Introduction

Under the sweeping “Real Yield” narrative, undercollateralized lending income has become increasingly studied and sought after in DeFi. Acknowledging the wonderful existing coverage on this topic in crypto media, we, at Treehouse Research, would also like to share our thoughts on a couple of different perspectives.

In this article, we will start by looking at what credit is, and why it is important to economies and businesses. Then, study the prevailing DeFi credit protocols, as well as their pros and cons compared to TradFi/CeFi lending. We will wrap up with a few points we think will be pivotal to the next stage of growth in DeFi credit markets.

Credit: The Modern Way of Borrowing and Lending

Borrowing and lending are among the oldest socio-economic behaviours in human society, dating back to ancient Mesopotamia. Ancient lending started in the form of pawnbrokers, which were simply loans collateralized by objects deemed with value. Early forms of credit emerged as resource owners lent production materials to labor workers and expected repayment of goods. If the borrower fails to pay, he risks his family being taken as slaves.

Nowadays, credit is important for businesses and entire economies because it allows economic units to leverage up working capital without diluting equity ownership. Such leverage leads to boosted investment, capital expenditure, and consumption, thus, leading to overcharged economic growth.

In TradFi, credit can generally be broken down into secured and unsecured credit. A mortgage is a type of secured credit, as the loan is collateralized by the property. A credit card is a type of unsecured credit, or one can regard it as being collateralized by the creditworthiness of the borrower. Credit creation means balance sheet expansion. For example, in a typical mortgage, a buyer puts down a 10-50% down payment for the market value of a property and finances the rest from banks. The differential between the property value and the down payment is credit created by commercial banks. In a grander scheme, the Fed purchases US Treasury bonds, an act of borrowing from the US federal government – that is credit created by the Fed (central bank) to a sovereign state (government).

In DeFi, on the contrary, the majority of existing lending protocols are based on an overcollateralized basis, similar to pawnshops’ lending style, which does not involve creating credit. An equivalent to overcollateralized mortgage in DeFi would be if Elon Musk had to put down US$1B worth of Tesla shares to borrow US$500M for a villa – not very attractive to someone who already owns US$1B because he could easily find a bank willing to lend him US$10B.

Credit as a Business Financing Channel

Two forms of financing are available for a traditional business: debt financing and equity financing. Equity financing involves diluting ownership, and founders avoid this especially during the early stages to avoid losing out on equity upside. Equity financing does not create credit because the business sells “part of itself” in exchange for cash.

To maintain majority control over their operations and business decisions while raising working capital, businesses opt for debt financing. Debt financing creates credit as lenders provide cash or other working capital in exchange for future repayment of principal plus interest, rather than a controlling stake. Lenders also avoid taking equity risks as they will have claims on the assets of the borrowers while equity holders do not. This form of financing or loan is usually available after a business, or a company manages to clear all the requirements that financial institutions impose.

What’s Stopping Credit Creation in DeFi?

As mentioned earlier, DeFi borrowing and lending still largely follow the ancient pawnshop model – borrowers put down something of value as collateral, and take out cash less than or equal to the collateral’s value. This is ultimately because DeFi lending and borrowing protocols are permissionless, which is efficient procedurally and resistant to prejudice against any borrowers. However, this hampers the pre-lending credit check and Know-Your-Customer (KYC) procedures that usually precede credit origination in the TradFi world. Since mainstream DeFi lending protocols lack the means to know the true identity of the borrowers and assess their credit risks, they are left with overcollateralization as a way to ensure that lenders are always made whole.

Overcollateralized loans enable many trading and hedging strategies for financial sectors. Since they do not create credit, their use cases for non-financial businesses are limited because only asset-owners can borrow, while the have-nots cannot leverage up. Even for the asset owners, there are more efficient ways for them to leverage up than to participate in DeFi borrowing. For instance, someone with US$10M worth of crypto assets might be able to borrow US$20M from a CeFi institution that conducts KYC and credit checks. Essentially, the core DeFi principle of being permissionless prevents DeFi lending markets from growing.

Burgeoning DeFi Credit Protocols

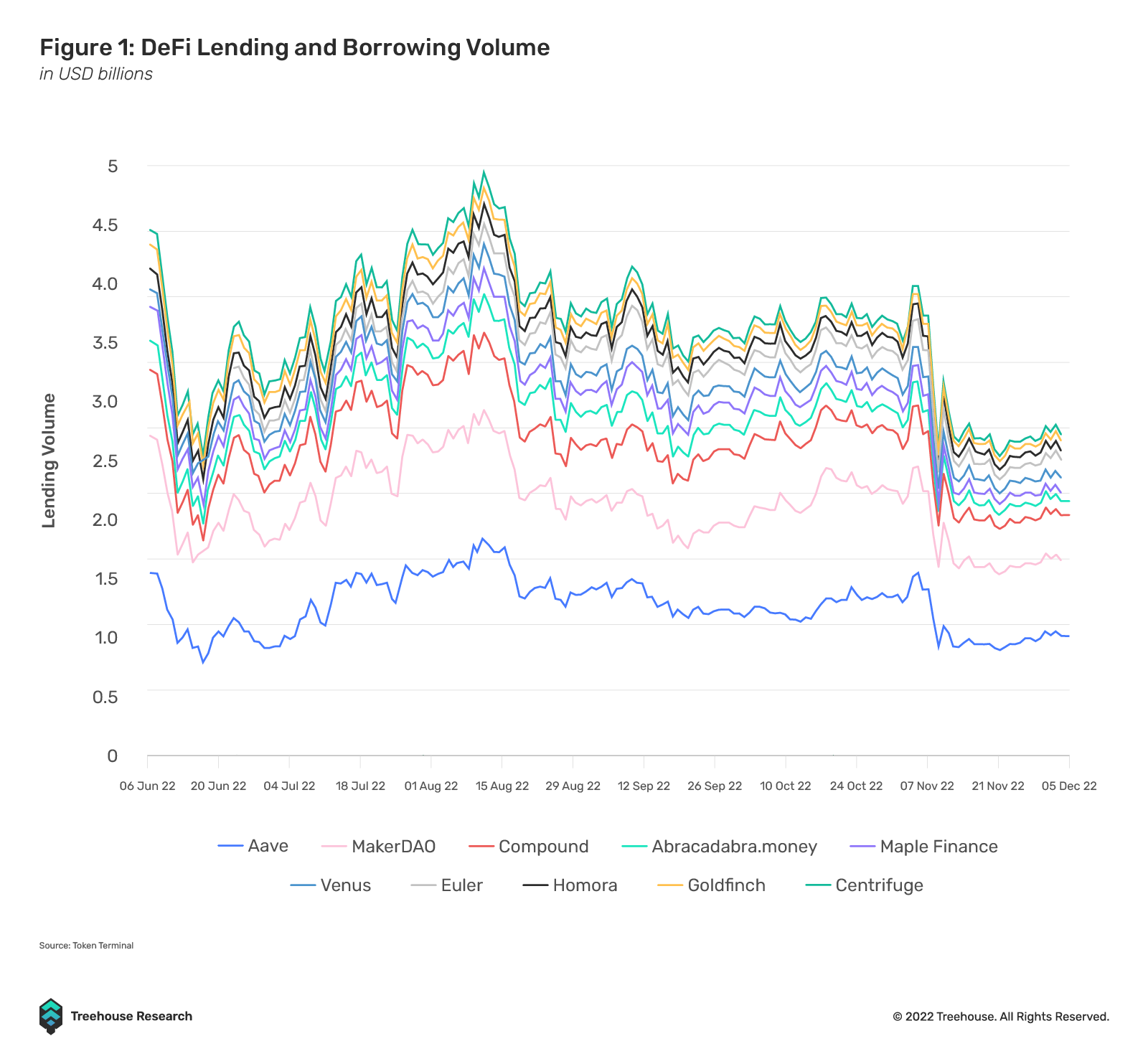

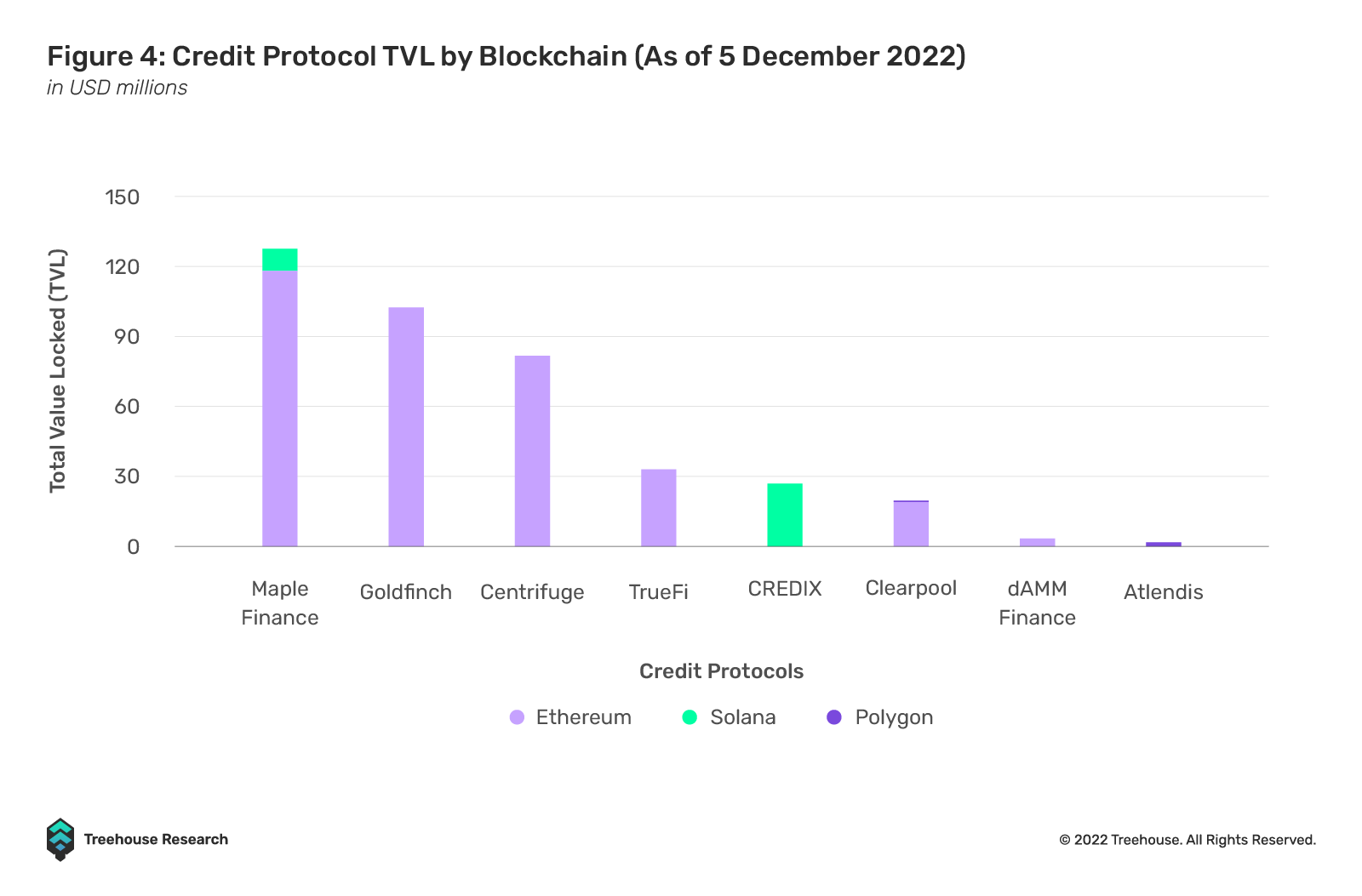

Currently, DeFi lending protocols have a cumulative TVL of US$13.96B as of 5 Dec 2022, with monthly borrowing volume ranging from US$9.37B to US$32.46B over the past year. Although this figure has been holding steady even during recent market contractions, the size of this money market still pales in comparison to that of TradFi markets.

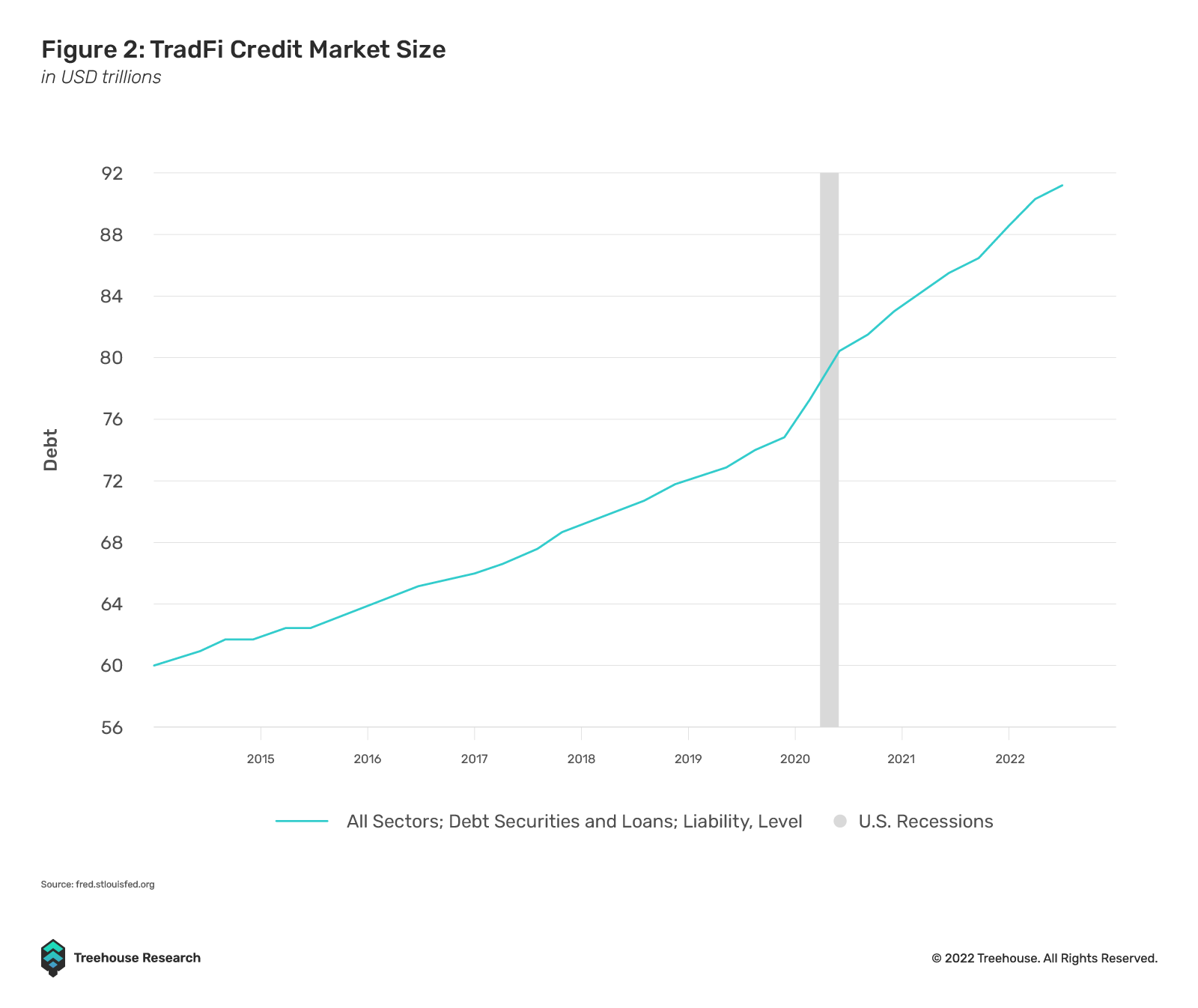

Credit markets in TradFi have a size of around US$91T, magnitudes larger than TradFi equity markets and DeFi money markets. This is largely due to the capital inefficiency and lack of means to assess and price credit risks in DeFi.

The introduction of credit protocols to the DeFi space has sparked heavy interest from institutional borrowers and lenders alike, especially during a period when liquidity in the global financial system is being drawn out by central banks.

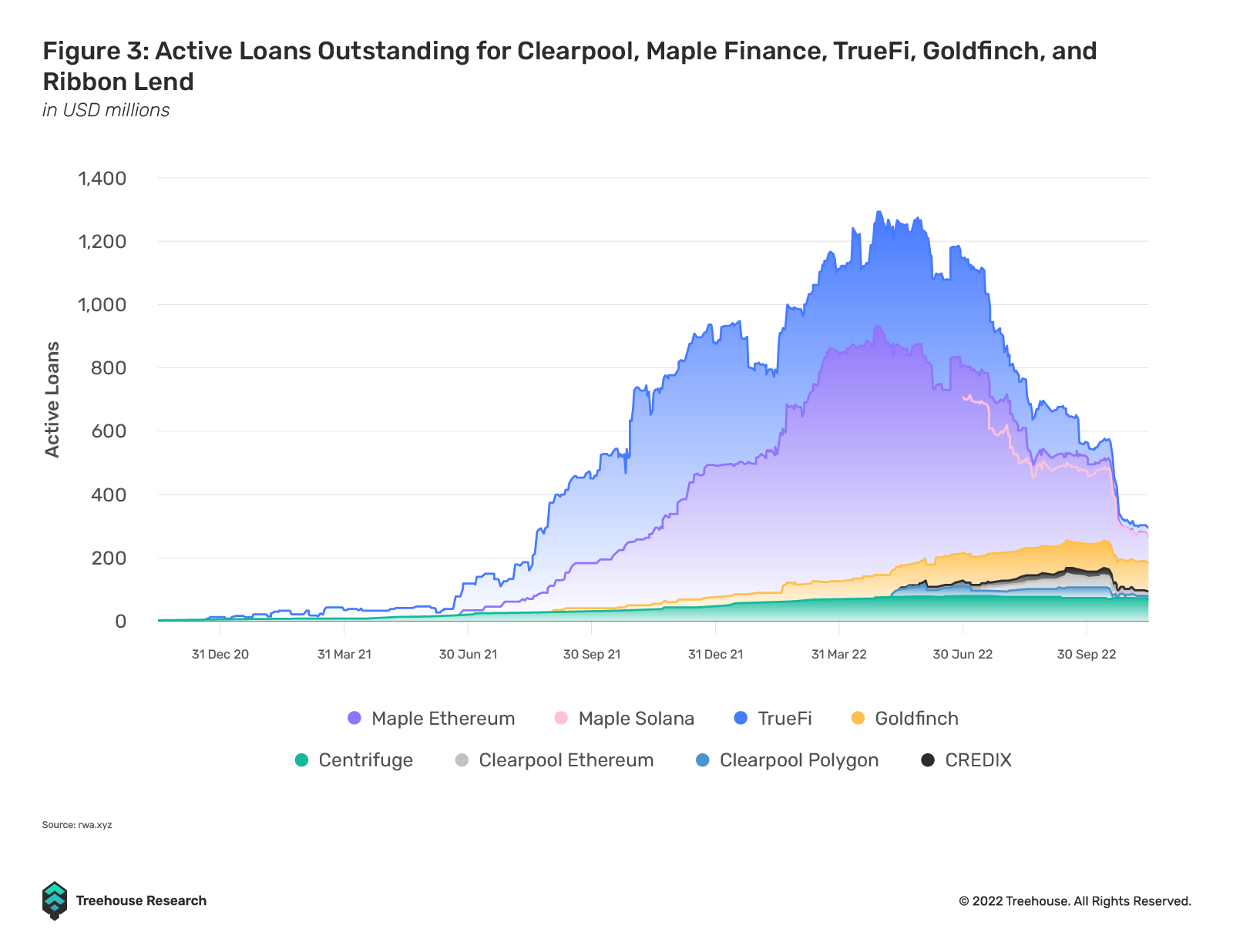

Credit protocols have originated a total of US$4.2B in loans for 2022, and there has been an increase in institutional borrowers.

Moreover, the defaults of large CeFi lenders like Celsius have led to overall credit contraction in the crypto financial sector, as CeFi lenders’ risk appetites have reduced, leaving crypto institutions with fewer options to obtain credit. Therefore, the emerging DeFi credit protocols can scoop up the market share vacuum left behind. For example, Maple Finance noted in its Q2 report that lender demand has remained strong throughout the year, with 23% of lenders having increased lending positions and increased appetite for capital from borrowers. Clearpool has also reported its total liquidity provided peaking at US$145M in September 2022, a 30% month-on-month increase in contrast to a broader TVL drop of 26.7% in DeFi. The outsized growth of DeFi’s credit origination generally corresponded with the CeFi credit crisis.

DeFi Credit Protocols’ Business Models

Most DeFi credit protocols currently do not directly originate loans, but rather, act as credit infrastructure providers by connecting borrowers and lenders. The main source of revenue for these credit protocols is similar to that of their overcollateralized counterparts, which is a share of interest revenue from outstanding loans. Once the onboarded institutions start originating loans, these credit protocols typically either take a percentage of the interest revenue generated from these loans, or charge a small fee at the point of loan origination. For example, Clearpool utilizes the model of pooling and lending of capital, and it takes 5% of all interest payments collected as a protocol fee. Protocols that run lending business set-up models, similar to Maple, charge a 1% establishment fee when loans are originated by any of the institutions with pools on their platform. 67% of this fee is sent to the Maple DAO as protocol revenue.

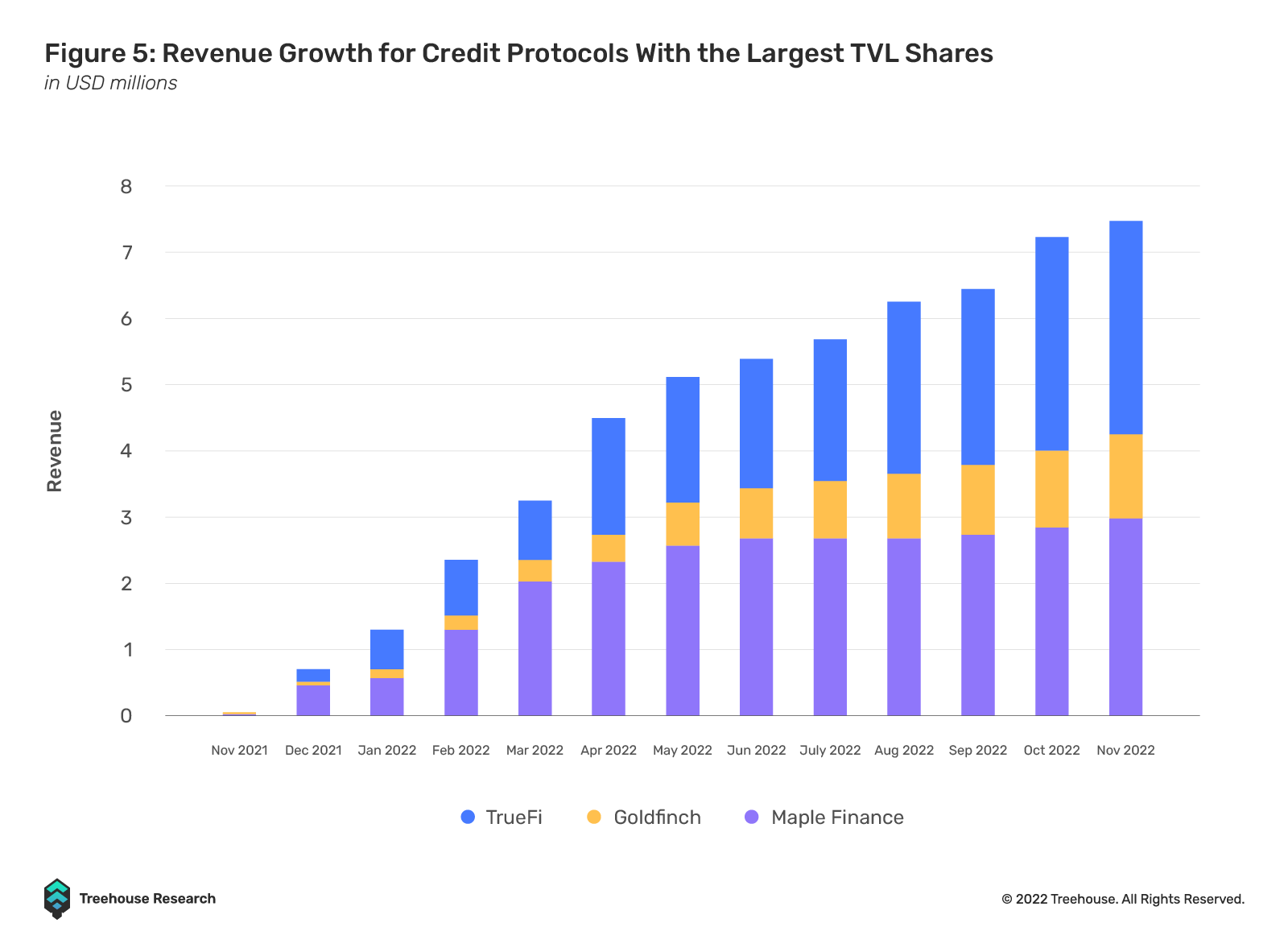

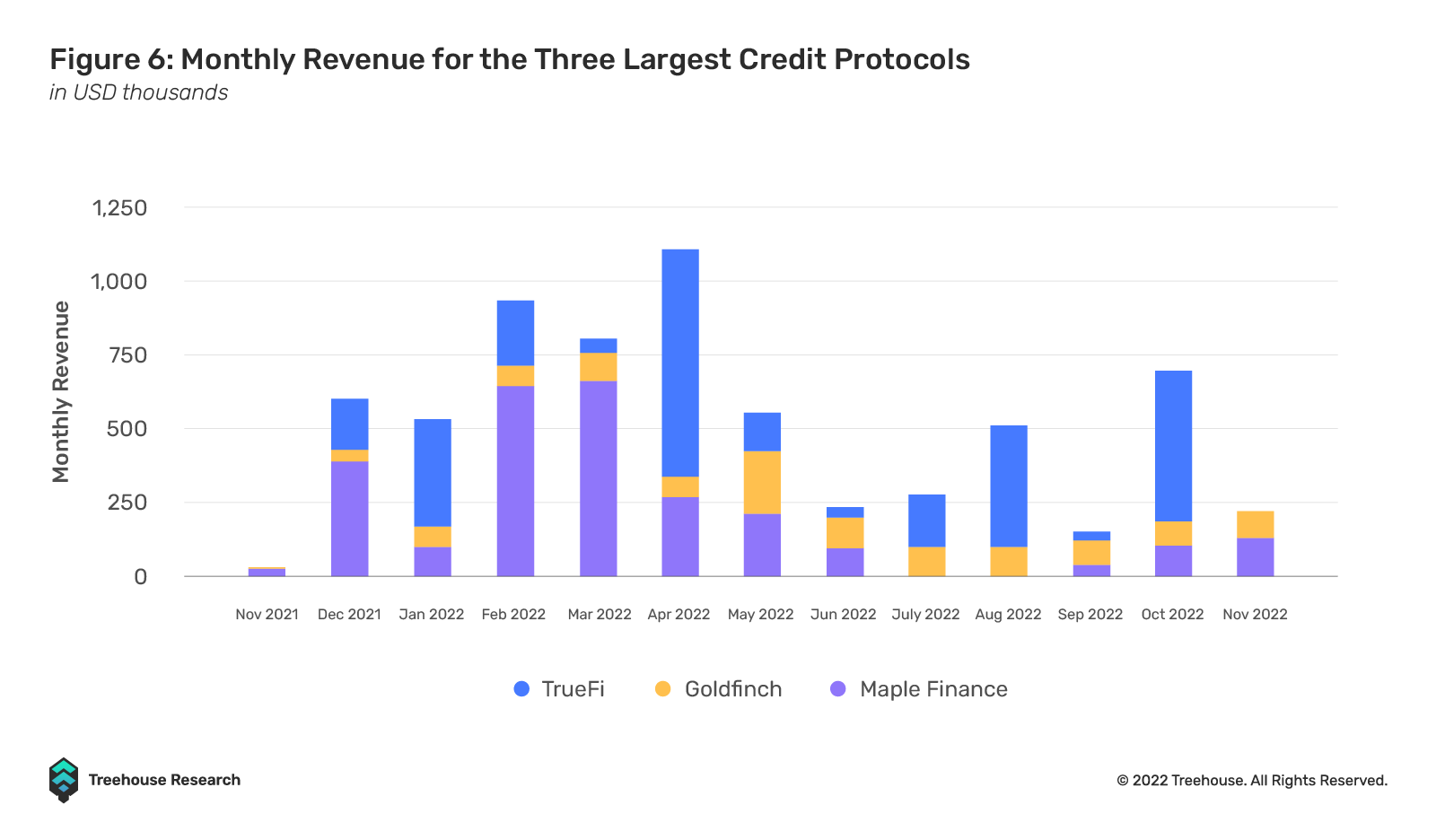

Credit protocols have managed to generate a total of US$10.9M in revenue over the past year. This revenue growth has been relatively stable, owing to the constant liquidity demanded by institutions that utilize these protocols.

The three largest credit protocols by monthly borrowing volume: Maple Finance, TrueFi, and Goldfinch, have generated relatively consistent monthly revenues over the past year despite broader crypto liquidity contractions.

The two main groups of institutions that these credit protocols provide funds to are crypto-native institutions and businesses in emerging markets. The crypto-native institutions that are currently actively taking loans on these protocols are mainly hedge funds and trading firms. These companies, although having similar, if not, superior performance to their TradFi peers and healthy balance sheets (although we did see surprises during the FTX drama), are unable to obtain loans through traditional institutions like banks.

Emerging markets are another set of borrowers that are funded by these credit protocols. Demand for exposure to private debt has continued to grow throughout 2022, with emerging debt markets riding on this trend as the startups and technological ecosystems in this sector continue to grow.

Emerging debt markets provide investors with favorable risk-to-reward investment profiles, which has created a demand for exposure to these types of debt instruments. However, investors might find it difficult to access debt markets in emerging economies. Hence, to address this problem, certain credit protocols have provided access and yield by connecting potential lenders and borrowers. Goldfinch, a protocol currently serving borrowers from emerging markets, has noted that in order to minimize the risks and uncertainties of providing credit to a sector that is still in its growth stage, they only provide loans to established credit funds and FinTech organizations with historically stable financial performance. In addition, ensuring that the borrowers are of a satisfactory standard has worked out well for both Goldfinch and Credix, as the total default rate has been 0% since their inception.

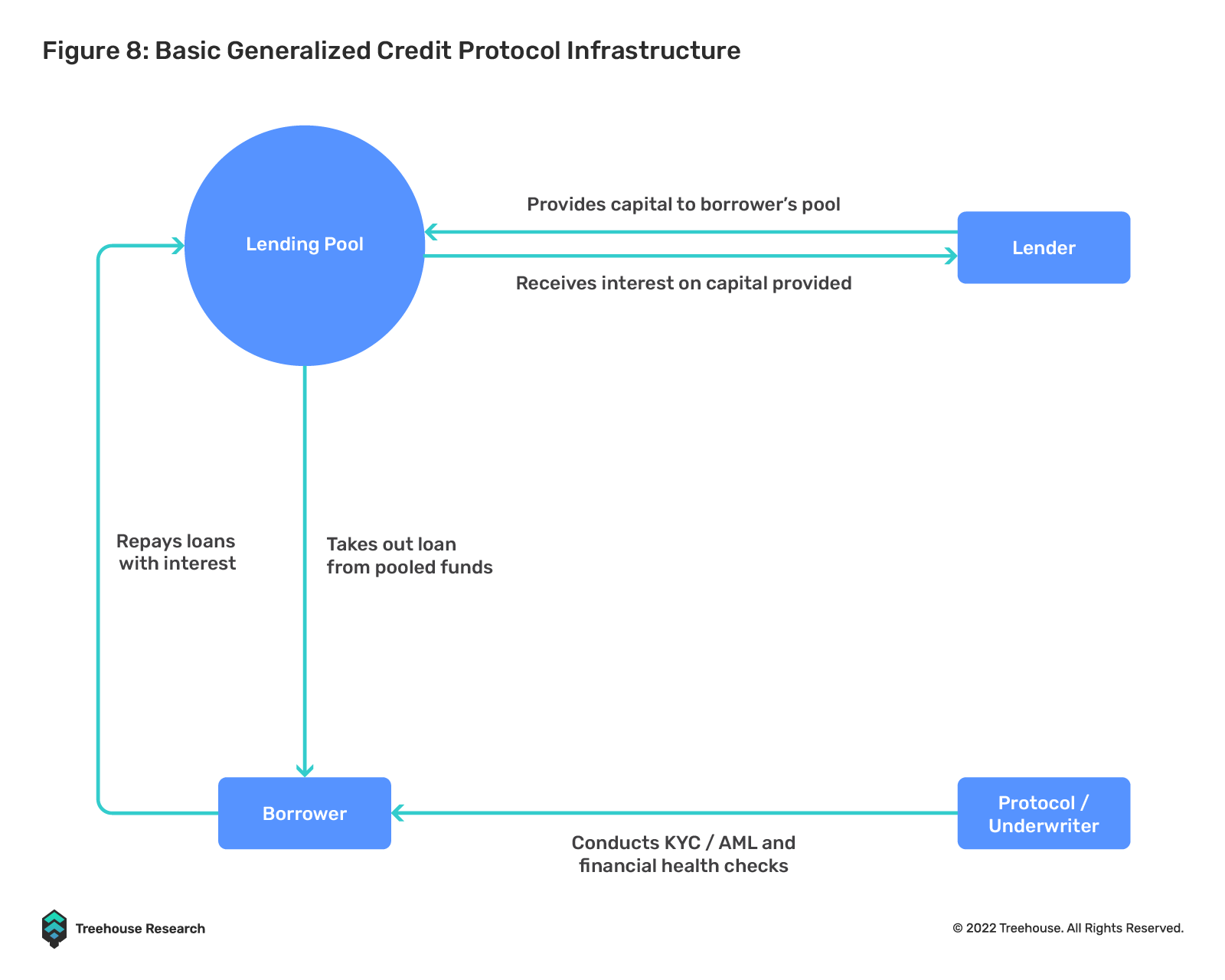

Credit Protocol Infrastructure

The current process of giving out credit for these protocols is relatively similar, with a few minor differences in protocol mechanisms and loan management.

Protocol Level

Credit protocols typically act as the infrastructure layer by providing the necessary risk assessment and credit scoring expertise required before loan origination, as well as making protocol-level decisions like interest rate mechanisms. Although such credit risk assessment decisions might make certain aspects of these protocols more centralized as compared to other DeFi money markets, they are essential in ensuring that the quality of borrowers on the platform meets certain criteria to minimize credit risk. Protocols either have teams with years of credit experience, or use a centralized credit rating vendor like Credora to assess the financial health of each potential borrower.

Protocols are also typically responsible for setting the interest rates for their lending pools, and these rates can be dynamic, or have a fixed default level. Examples of fixed interest rate protocols include Maple Finance and TrueFi, as the loan terms for their lending pools are typically decided off-chain between the borrowers and the party running the pool. Dynamic interest rates are typically implemented using algorithms that factor in pool utilization rates to determine the appropriate interest rate. This method is utilized in protocols like dAMM.

Borrowers

How to Borrow?

The processes for borrowers across most credit protocols are relatively standardized, where they have to clear KYC and anti-money laundering (AML) procedures set by the protocols, as well as undergo an analysis of their financial health before they can open a lending pool. After borrowers clear the necessary procedures, they can open a lending pool that usually functions similarly to a revolving credit line, where they are able to borrow up to a certain amount of capital supplied to the pool, and can take loans at any time as long as there is sufficient capital available. These processes apply to most protocols that allow institutions to set up their own pools and borrowend directly from them, such as dAMM and Clearpool.

However, for protocols that use the business model of allowing institutions to set up credit facilities, borrowers usually have to go through an additional third party in the setup process. This additional party plays the role of a pool manager, interacting directly with the borrowers, and negotiating credit terms with them. These pool managers typically have to go through KYC checks by the protocols as the pools are set up by them. Being a pool manager is akin to running a credit business, and the borrowers have to interact with them to get loans. Once these loans are approved by the managers, borrowers can start borrowing from these pools as well. Protocols that follow this structure include Maple Finance and TrueFi’s Capital Markets, where each pool is run by an institution that pools funds and approves every individual borrower on their own, managing different loans, thus, acting as a credit business.

Interest Payments

For most protocols, interest is automatically compounded every epoch, and borrowers have the flexibility to choose to pay back their loans whenever they deem fit. There are, however, some protocols like TrueFi where interest only has to be repaid at the end of the loan tenor, which allows borrowers to not have the obligation to make interest payments until the date of repayment arrives.

Lenders

How to Lend?

At the moment, the majority of credit protocols run permissionless pools, which means that lenders can choose to deposit funds into any pool of their choice. As long as a user has a compatible Web3 wallet and pool assets to be deposited, they can supply capital to lenders of their choice to start earning interest. For some protocols and permissioned pools, however, lenders need to go through KYC/AML processes before they are able to deposit funds into these pools. At the moment, the three protocols that require lenders to clear KYC before they are able to deposit funds are Goldfinch, Centrifuge, and Credix.

Vanilla Lending Pools

Most of the current protocols adopt a model where lenders simply need to pick an institution that they wish to lend their funds to, and deposit capital into the respective pool. This is similar to supplying funds on AAVE, just that the borrowers are institutions that have undergone the KYC process to be onboarded by a credit protocol.

Tranched Lending Pools

There are several protocols that split their lending pools into different tranches, offering lenders the ability to choose the amount of risk they are willing to take on to receive interest yield. Centrifuge is an example of a protocol that offers tranched loans in the form of different tokens that represent Junior or Senior tranches. Lenders that choose to lend funds to Junior tranches typically earn higher yields as they provide first-loss capital in the case of any defaults. On the other hand, lenders of Senior tranches earn lower yields, but they are shielded from defaults by the Junior tranches’ liquidity.

Interest Payments

For most protocols once a lender has deposited funds, he is unable to withdraw them until either the loan term has ended, or there are sufficient funds in the pool. This might mean that the funds provided are illiquid for the loan term. If the lender deposits in a pool that has its funds fully utilized at the moment, the lender would be unable to withdraw his funds until the next interest repayment, or until the loan is fully repaid.

DeFi as the Equalizer of Credit Access?

It might seem that DeFi credit protocols are merely on-chain iterations of traditional banks or lending institutions due to their centralized nature as compared to their overcollateralized counterparts. However, DeFi credit protocols offer advantages throughout the entire process and lifetime of a loan that is not replicable in TradFi.

Evolution of Credit Processes

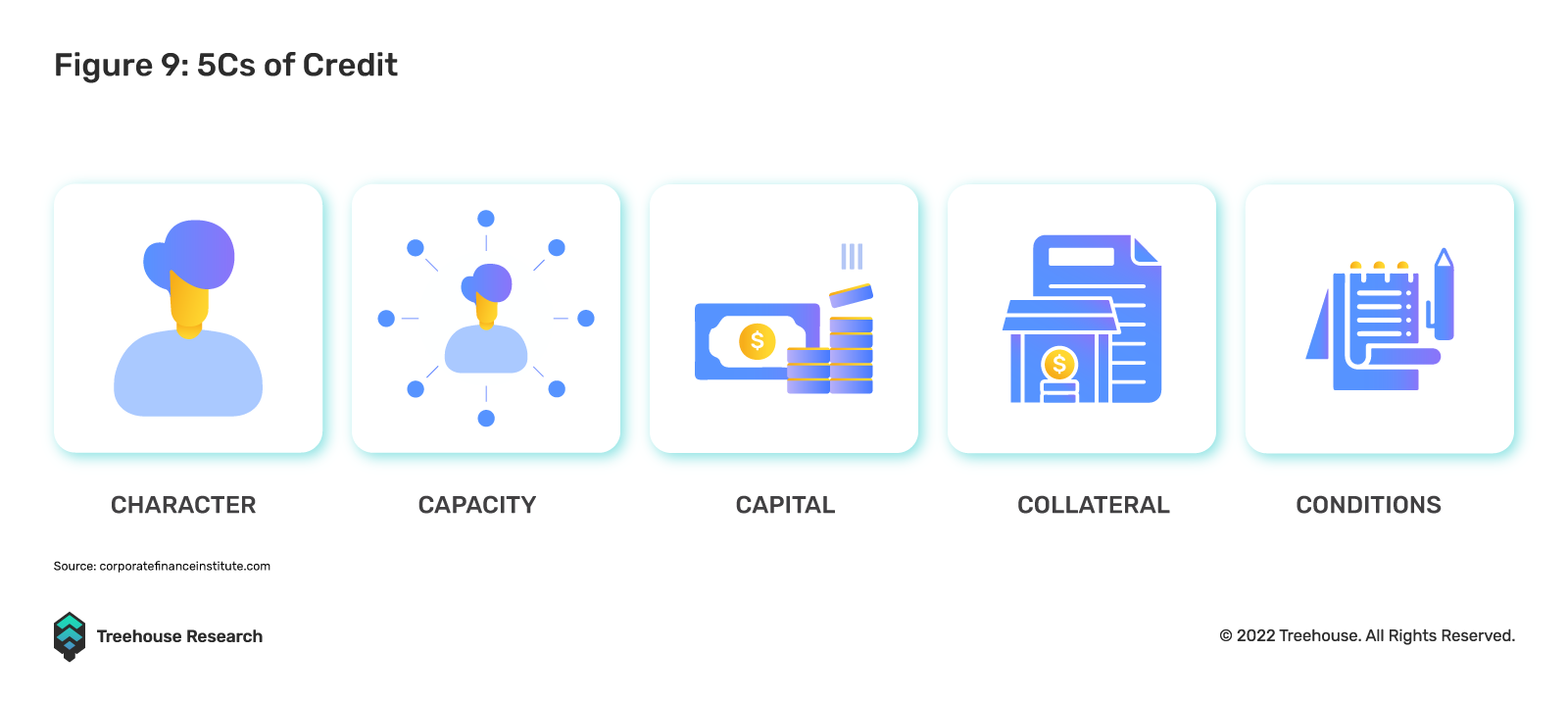

In TradFi, the amount of credit that one can receive depends on a framework commonly referred to as the “5Cs of credit”. This framework plays a heavy role in deciding how much credit might be extended to the party looking to receive it. This is also known as the creditworthiness of the party requesting credit.

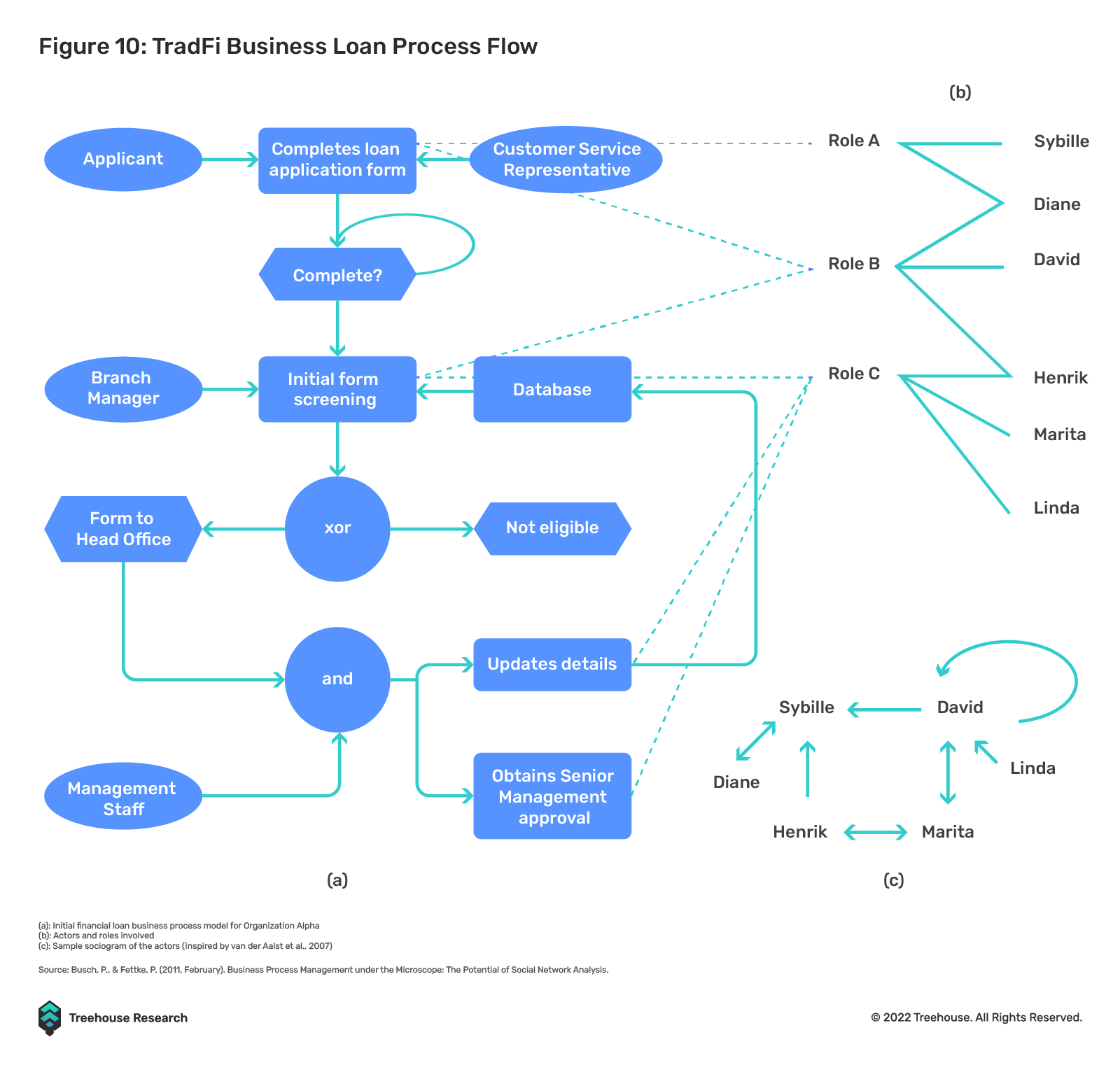

These 5Cs are typically assessed concurrently to get an accurate picture of the potential borrower’s current financial situation. For example, if an SME wishes to receive a loan from the bank to finance the purchase of machinery, they would be assessed by the 5Cs. However, the process of getting a loan is not as straightforward as just approving a transaction on your wallet in MetaMask like getting a loan on AAVE, instead, it requires the involvement of multiple parties and individuals to complete each step of the process.

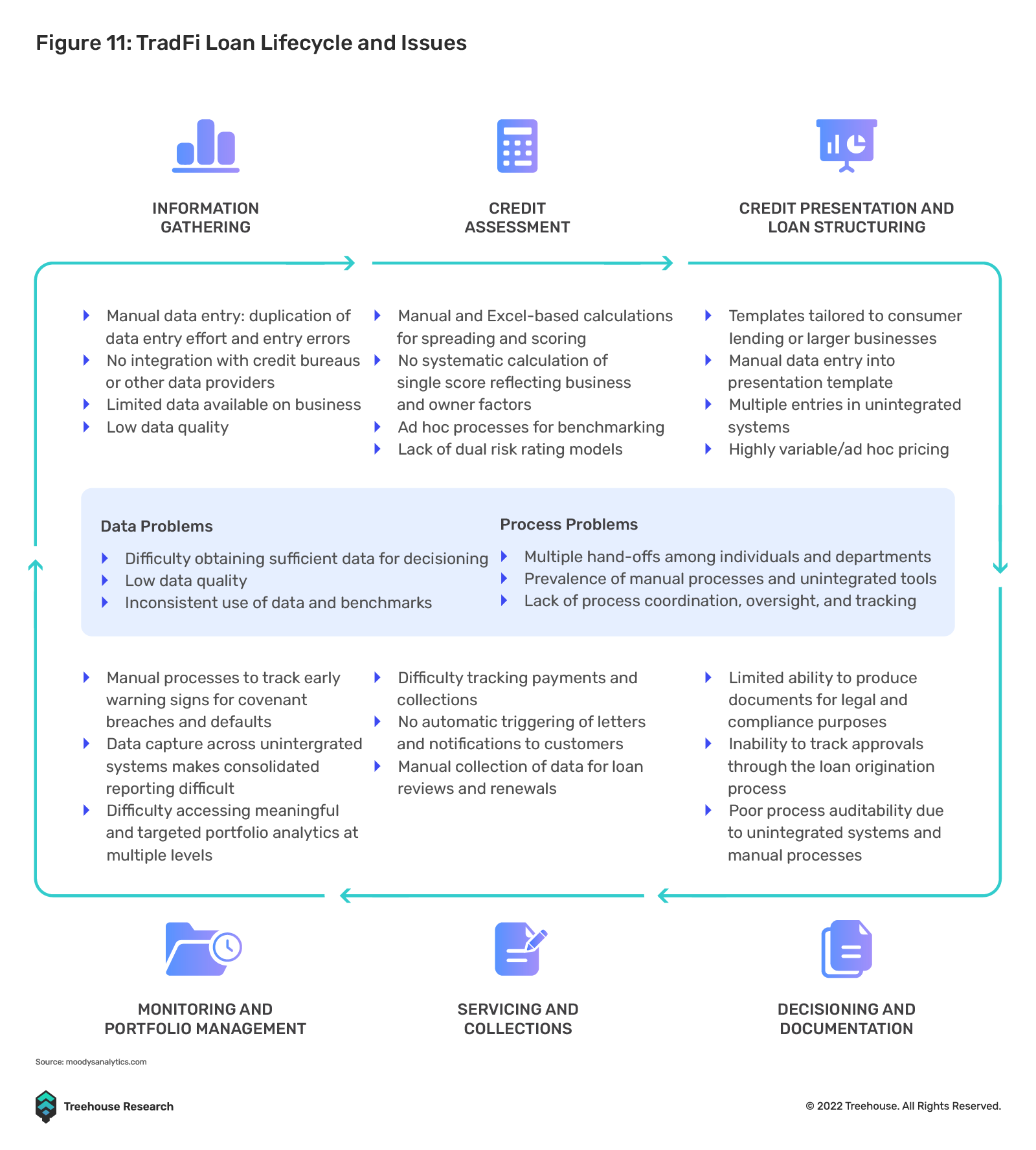

Obtaining a TradFi loan is, therefore, not only expensive, but also time consuming. Data suggests that only around 7% of TradFi loans are processed in a week on average, and the involvement of multiple parties can cause lending costs to balloon. Plus, applying for a new credit line at a financial institution with which the borrower has an existing relationship might still require going through the entire 5C vetting cycle again. The operational costs of all these processes will likely be borne by the borrower in the ultimate loan pricing, because TradFi lending (at least the legitimate ones) is highly monopolized by established financial institutions. Thus, the costs that tally up will likely be borne by the borrower in the aggregate loan pricing.

The inefficiencies of Tradfi’s archaic processes have been streamlined by current DeFi credit models, which provide borrowers with the operational flexibility to borrow and repay 24/7 once the initial borrower application is approved.

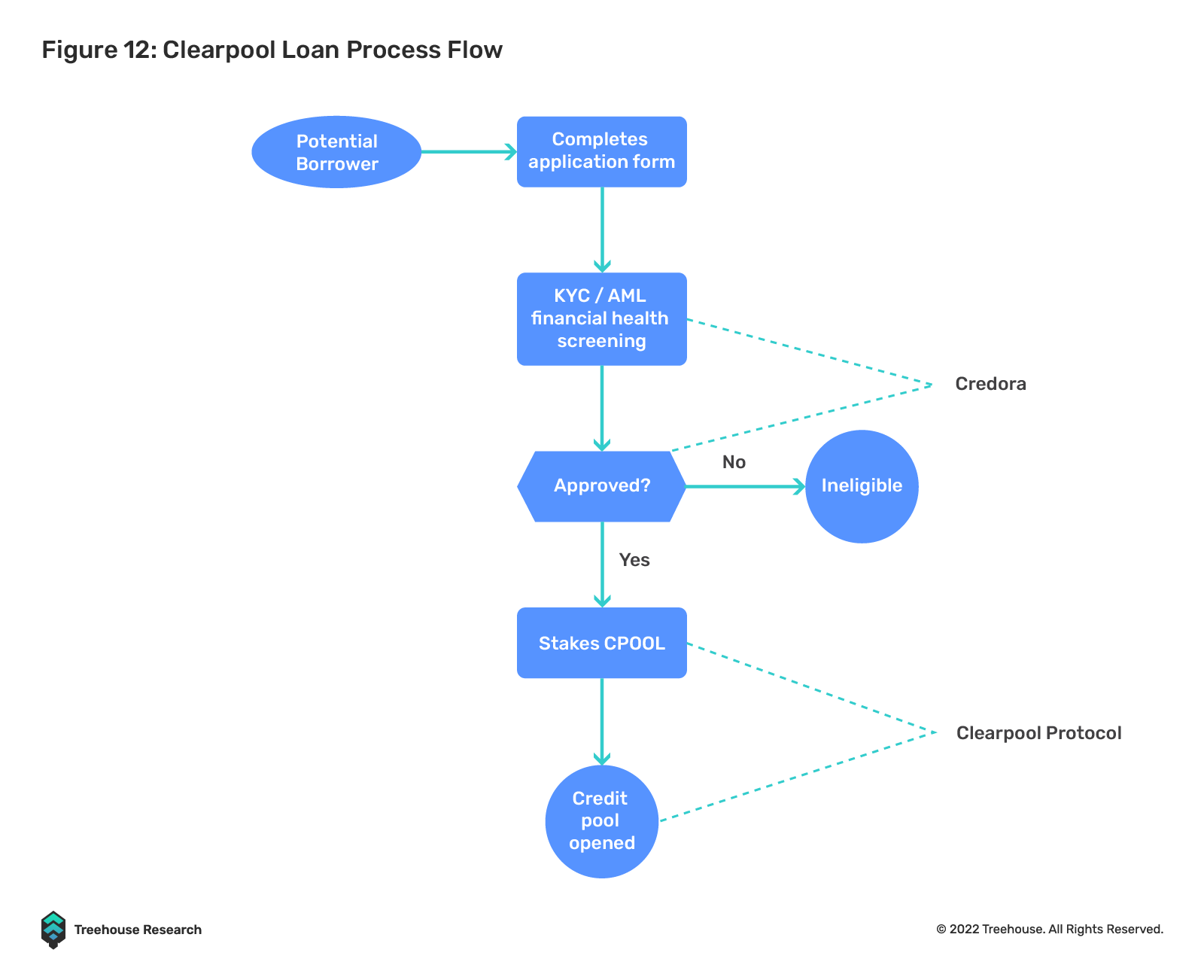

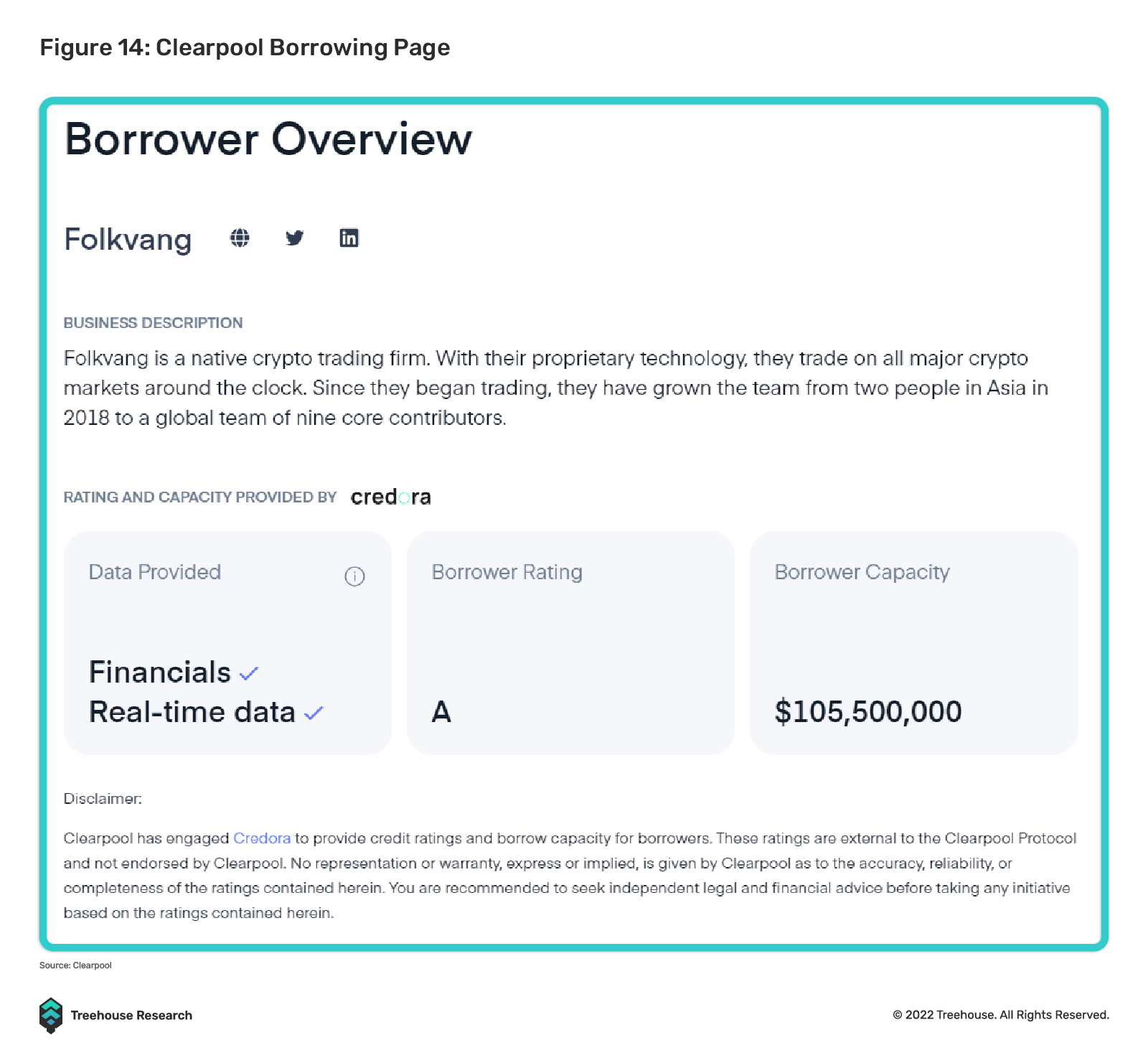

An example would be Clearpool’s loan origination process. For Clearpool, borrowers only go through two intermediaries – the protocol itself and Credora. Additionally, the number of steps and processes required to get a loan request approved and originated is drastically reduced as compared to TradFi institutions. Intermediaries are cut out and, as a result, borrowers can access competitive rates from DeFi undercollateralized lending protocols. The cumbersome technicalities involved in TradFi borrowing such as waiting for loan drawdown to be credited into the borrower’s account, or transferring borrowed liquidity to a destination account, can be efficiently replaced by blockchain technology.

Greater Credit Availability for Underserved Borrowers

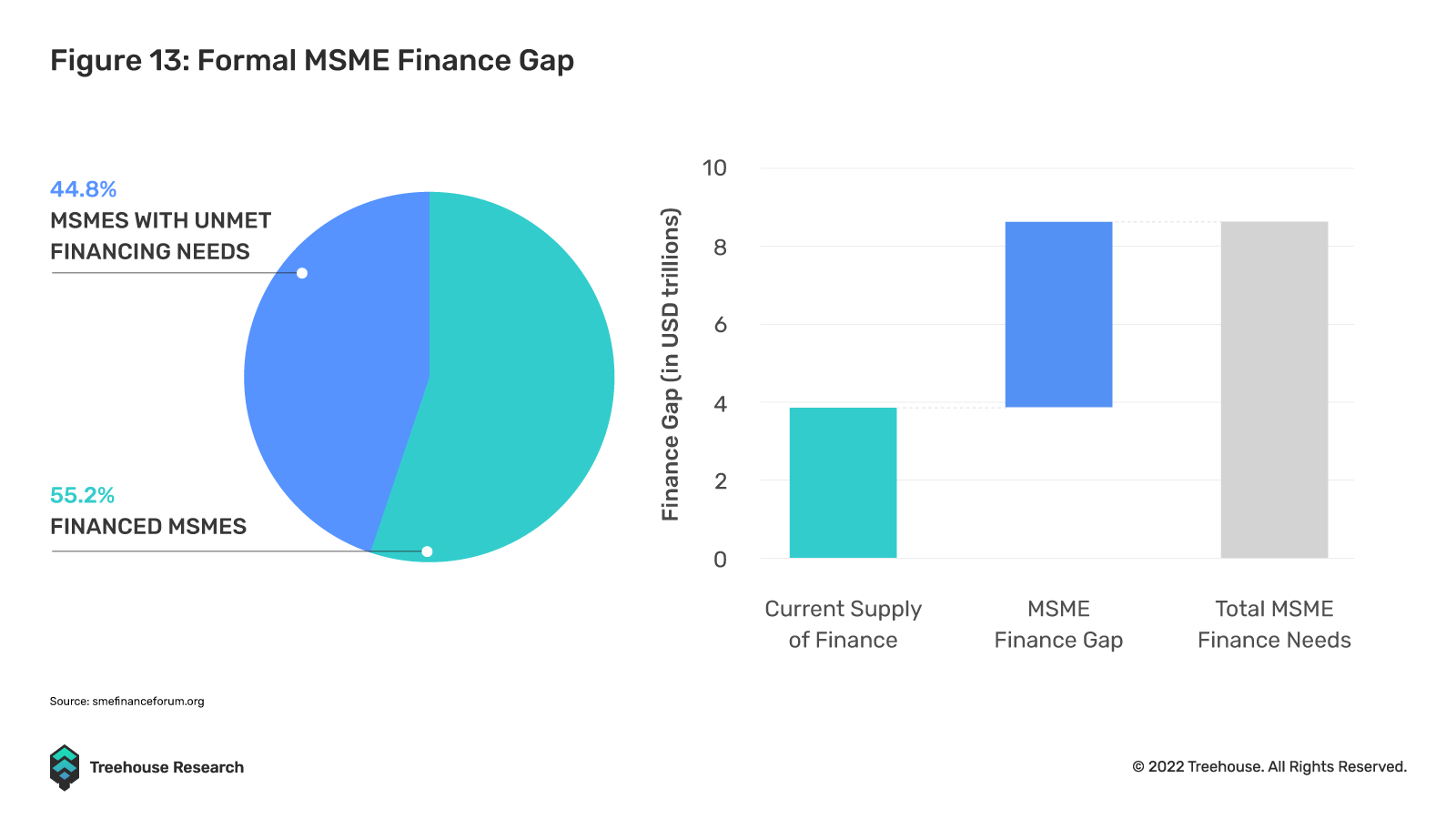

DeFi credit protocols, though not perfect, have brought easier access to borrowers previously deemed “underserved” and/or priced out by legitimate TradFi/CeFi lenders (loan sharks are, of course, outside of the context in this article). For example, aspiring crypto market makers might find it hard to leverage up by borrowing from CeFi lenders after the 3AC fiasco, and they certainly have little hope of expanding balance sheets via repo trades with TradFi investment banks. Similar roadblocks exist for many crypto financial institutions as well, and DeFi credit provides a cheap and non-dilutive alternative to introducing fresh venture capitalist (VC) capital. In non-financial sectors, DeFi credit also fills the gap for businesses in emerging markets (Latin America, Africa, and Emerging Asia).

Businesses in emerging markets face a notable gap in financing since many are underserved, lacking around US$5T in investment annually. Several credit protocols have sought to fill this gap, one of them being Goldfinch, specializing in bridging lender capital to borrowers in developing countries where access to TradFi credit is expensive and inconvenient. Although the 5C credit due diligence process is still carried out for borrowers on Goldfinch, the credit risk assessment is, at least, carried out through decentralized consensus (among stakers) rather than corporate monopoly.

Although DeFi credit protocols serve only a niche market today, there are a couple of pathways leading to larger-scale adoption. One fathomable trajectory is the mutual acknowledgment of credit scores/ratings between users and entities in DeFi and TradFi, which will allow borrowers with credit history on one side to access credit on the other. This would benefit not only institutional, but also, retail borrowers, and potentially bring on-chain credit “card” into reality. The mutual acknowledgement of credit scores, however, will likely require borrowers to reveal their real identities for KYC and compliance purposes. This could be a dealbreaker to decentralization maxis.

Transparency, Anti-fraud, and Risk Management

Growth in DeFi credit protocols provides hopeful cures to several plagues in TradFi and CeFi credit markets.

Above all, DeFi borrowings are on-chain and open to scrutiny, which levels the access to information between lenders. In comparison to TradFi, there have been cases where lenders with private credit exposure to a borrower learn of an upcoming default sooner than those with only public debt exposure. Private credit lenders would have an unfair edge in accessing information sooner and potentially reduce their exposure at the expense of public credit lenders. Despite insider trading laws, such cases would be hard to prove in a court of law and, thus, lenders without information edge would be stuck with the loss. If an institution conducts all lending through DeFi, the transparency would prevent the aforementioned information gap, and bring fair and true pari-passu status to all lenders. Several DeFi credit protocols provide borrowers with real-time on-chain credit scores as well as historical borrowing activity, offering a greater level of loan transparency as compared to their CeFi counterparts.

Protocols like Clearpool provide real-time credit scores via the use of Credora, where information on borrowers and their respective loan pools is readily available. They also provide users with information on the size of loans as well as the repayment history, along with the transaction hash should lenders wish to track the flow of funds for each borrower. Although credit terms such as collateral size are not visible to users, there is still a greater level of information access as compared to lending to CeFi institutions.

Admittedly, at this stage, many whitelisted DeFi borrowers are not exclusively borrowing on-chain, leaving a potential information edge to CeFi lenders. However, as we have observed during the CeFi credit crisis of May to July 2022, publicly scrutinized on-chain borrowings were usually repaid first (partially to release asset collaterals, but also due to pressure from oversight).

The consensus mechanism in DeFi credit due diligence also helps to reduce fraud. Traditional loan approval processes at financial institutions usually rely on a few decision-makers, which poses concentration and key man risks when it comes to fraud prevention. Netflix fans might recall the heroine, Anna Delvey or Anna Sorokin, in the true-story-turned-drama Inventing Anna, who faked her identity and managed to trick banks into extending credit lines on false impressions and forged papers. It is hard to imagine her pulling off such a feat in the context of DeFi borrowing, where KYC is conducted by a cohort of protocol stakeholders such as token stakers.

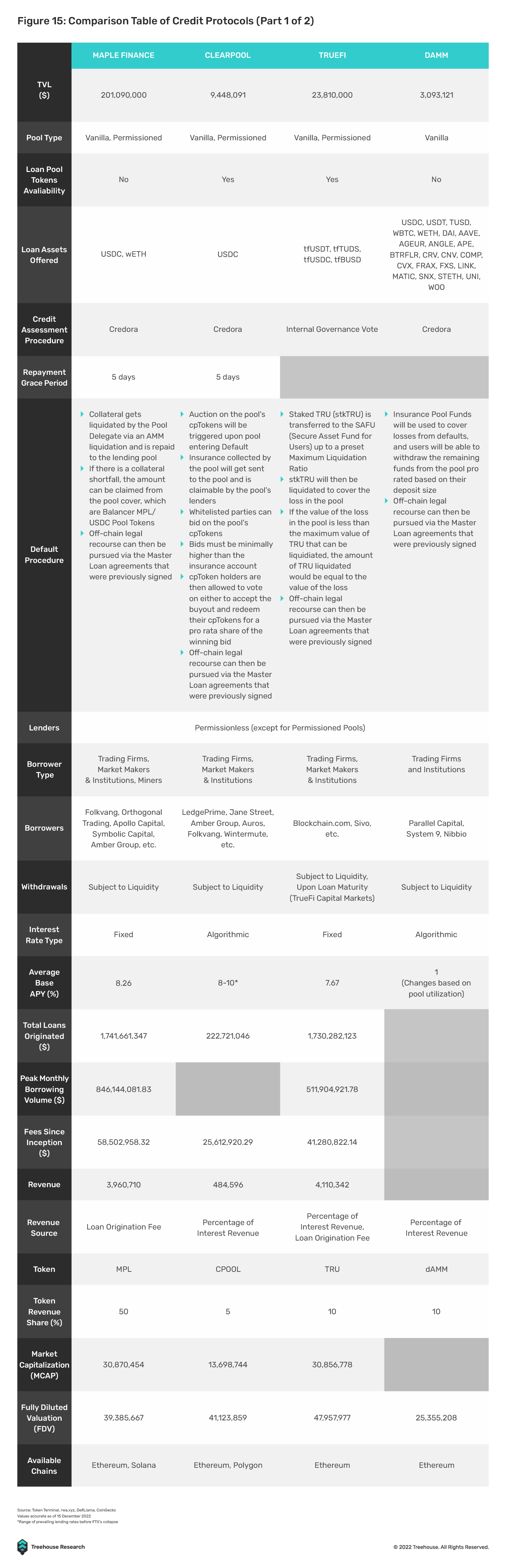

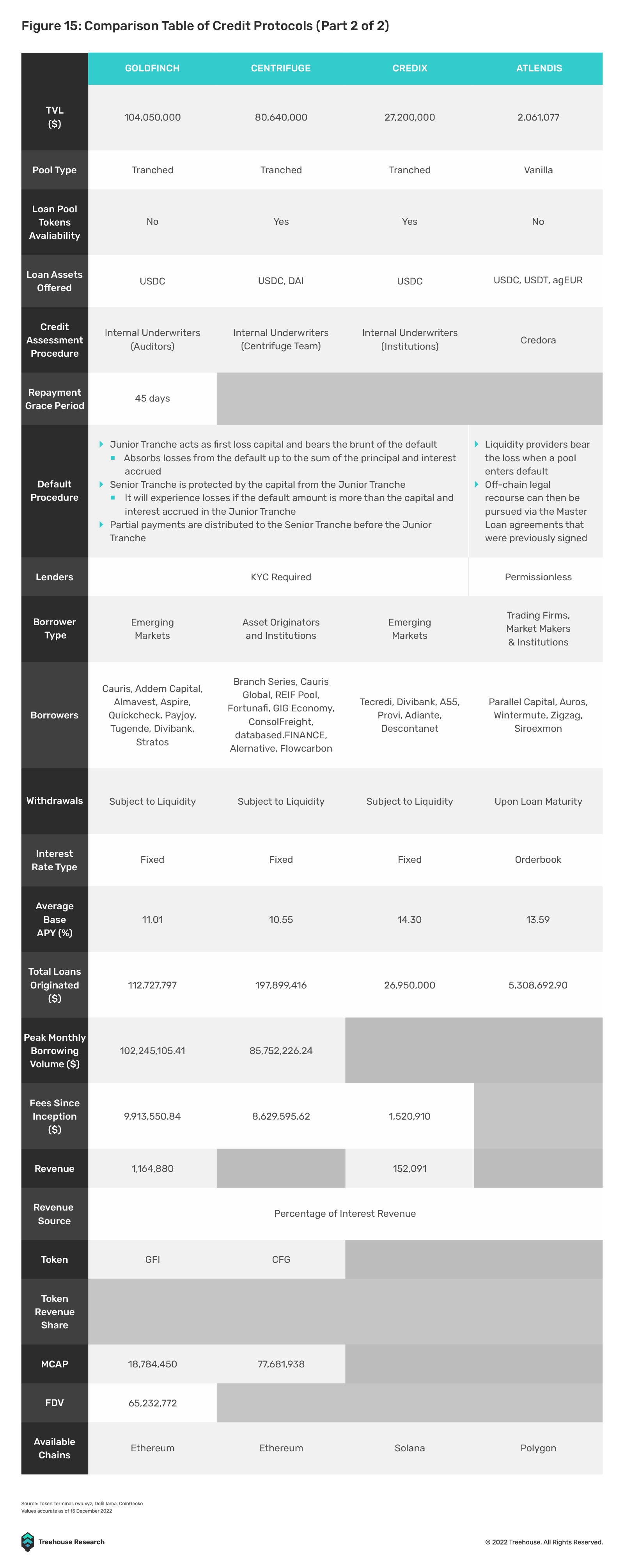

Existing Credit Protocols

In the table below, we compare current and notable credit protocols in DeFi using a variety of qualitative and quantitative metrics.

Current Limitations of DeFi Credit Protocols

Despite their achievements, prevailing DeFi credit protocols face several limitations that hamper further adoption to different extents.

Lack of Term Structure

This shortcoming is, by no means, limited to DeFi credit protocols. Most of DeFi money markets operate in a zero-duration fashion, as investors are still largely clinging to liquid investments due to smart contract risks. Depending on the protocols, DeFi credit pools are either structured as revolving credit facilities, where borrowers draw down and repay on a flexible schedule, or as short-term fixed-maturity credit lines with durations of less than six months. The only exception is Goldfinch, which allows businesses to secure three-year borrowing arrangements.

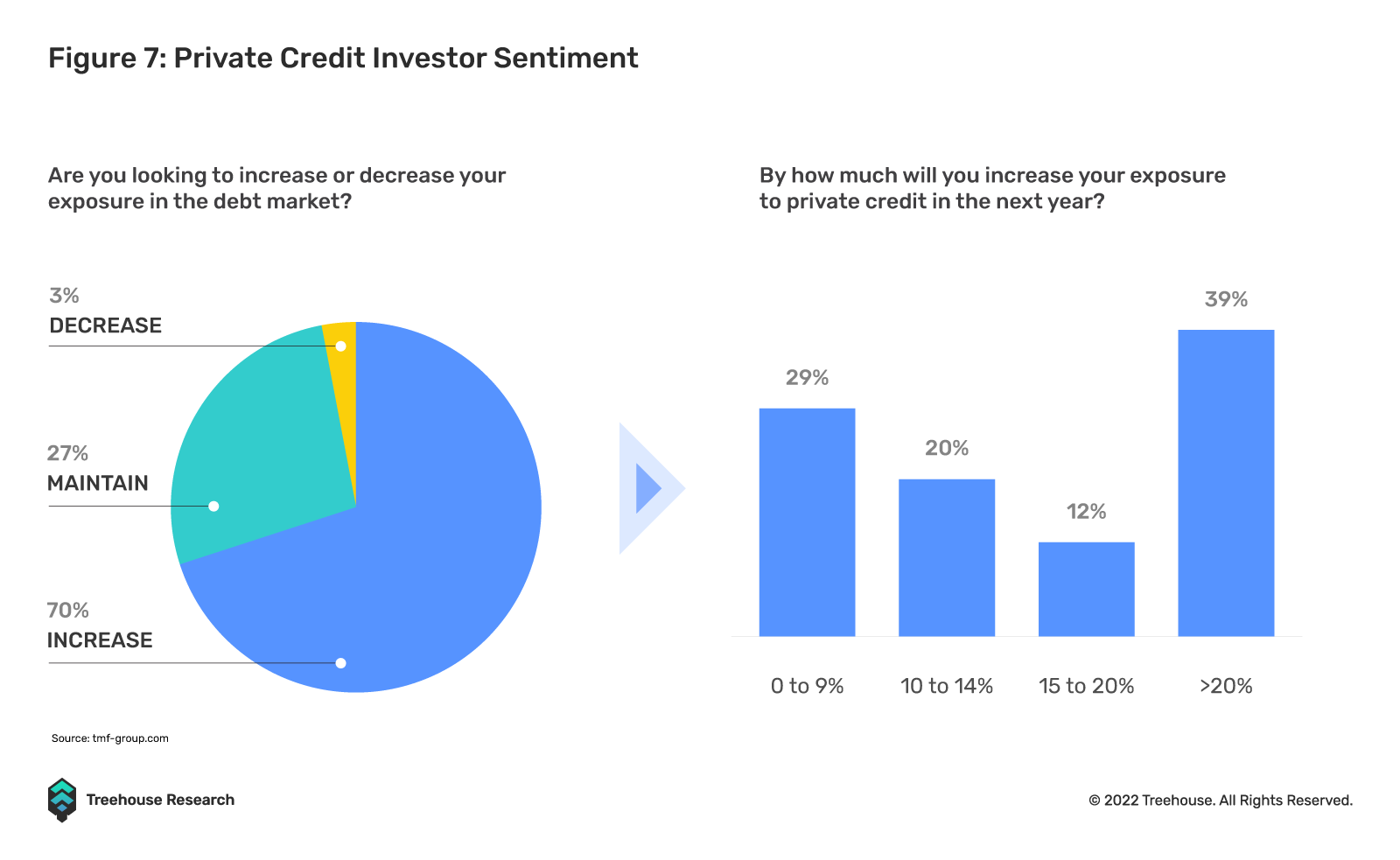

Right now, since most DeFi credit borrowers are financial institutions such as trading firms, lack of duration is of less concern because these borrowers are usually content with short-term financing. This way, they enjoy the flexibility of shrinking balance sheets when market opportunity sets do not justify large borrowing. For credit investors, however, some are becoming more comfortable with taking smart contract risks and looking for longer-term, fixed-rate yield. Demands from these investors will likely be better served with differentiated, longer-duration offerings.

Concentrated Sector Risk

As mentioned above, most DeFi credit borrowers operate in the same segment, which exposes lenders to heightened correlation among their lending portfolio, also known as higher joint default probability. Goldfinch’s model of introducing non-financial borrowers helps to bridge this gap through diversified on-chain lending.

Lack of Consensus Credit Rating Framework

With the emergence of on-chain credit rating providers such as Credora, the current lack of a standardized DeFi credit rating framework could be solved soon. Investors currently have no easy means to assess the creditworthiness of borrowers: they either have to establish bilateral relationships and collect financial statements, or rely on rating providers.

Legal and Compliance Implications

There are many unclear legal implications when it comes to DeFi credit. First and foremost, DeFi credit origination does not necessarily provide prospectus like TradFi credit bond offerings. The absence of prospectus and legal documentation can lead to issues including, but not limited to, illegal solicitation and ambiguous debt seniority. How do lenders determine whether their lendings are pari-passu to other off-chain unsecured liabilities of the borrower? In times of default, do off-chain creditors have the right to accelerate DeFi obligations even if the DeFi credit pools are being paid on time? Does on-chain proof of lending to a borrower have legally binding power in a court of law? All of these subtle procedural necessities have to be addressed before DeFi credit markets can achieve greater adoption.

Capital Illiquidity

Although most current DeFi credit pools do not come with explicit capital lock-up periods, lenders can, by no means, treat their invested principal as liquid. Withdrawable amounts are determined by the utilization ratio, which means that if most of the available pool capital is borrowed, lenders need to wait for either repayment or new inflow to take their money out.

Although some protocols offer a “liquid exit” by allowing lenders to sell their tokenized loan tokens on the open market, in the event of a massive lender exodus from the pool, lenders would still be left stranded for obvious reasons. This issue is likely better solved by differentiating term loans against revolving credit facilities, so that lenders know for sure how long their capital is locked up for, and can proceed to plan accordingly.

Another way of increasing liquidity for DeFi credit borrowings is the introduction of market makers to tokenized loans – similar to how TradFi market makers provide secondary liquidity using principal balance sheets. The obvious obstacle to this route is the lack of credit instruments (credit default swaps, shorting tokenized loans, etc.), which reduces market makers’ capability to hedge risks and, thus, reduces the depth of market.

Future Developments

In this section, we outline several directions that we foresee the DeFi credit space will eventually move towards to one day, making general-purpose DeFi credit a reality.

Credit for Retail

In TradFi, credit is heavily utilized by retail for funding big ticket item purchases like cars or mortgages, as well as more ubiquitous use cases like paying for college education. The availability of retail credit in DeFi would be a major value proposition.

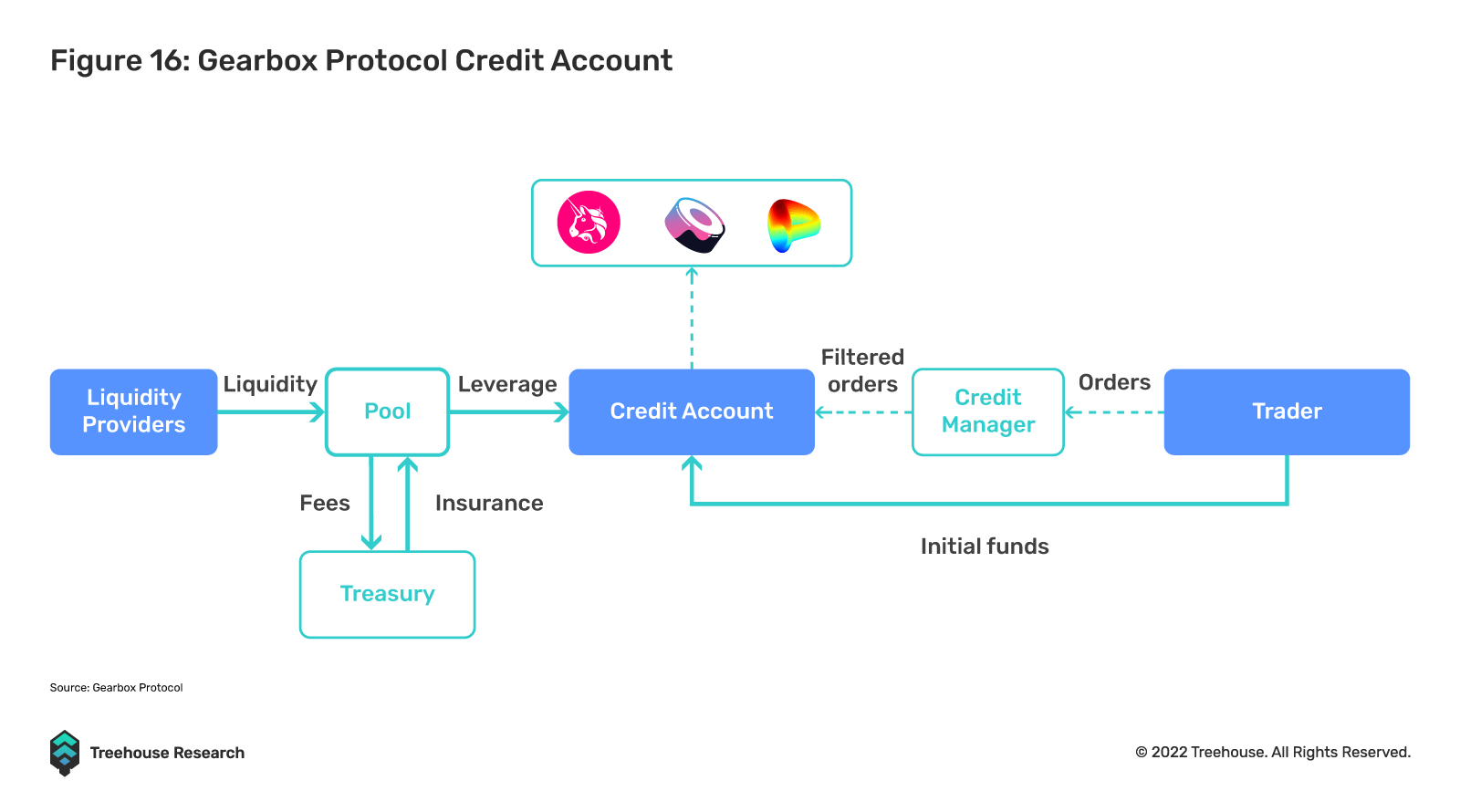

An example of an attempt to address the retail DeFi credit market is Gearbox Protocol. It provides retail credit via the use of credit accounts, which are isolated smart contracts with set parameters that only allow access to whitelisted tokens and protocols for the implementation of yield or trading strategies using credit loans. This model allows for credit creation without the need for KYC as the borrowed funds are not held directly by users, which eliminates the risk of them defaulting and running away with the borrowed funds.

Right now, retail DeFi credit is still limited to financial use cases, while consumer use cases remain very limited due to difficulties in ascertaining on-chain identification. We believe that a possible solution to this problem of “incentive to default” is by making use of soulbound tokens (SBTs). These non-fungible and non-transferable tokens would ensure that should a user default, he would be unable to take future loans as his credit history would be tied to his on-chain identity. As the technological stack continues evolving, we foresee that SBTs will play a central role in ensuring compliance for retail consumer credit to be a reality.

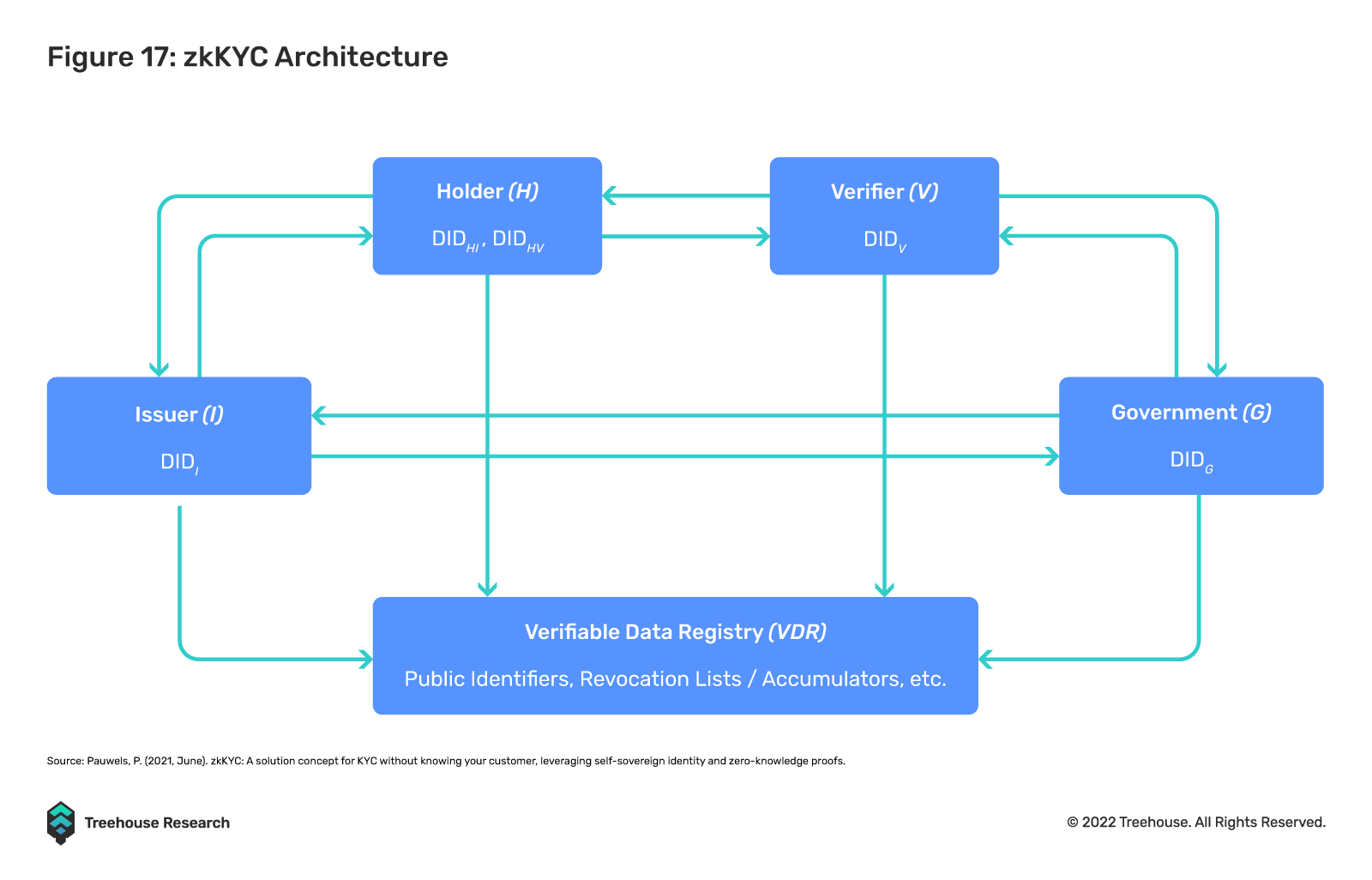

Zero-Knowledge KYC (zkKYC)

Current credit protocols require all borrowers and certain lenders to undergo KYC/AML procedures, which are still currently centralized and without industry-wide standards.

zkKYC would allow users to prove their identity without needing to fully reveal all personal data, while still adhering to all required KYC obligations. This could also help to provide a standardized KYC procedure across different credit protocols, possibly increasing the composability of decentralized identification across different protocols and preserving user privacy at the same time.

Final Thoughts

Despite many hurdles ahead, the DeFi credit market has demonstrated its growth momentum and ability to nurture innovation. As one of the most traded risk premia in TradFi, credit risk could become the next heavyweight in the “real yield” narrative.

The most interesting observation of DeFi credit is perhaps that the growth of this market is directly against the decentralization in “DeFi”. Both lenders and borrowers voluntarily undergo KYC and whitelisting in order to participate in these protocols, putting anonymity at a lower priority. Such permissioned on-chain marketplaces are likely a lasting trend that will lead to increased institutionalization of on-chain financing and investing activities, as regulators reach deeper into transactions and returns that were previously out of reach for them. The long-term impact of such developments is hard to gauge, as DeFi’s original concern of erosion of privacy and distributed governance might be resolved by future innovations that allow permissionless and algorithmic credit assessment.

All things aside, we, at Treehouse, are optimistic and excited to be part of the DeFi credit market growth as our engineers work hard to integrate credit risk management tools. In our opinion, the next star projects in the DeFi credit space will likely involve tools and marketplaces that trade credits more capital-efficiently, and on more diversified borrower entities, or in indexed packages with various term structures.

Disclaimer

This publication is provided for informational and entertainment purposes only. Nothing contained in this publication constitutes financial advice, trading advice, or any other advice, nor does it constitute an offer to buy or sell securities or any other assets or participate in any particular trading strategy. This publication does not take into account your personal investment objectives, financial situation, or needs. Treehouse does not warrant that the information provided in this publication is up-to-date or accurate.

Hyperion by Treehouse reimagines workflows for digital asset traders and investors looking for actionable market and portfolio data. Contact us if you are interested! Otherwise, check out Treehouse Academy, Insights, and Treehouse Daily for in-depth research.