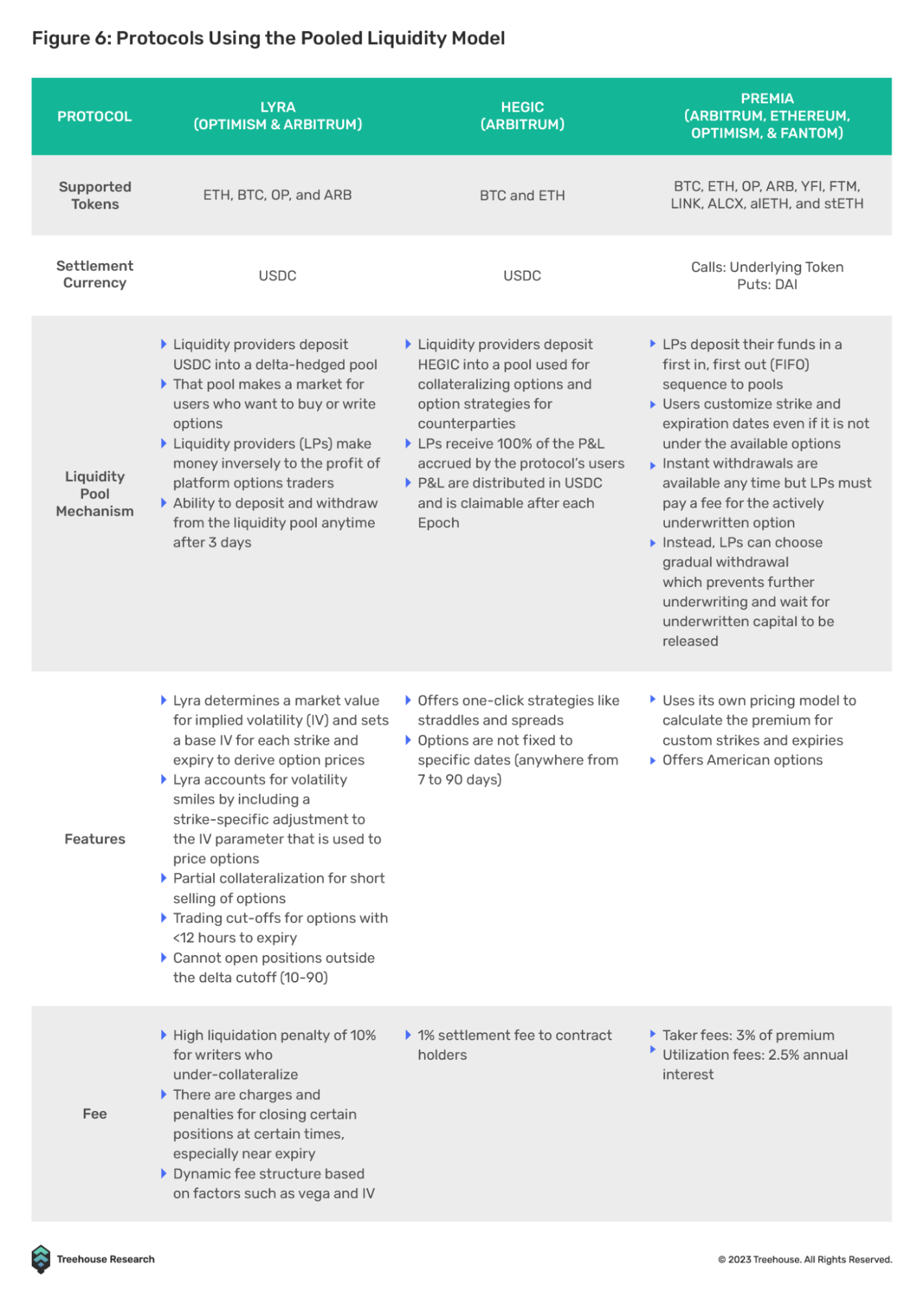

| Currently, Dopex is the most well-known on-chain option protocol that uses the Single Vault AMM model. Built on Arbitrum, Dopex offers options on various tokens, including ARB, BTC, CRV, CVX, DPX, ETH, GMX, GOHM, MATIC, RDPX, and stETH. Liquidity providers participating as option writers receive incentives through DPX or rDPX tokens. Dopex also offers other innovative products, such as Atlantic Options and Insured-Perps, and has formed partnerships with protocols like JonesDAO and DeFi derivative heavyweights like GMX. |

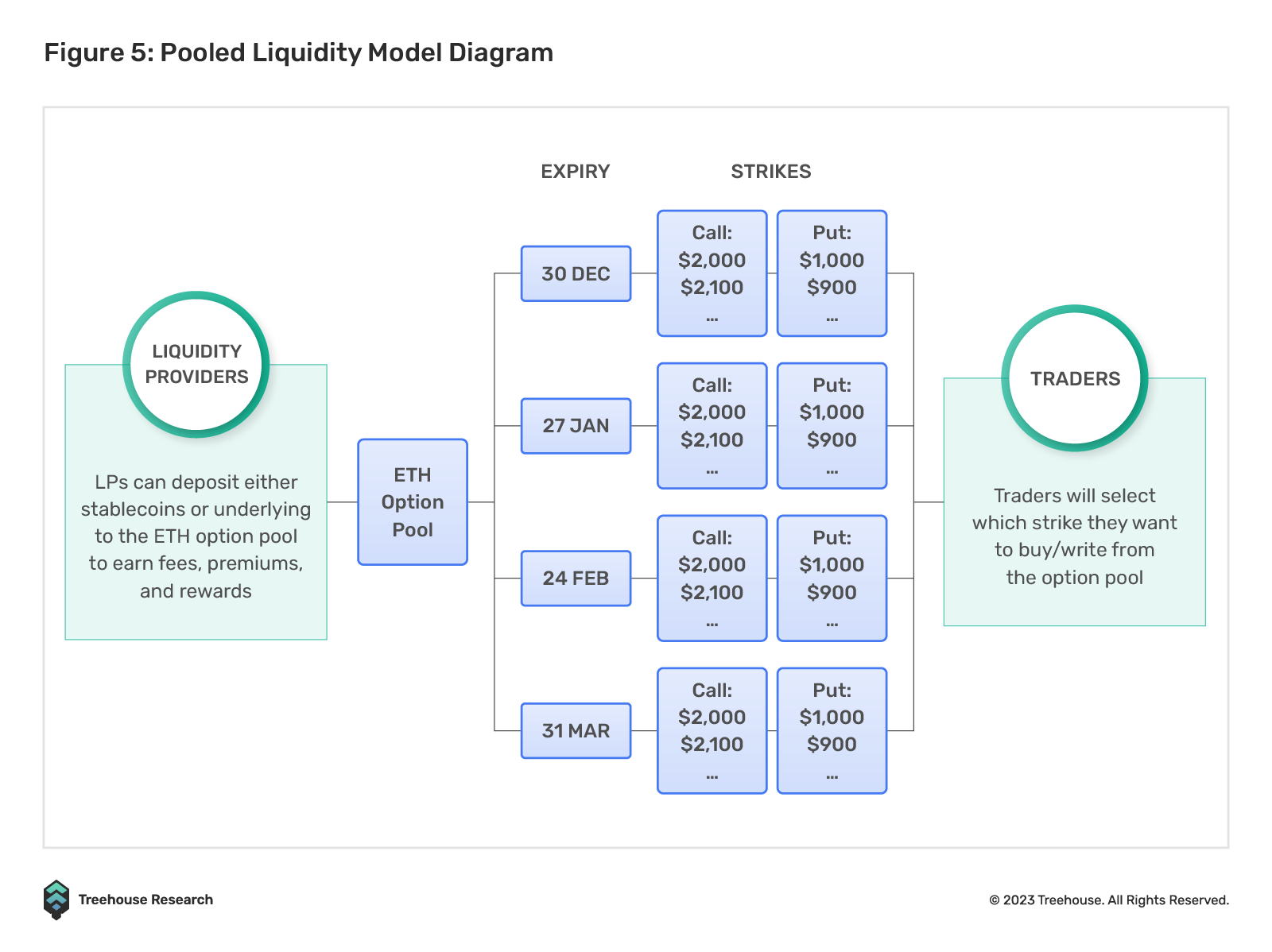

Pooled Vault AMMs

Lastly, Pooled Vault AMMs enable liquidity providers to serve as counterparties for all options trades related to the respective token and are not limited to specific strikes or tenors. Vaults can write both calls and puts or have separate pools depending on the protocol. Combined pools typically accept only stablecoins, while separate liquidity vaults require an underlying asset as collateral for the call pool and stablecoins for the put pool.

The concentrated liquidity of the Pooled Vault AMM model has a significant advantage compared to the Single Vault AMM model in that liquidity is not fragmented.

The simplicity of the model also benefits liquidity providers who prefer a hands-off approach to yield generation. LPs can deposit their assets into the pool and let the market take care of the rest without actively defining risk tolerance.

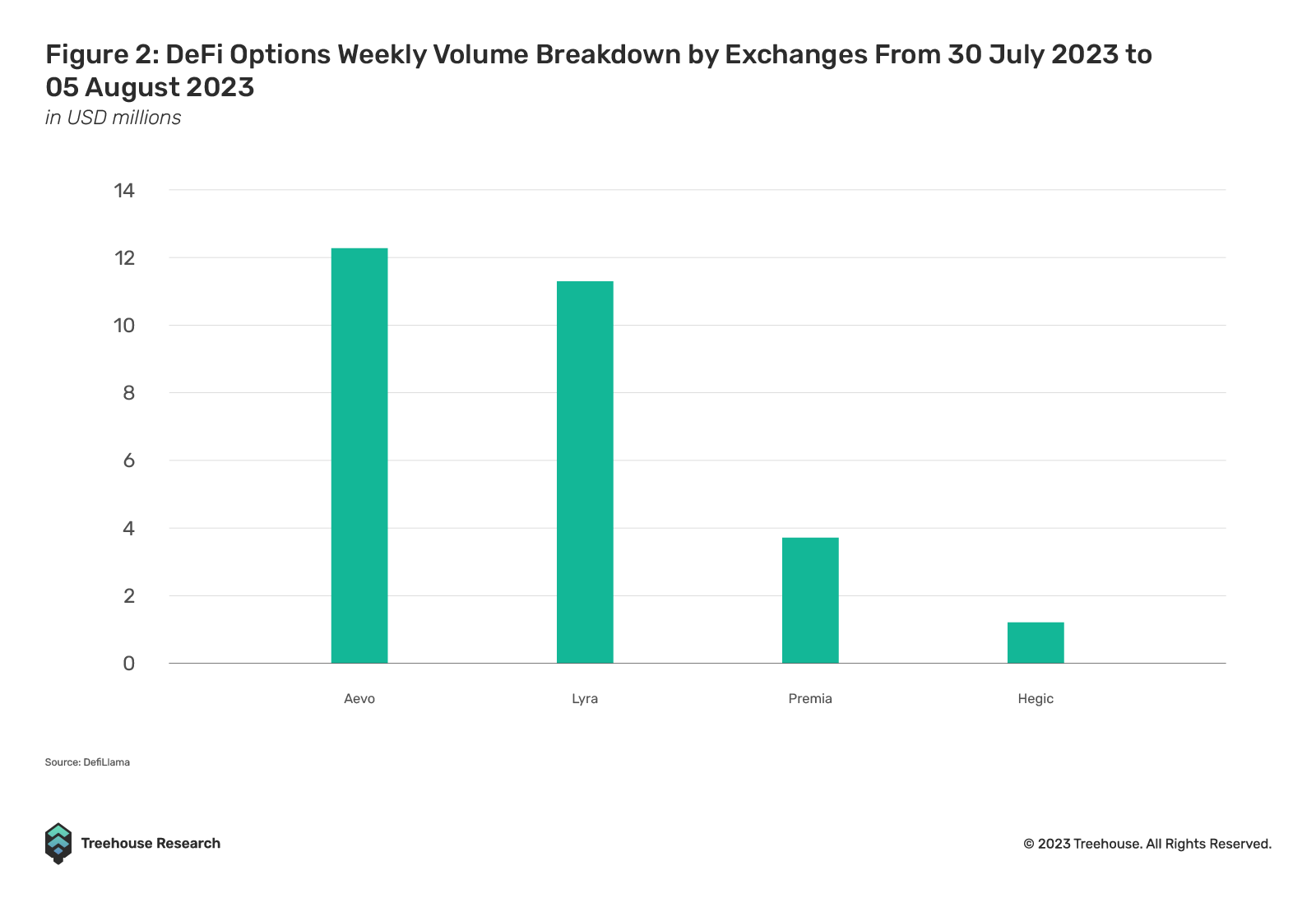

| Currently, Lyra stands at the forefront as the premier DeFi option protocol, excelling in both Total Value Locked (TVL) and trading volume through its pooled liquidity model. Boasting an impressive TVL of $27 million, Lyra outpaces Dopex, which secures the second-highest TVL among option protocols at $22.85 million. In terms of trading volumes, Lyra also emerges as the market leader with over 3.5 times the volume of Premia, its closest rival utilizing a pooled liquidity model for options trading. Lyra’s platform encompasses diverse options, including those linked to ETH, BTC, OP, and ARB tokens, all of which are settled in USDC. Moreover, Lyra has established close integration with protocols on Optimism and Arbitrum networks, such as SNX and GMX. This integration enables automated delta-hedging of the liquidity pools by capitalizing on the perpetuals offered by these protocols. |

Out of the three models, the Single Vault AMM and Pooled Vault AMM are the most heavily used in DeFi.

Are DeFi Options ‘there’ yet?

In the spot and perpetual space, DeFi is slowly catching up to CeFi in terms of trading volume thanks to the emergence of prominent platforms like GMX and dYdX. When it comes to options, CeFi options still maintain a dominant position in terms of volume and open interest. At present, DeFi options are still in their early stages, and the prevailing model that will reign supreme is yet to be determined. Our analysis reveals that the primary challenge for DeFi options lies in the fragmentation of liquidity and the inflexibility faced by liquidity providers. As a result, DeFi options have yet to gain significant traction from the public.

Fragmented Liquidity

Inability to support large sizes

Single Vault AMMs experience liquidity fragmentation across various strikes and tenors. This often means that options with lower liquidity may not have sufficient liquidity for buyers. For example, an at-the-money put option may have less liquidity compared to an out-of-the-money option as liquidity providers are more inclined to write options that have a lesser probability of settling in-the-money. As a result, institutions or traders with larger size requirements on specific strikes prefer to trade on CLOBs with deep liquidity or through over-the-counter dealers.

Giving up variety for the sake of liquidity

Due to fragmented liquidity, protocols that adopt the Single Vault AMMs typically have minimal strikes and tenors to choose from. For example, Dopex option vaults only allow buyers to choose from four strike levels. Additionally, most DeFi option protocols only offer expiries with no more than 90 days. This starkly differs from traditional CLOBs that typically offer more than 12 strike levels and expiries of up to 1 year.

Inflexibility for Option Writers and Liquidity Providers

LPs cannot define risk exposure

In Pooled Vault AMMs, liquidity providers (LPs) act as the counterparty to all option transactions. However, LPs cannot specify their risk exposure, unlike CLOBs, where option writers have more control over strike and tenor selection based on their market outlook or risk tolerance. The lack of control exposes LPs to the risk of significant losses if an informed trader makes a large winning trade on the pool. Furthermore, LPs in such protocols face the challenge of writing options without knowing at what spot price or implied volatility the option is being written, making effective hedging difficult.

LPs must make a balancing decision

For Single Vault AMMs, each strike pool has its own APY and utilization rate. A higher utilization rate results in a higher APY for liquidity providers (LPs), while a lower utilization rate leads to a lower APY. This poses a challenge for LPs, who must balance the desire for higher returns with their risk tolerance. Writing options closer to the At-The-Money (ATM) strike price attracts more demand and higher premium payments, but it comes with associated risks such as gamma. Conversely, options that are further out of the money carry lower risks but offer lower yields in terms of option premiums. In contrast, option writers on a Central Limit Order Book (CLOB) receive a premium based on the fair value of the contracts, which is determined by their parameters.

LP’s capital can be locked up indefinitely

In a similar vein, LPs may face the challenge of having their entire capital locked up indefinitely if the pool utilization remains consistently at 100% and users continuously open or roll positions. This limits LPs’ flexibility and hampers their ability to allocate capital to other trading opportunities.

Ideally, LPs prefer 100% utilization in a liquidity pool to generate maximum returns. However, maintaining full utilization means LPs cannot withdraw their capital, and if options become excessively overpriced, buyers may seek alternatives elsewhere. Conversely, if pool utilization falls below the optimal level, returns from writing options are limited, and LPs may find it more advantageous to manually sell their options on CLOBs and delta-hedge them in other markets.

Does this spell the end for DeFi Options?

At first glance, this looks like the end for DeFi Options, or at the very least, the Single and Pooled Vault AMM models. However, DeFi options still have a very strong edge over their CeFi counterparts in terms of product innovation and speed-to-market.

DeFi offers a wider variety of altcoin options

In part 1 of our article, we mentioned the lack of altcoin options as a barrier to retail adoption. Compared to its CeFi counterpart, DeFi option protocols offer a wider variety of altcoin options (barring OTC market makers).

A key reason why market makers on centralized CLOBs are reluctant to provide option liquidity on a wide range of underlying tokens is because of the challenge of hedging. This is especially true when market makers are unable to find enough liquidity from other sources. Unlike benchmarks like BTC and ETH, many altcoin tokens have a short market history. The lack of data and price volatility associated with these tokens makes it difficult for market makers to accurately price options. Additionally, the longer-tailed characteristics of such altcoins may deter market makers from providing liquidity.

While CeFi platforms usually limit their option offerings to BTC and ETH, DeFi protocols like Premia and Dopex provide a broader range of options, including altcoins like GMX, ARB, LINK, and more. DeFi protocols leverage the AMM model, which facilitates faster liquidity provision and enables the creation of diverse option markets.

Innovation is widespread in DeFi options

Blockchain and smart contracts truly fuel boundless innovation, and DeFi options exemplify this notion. While CeFi platforms have largely stuck to standard options trading, limited to buying and selling vanilla or multi-legged options, the DeFi options landscape presents a plethora of innovative products built upon the foundation of options.

As a case in point, both Volmex and Squeeth offer traders the ability to directly trade volatility through volatility-linked products, which is not commonly seen on CeFi platforms today. Moreover, DeFi perpetual options are gaining traction, with Panoptic leading the charge. Panoptic is pioneering options that are built on top of Uni-V3, veering away from conventional models as described in earlier parts of this article. An additional noteworthy example is Dopex’s Insured Perps, an offering that enables users to acquire ‘Atlantic Puts’ to safeguard leveraged long positions on GMX. These innovative advancements highlight how DeFi options may surpass the traditional offerings found in CeFi platforms, pushing the boundaries of what is possible in the options market.

Lyra, one of the most prominent figures in the DeFi options space, has also recently unveiled its plans for Lyra V2. According to the proposal, Lyra V2 is set to launch on the Lyra Chain, a tailored L2 solution built using the OP stack. Following the precedent set by Aevo, Lyra aspires to become the second decentralized protocol offering Central Limit Order Book trading for spot, perpetuals, and options, all within a modular and permissionless framework. Notable improvements encompass an intuitive user experience, advanced risk management capabilities, heightened capital efficiency, and robust security mechanisms. Through its integration with the Optimism Superchain, Lyra V2 ultimately envisions itself as a versatile and composable derivatives liquidity layer, cultivating a dynamic ecosystem for DeFi derivatives while remaining poised for institutional adoption.

Stable or Tokened-Margin? You Choose

DeFi options hold a distinct advantage over centralized platforms in terms of its flexible margin system offered to traders. Deribit, for instance, only provides support for fiat or stablecoin margin for perps and mandates users to collateralize their trades with BTC for BTC options or ETH for ETH options. As a result, there is sometimes an extra step for users seeking to minimize fluctuations in token exposure and it also adds an additional layer of execution risk.

DeFi protocols like Aevo, Premia, Hegic, and Dopex, on the other hand, allow users to post collateral in stablecoins or in the underlying token.

| Token-margined options… the Good and the Ugly Imagine this scenario: You hold a bearish view on ETH and decide to buy an ETH put option. For token-margined options, the collateral, premium, and option price are all denominated in ETH. As a result, the payout of the option will be heavily influenced by the price of ETH, which will be lesser in dollar terms as compared to dollar-margined options. In an extreme case where you purchased LUNA put options prior to the crisis in May 2022: If the option’s payout was in LUNA instead of USDC, the profits from the LUNA put option would essentially have evaporated. On the flip side, token-margined options can also bring significant upsides. In the case that you decide to purchase a call option on ETH, and then ETH rallies afterward. Both your collateral and profits increase in dollar terms. In essence, token-margined options can significantly skew both the upside and downside potential, giving rise to non-linear payouts. For more sophisticated traders, shorting the underlying collateral using Perps to get whichever exposure they are keen on having also works! |

Despite the inherent drawbacks of DeFi options due to their unique model, it’s clear that there are aspects where DeFi outshines its CeFi counterparts.

The Future of Crypto Options

The landscape of crypto options is still in its early stages, with retail adoption yet to reach its full potential. While DeFi options may currently lag behind their CeFi counterparts in some ways, there is a significant amount of innovation happening within the DeFi space that could potentially revolutionize the industry.

Just as Uniswap revolutionized the AMM model to compete with traditional spot order books on centralized exchanges, new players within the DeFi crypto options space are striving to introduce novel approaches and features to attract traders and investors.

The minimum viability for any DeFi option model requires robust liquidity across multiple cryptocurrencies, even for assets with varying tenors ranging from weekly to yearly options. Traders and investors seek a platform that not only offers flexibility but also possesses the ability to facilitate complex strategies while maintaining robust liquidity.

Additionally, a strong reason to remain optimistic about DeFi options lies in their utilization of smart contracts and settlement layers, eliminating the necessity for centralized clearinghouses and exchanges.

While this analysis takes a critical perspective, we acknowledge the invaluable contributions of the pioneers who have paved the way for crypto options. It is with the benefit of hindsight that we draw these conclusions, which would have been challenging to reach without their groundbreaking efforts. Nonetheless, we maintain an optimistic outlook and envision DeFi options as potentially emerging as one of the leading categories in the forthcoming cycle.

Disclaimer

This publication is provided for informational and entertainment purposes only. Nothing contained in this publication constitutes financial advice, trading advice, or any other advice, nor does it constitute an offer to buy or sell securities or any other assets or participate in any particular trading strategy. This publication does not take into account your personal investment objectives, financial situation, or needs. Treehouse does not warrant that the information provided in this publication is up-to-date or accurate.

Hyperion by Treehouse reimagines workflows for digital asset traders and investors looking for actionable market and portfolio data. Contact us if you are interested! Otherwise, check out Treehouse Academy, Insights, and Treehouse Daily for in-depth research.