Introduction

Ethereum’s nature sets it on a path to grow increasingly complex and it does not escape the drawbacks it brings. This sprouts from the core developments of smart contracts, a radical tool that allowed developers to build in the realm of DeFi, which has witnessed exponential growth and volatility over the last few years. However, novel systems bring novel risks.

MEV has existed since Ethereum’s inception but publicly surfaced in early 2021, especially when gas prices skyrocketed and the economy for MEV is worth hundreds of millions of dollars today. Currently, MEV is arguably one of the most severe issues Ethereum faces today.

In this article, we will be diving into what exactly MEV is and its implications, solidifying the knowledge of how a blockchain truly operates. Additionally, we bring forth the implications it has to the digital asset space (including users, searchers, builders and validators) as well as the existing and future developments. Lastly, we touch upon the debate between the two schools of thoughts on MEV: one suggests that it is harmful and has to be rooted out, while the other suggests that it is inevitable and has to be democratized.

What Is MEV?

Maximal Extractable Value (MEV) refers to the maximum value that can be extracted from block production in excess of the standard block reward and gas fees accrued. This is typically done by including, excluding, or reordering transactions in a block before mining or validating the actual transaction hash. Drawing an analogy to TradFi: MEV is to DeFi like how High-Frequency Trading (HFT) is to traditional finance.

“MEV” in TradFi

Skip this section if you want to get into the thick of Blockchain MEV

Flash Boys, a book about HFT written by Michael Lewis, documents trading firms that created methods to front-run orders placed by investors. Such behaviors existed since the 1930s when the telegraph was used to communicate positions across exchanges but it did not gain traction until 1983 when the Nasdaq introduced electronic trading.

Today, arbitrage opportunities are present all the time in traditional finance. These opportunities arise in milliseconds and are usually imperceptible to humans, but can be picked up by computer algorithms. A company called Spread Networks spent US$300M constructing a fiber optic cable 827 miles long from Chicago to the Nasdaq data center in New Jersey. The cable allowed HFT firms an extra 4 milliseconds to see investors’ orders, buy a stock before they could be executed and sell the stock to the original buyers for a slightly higher price.

Institutional and retail clients alike were constantly front-run by HFT firms as the exchanges provided fee rebates to HFT “market makers (MMs)” in pursuit of higher volume. According to the Financial Times, HFT accounted for 65% of the US Stock market volume in 2008. The debates on whether HFT MMs do more harm than good persisted – the proponents argue that HFTs increase liquidity and cite the increased volume and speed of execution as evidence, while the opponents argue that HFTs introduced friction by making execution more expensive and ultimately, the pension funds and everyday investors pay the extra price.

Other common methods HFT MMs deployed to extract value in TradFi include:

- Colocation → firms move nearer to the source of order book and flow data to cut the queue in information acquisition

- Dark pools → private exchanges, mostly run by investment banks, for trading securities that allow institutions to make privately negotiated trades, called “block trades” to avoid price impacts on open markets

- Payment for Order Flow (PFOP) → a form of compensation that a brokerage firm receives for directing orders for trade execution to a particular market maker or exchange

All of these TradFi examples of arbitrage come from two things: access to information and the speed to act on it. “Buy low, sell high” is not a new concept. Blockchain MEV originates from the same roots but with a different route of growth.

Blockchain MEV

Blockchain MEV was previously known as “miner extractable value” in the context of proof-of-work (PoW). In PoW, miners have control and are able to finalize transactions of a block in arbitrary order. However, since the transition to proof-of-stake (PoS) after The Merge, validators have now undertaken the responsibility for authenticating transactions. The value extraction techniques still exist but the phrase was renamed to “maximum extractable value” to reflect the change in consensus mechanism.

Brief History

MEV opportunities in Ethereum were first identified in 2014 – a year before Ethereum launched – by a coding analyst and experienced algorithmic trader under the pseudonym ‘Pmcgoohan’. His warning fell on deaf ears. In 2019, a group of researchers highlighted the same issue in a paper called Flash Boys 2.0, where the term “MEV” was coined.

Subsequently, Georgios Konstantopoulos’ and Dan Robinson’s Ethereum is a Dark Forest and Samczsun’s Escaping the Dark Forest in 2020 revealed MEV as an integral concept in crypto-economics. These articles not only bring light to MEV theoretically but also reveal that it was a real phenomenon already occurring at a significant scale with concerning consequences for Ethereum users in the form of exorbitant gas prices.

Why Does MEV Exist?

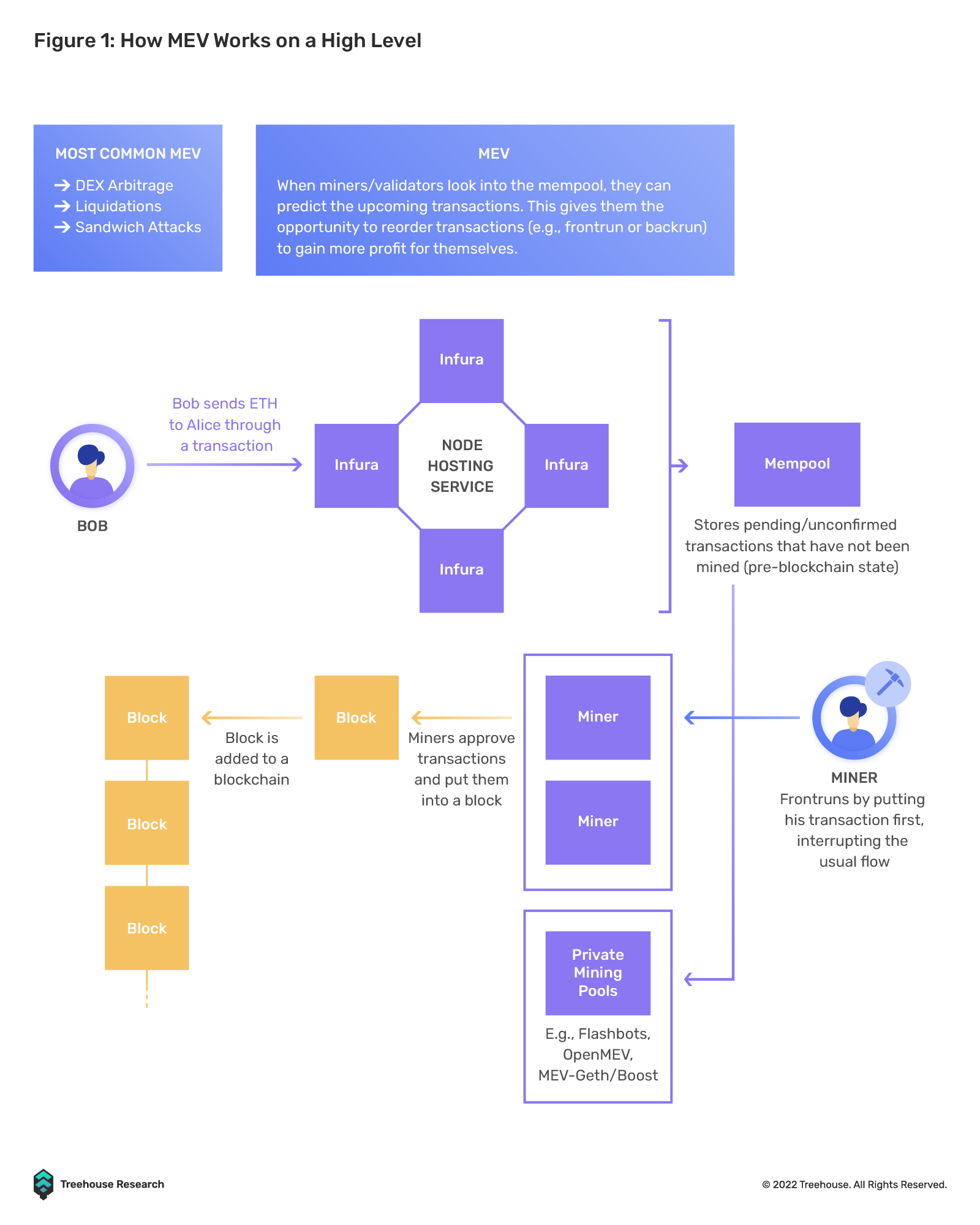

In every blockchain, there exists either miners (PoW) or validators (PoS), who are in charge of placing pending transactions into blocks before authenticating and adding them to the blockchain, according to the consensus mechanisms on the relevant ecosystems. These stakeholders of blockchain ecosystems are referred to as block producers and their power of sequencing the pending transactions, which will be explained more in detail, led to the existence of MEV.

The diagram below illustrates a high-level view of how the blockchain flow works and where MEV (in purple) usually fits in the blockchain:

Block producers can leverage their discretionary power to reorder transactions or even insert their own transactions to extract profits from the users. Ordering transactions by timestamp is not possible on blockchain networks as there is no unified concept of time in a decentralized network. The consensus algorithm of the blockchain instills the concept of time, thereby bringing order into the chaos.

MEV – A Simple Analogy

A special sale in a supermarket can be used to explain how MEV happens. Imagine, the owner-cashier could prioritize the order of customers willing to pay the highest tip and select his desired goods first – a bidding process would soon start as the deal hunters compete against each other

Note that in this example, since the cashier is also the owner of the business, there is no management who can penalize the cashier for his behavior . Moreover, the cashier will not be punished for discriminating against those who were outbid, as he did not force shoppers to shop at his business. The highest bidder earns the MEV from that transaction (either by flipping the goods to those priced out in tipping war, or getting his long desired PS5) and the cashier benefits by receiving the highest tip.

MEV Supply Chain

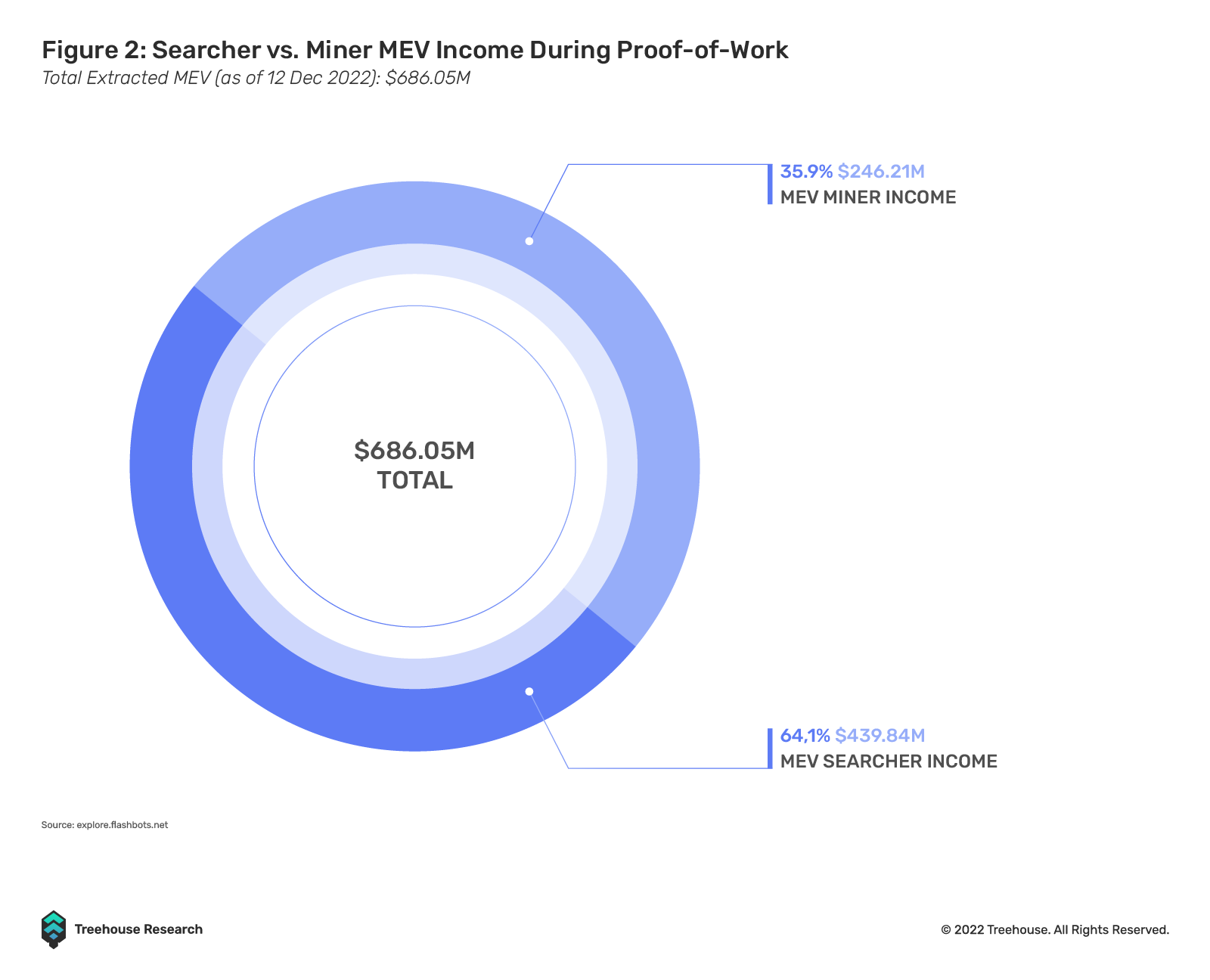

Back in the PoW days, there were two main stakeholders who existed in the business of MEV: miners and searchers. Miners make up the majority (>60%) of extracted MEV profits.

MEV Searchers constantly attempt to locate all extractable value on-chain – they are the customers who try to win the bidding war in our previous supermarket sale example. Searchers work with miners (the supermarket owner-cashier) since they surrender more than 90% of their total MEV revenue in gas fees to miners.

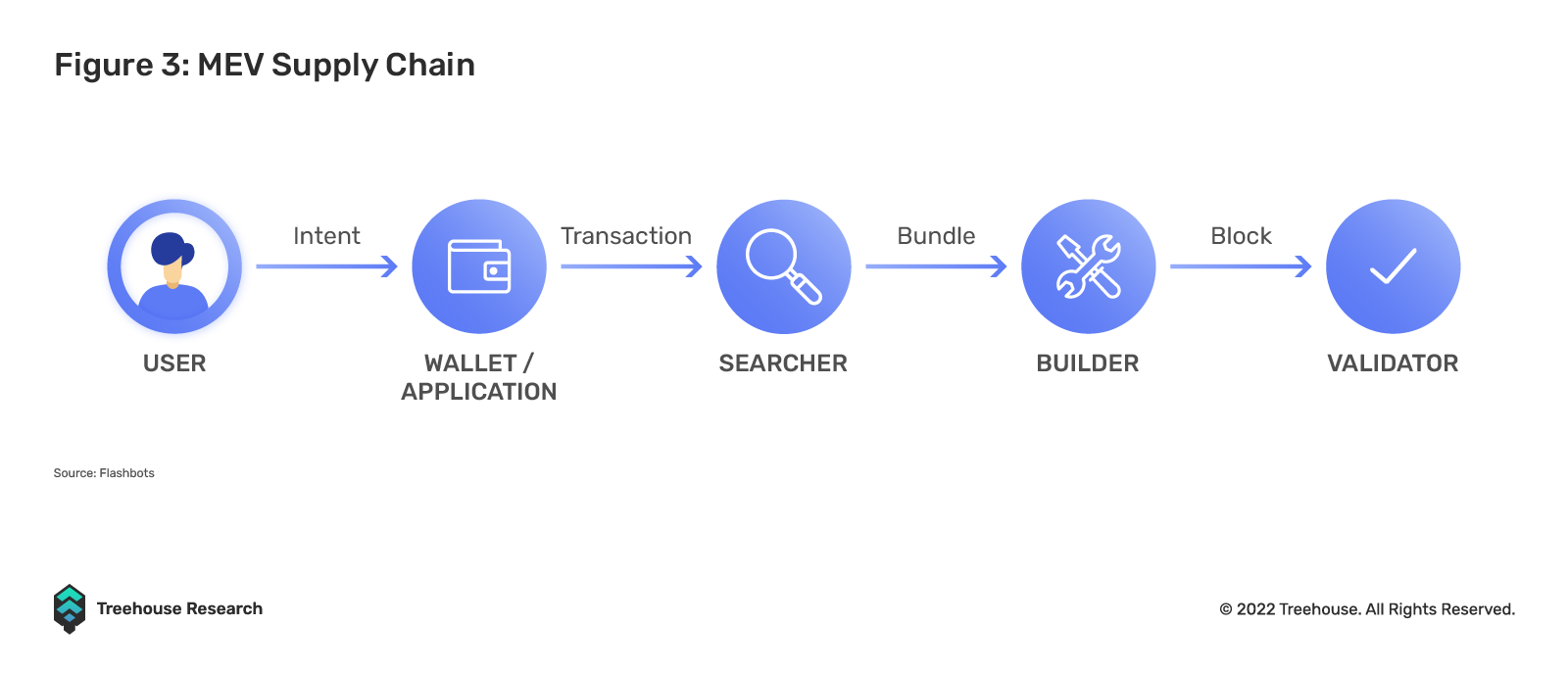

If we were to look at the two roles in the context of MEV supply chain:

Users: Individuals who interact with blockchains

Wallet: Applications that translate users’ instructions to blockchain commands and transactions. Protocol developers at this layer can build different MEV-relevant mechanisms for users. For instance, developers could decide to route transactions to the public mempool, or to a private routing system like Flashbots Protect RPC, which shields user’s transactions from searchers.

Searchers: Users that scan other users’ transactions and convert them into a transaction type called a bundle, which are one or more transactions grouped together and executed in the submitted sequence. In addition to the “searched” transactions, a bundle can also potentially contain other users’ pending transactions in the mempool.

Builders: Builders aggregate bundles and construct a block

Validators/Proposers: Validators execute the consensus mechanism to validate the blocks and broadcast them to the rest of the blockchain.

On pre-Merge Ethereum Mainnet, miners took on the roles of both builders and validators. For post-Merge, however, the separation between block proposer and builder, also known as the proposer-builder separation (PBS), was introduced. Node validators, under the PoS model, are only responsible for validating the blocks and have no role in block construction.

Types of MEV bots

Front-Running

This type of MEV exploit involves getting a transaction executed ahead of a known transaction in the mempool. For instance, if a bot spots a large trade, it copies the user’s trade and pays a higher gas fee to ensure top priority in the transaction order sequence of the block.

Back-Running

Back-running involves placing a transaction immediately after a known pending transaction. Searchers typically employ such bots to monitor the mempool for new token pair listings or liquidity pools created on DEXs like Uniswap. Upon discovering a new token pair listing, the bots can place a transaction order right after the initial liquidity and buy as many tokens as it can, leaving only a small amount for other traders to buy. The bot could then wait for price appreciation and flip the tokens to subsequent buyers.

DEX Arbitrage

This is the most common form of MEV seen today. Arbitrage opportunities are present when different prices exist between the exchanges. Due to its popularity and ease of implementation, DEX arbitrage is a highly competitive playground. Bots bid up gas fees aggressively, leading to high transaction costs for other users.

Liquidations

Liquidation is another well-known MEV practice. Searchers that specialize in MEV liquidations make money through liquidating leveraged positions (loans, perps positions, collateralized debt positions (CDPs), etc.). Liquidators run bots to either front-run or back-run transactions to be the first to liquidate someone’s collateral, instantly paying off the lenders. Liquidators get paid incentives from protocols and sometimes, enjoy a below-market discount to purchase assets that they can immediately sell for profit on other venues.

Sandwich Attacks

Sandwich attack bots are a variant of front-running bots – these bots place two transactions, one before and one after a target transaction. Searchers use this attack to extract MEV from unsuspecting traders on DEXs.

For example, a trader wants to buy 100K ETH with USDC on Uniswap. A trade of this size will significantly impact the ETH/USDC pair’s automated market maker (AMM) price. A searcher can then calculate the potential price effect of this large pending transaction on the ETH/USDC pair and execute a buy order right before the large trade, buy ETH at a cheaper price and then sell it right after the exploited trade at a higher price due to the price impact of that large trade.

Early MEV

Early MEV opportunities from DeFi activity enabled some blockspace to become much more valuable than others. For example:

- A DEX order with a large impact on the trading pool creates a back-running trading opportunity

- A poorly specified DEX order can be exposed to a sandwich attack, resulting in the blockspace before and after the transaction more vaulable

- Oracle updates enabling liquidations on borrowing and lending platforms can cause the blockspace to be more valuable after the oracle updates a transaction as the blockspace can be used for liquidation purposes

- Trading activity on DEXs can cause price dislocations between multiple DEXs, creating arbitrage opportunities

Priority Gas Auctions (PGA)

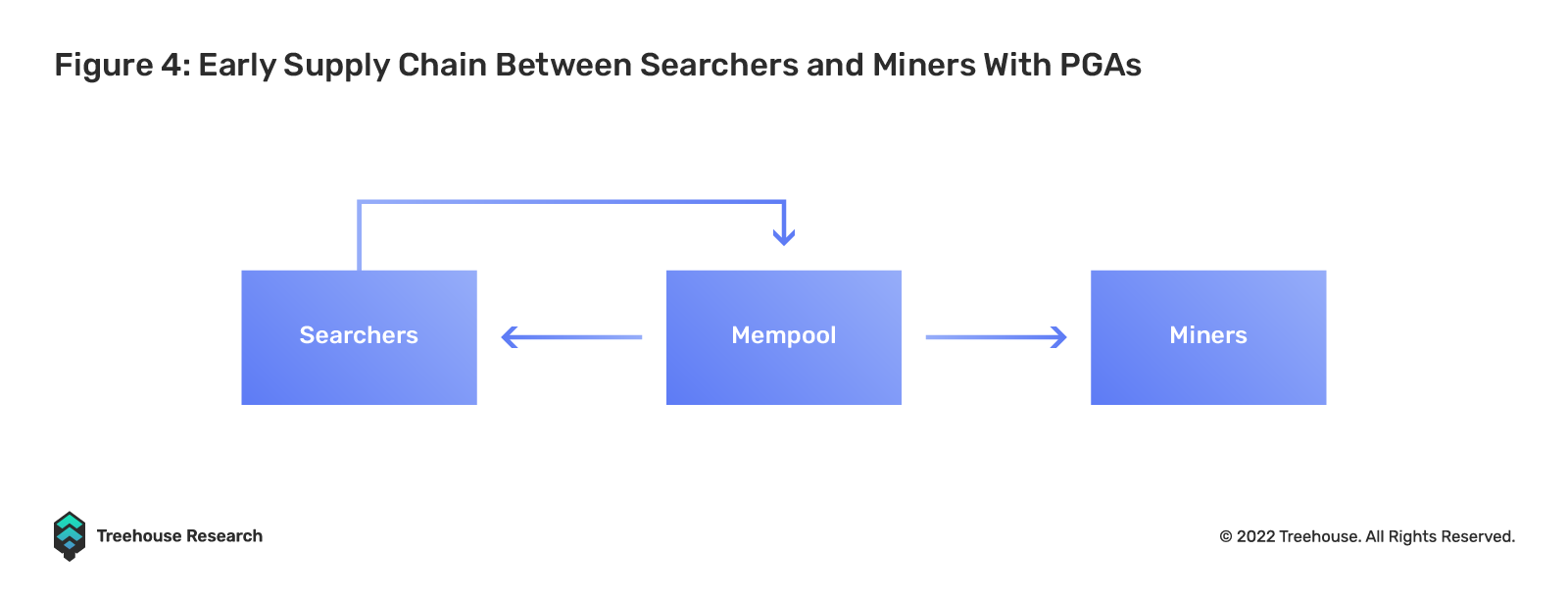

Previously, without a blockspace marketplace, searchers participated in Priority Gas Auctions (PGAs). To capture the arbitrage opportunities created at the top of the next block, searchers would submit arbitrage transactions to the mempool, bidding gas up until the transaction costs paid outweigh the arbitrage profits.

It was usually hard to get a specific blockspace in a block. One of the most common Ethereum clients, Geth (Go Ethereum), allowed individuals to run ETH nodes and order transactions by gas before randomly shuffling them. MEV searchers looking for back-run transactions needed to send their transactions as quickly as possible using the same gas as the target transaction. Because of the decentralized nature of Ethereum’s gossip network, the best strategy was to spam the network in the hopes of landing right after the target transaction. An update changed Geth to break ties by timestamp, thus lowering the incentive to flood the mempool with transactions, but there was still no explicit bidding process for valuable blockspace.

MEV extraction via PGAs brought some undesirable externalities to the Ethereum network. These include:

- Failed MEV extraction attempts landed in blocks, reducing blockspace for general users, as well as searchers’ efficiency by increasing their cost

- PGAs in the mempool involved spamming transactions which increased the load on every node operator

- Large fluctuations in gas prices caused some transactions to take a long time to land which also led to systematic overbidding by gas estimators. The issue has been mostly mitigated by EIP-1559.

- Miners with capabilities to extract MEV independently without relying on searchers had an advantage in mining since they could arbitrarily reorder, censor and insert transactions anywhere in the blocks they mined. This advantage was a centralizing force because sophisticated miners had better unit economics.

As on-chain activities picked up, more MEV opportunities arose, resulting in more network externalities.

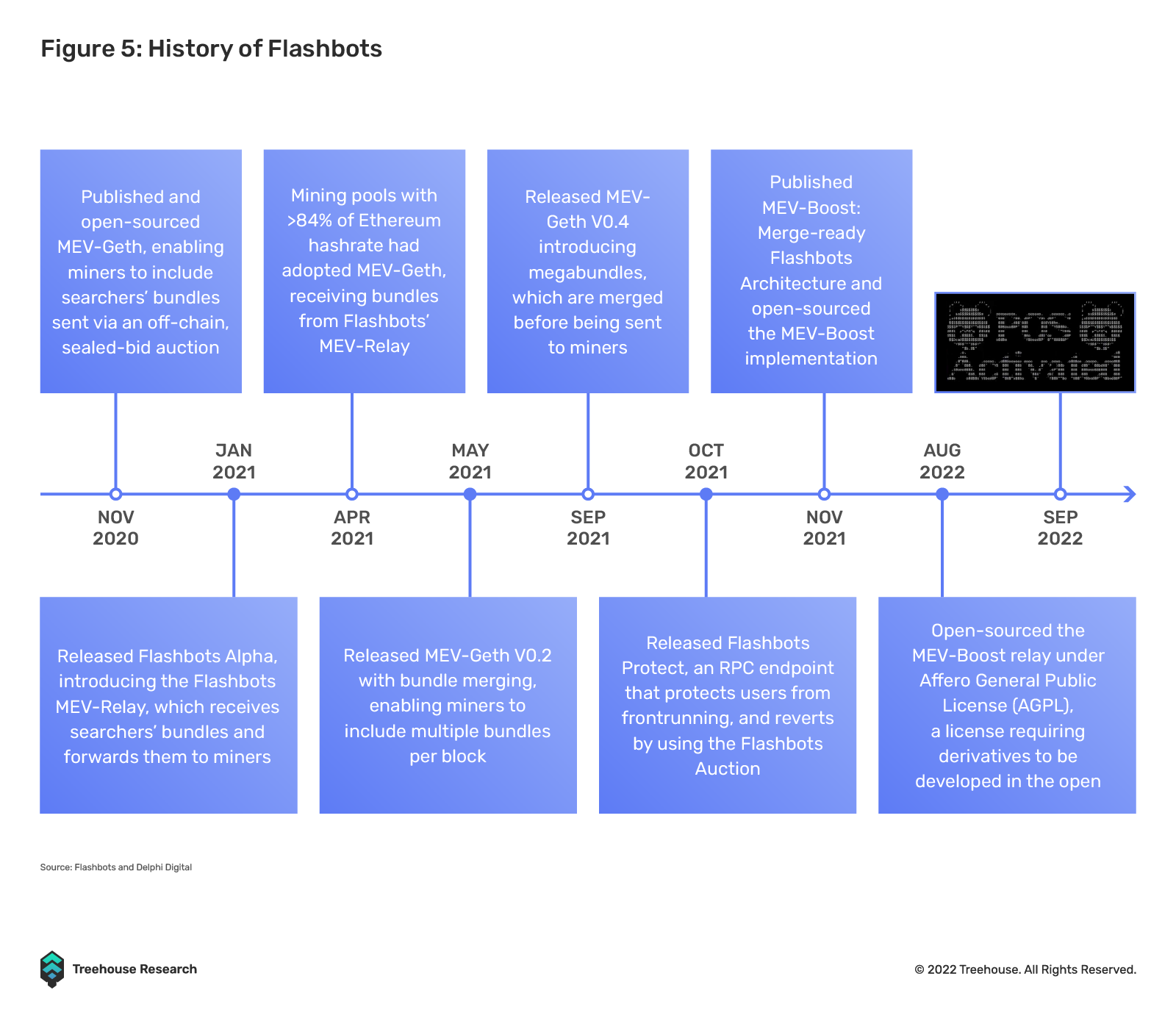

Early Flashbots

Flashbots is a research and development organization built to mitigate the negative externalities of MEV activities. Specifically, they aim to democratize revenue access, introduce transparency and redistribute revenue for MEV.

Flashbots Auction introduced an auction system for blockspace, which hosted auctions for specific blockspaces away from the mempool in a sealed-bid, private auction. It allowed for a more granular expression of preferences than the mempool PGA.

A canonical example of an MEV bundle is for sandwich attacks: with a poorly specified DEX trade B in the mempool, a searcher is able to specify a bundle consisting of a front-run transaction A placed before the actual transaction B, followed by back-run transaction C, where A and C are included if they land in this specific order.

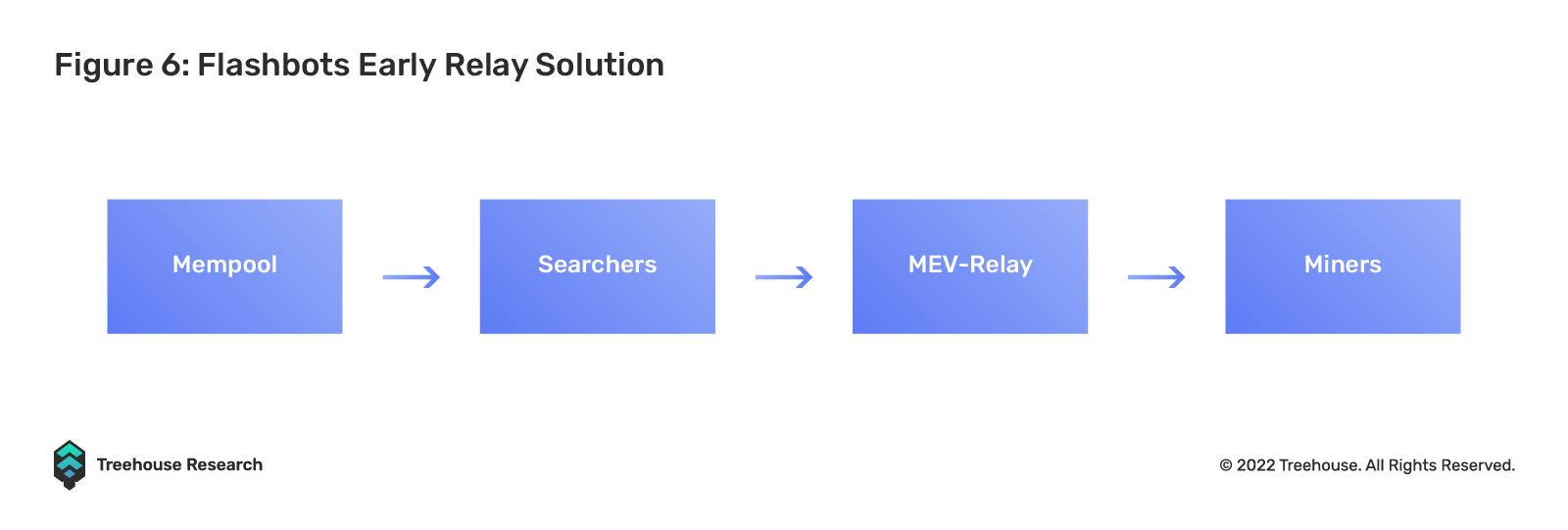

In Flashbots Auction, searchers send bundles with their bids to mev-relay, a private Flashbots-operated relay that prevents front-running by other searchers who did not bid in the auction. Participating miners would create blocks with the most profitable bundles they received through mev-geth. Carrying out the auction this way makes it more profitable for miners to run mev-geth than vanilla Geth.

Flashbots relay mitigated several aforementioned undesired externalities that PGAs brought about, optimizing Ethereum’s network activities in the following ways:

- Failed transactions and bundles are not included in the blocks, improving the efficiency of blockspace auctions and minimizing wasted blockspace

- MEV opportunities will become more competitive, limiting centralization at the miner level

- Blockspace auctions are migrated off-chain and without consuming unnecessary resources on-chain

- Current gas prices to reflect the real demand of the network with fewer spikes

In theory, multiple competing bundle relays can prevail, but once there is a single credible, compliant relay with a sizable market share, no searcher would be motivated to use a new relay unless miners comprising a sizable portion of hash power switched exclusively to the new relay. The mev-relay operated by Flashbots was dominant, but other systems such as Eden and alternate bundle relays operated by Etheremine and bloXroute had some market share as well. bloXroute, in particular, was able to establish itself where searchers used its mev-relay for better latency. In PoW, latency was vital to searchers as any delay could result in their bundles getting overlooked by miners.

In addition, there is no public auction system for end-of-block MEV opportunities. In theory, there should be no atomic arbitrage opportunities at the top of the next block: it should be extracted in the previous block. With the auction, miners are more likely to include end-of-block MEV trades so they can collect the MEV rather than the miner of the next block. The more MEV that can be extracted through the auction system, the less incentive miners have to develop their own MEV capability.

In this part, we discussed the evolution of blockspace markets in PoW with the inception of flashbots. Next, we will discuss the proposed blockspace markets in PoS.

MEV in the present

Ethereum PoS Structure

As Ethereum turned into a PoS chain, we know that the Beacon chain merged with Ethereum mainnet. What does this mean?

After the merge, block time will be fixed to 12 seconds rather than being generated from a Poisson distribution. Additionally, block proposers will be known ahead of time. This combination of fixed block times and pre-known block proposers will allow searchers to submit their bundles just before a block is going to be proposed. Searchers will tend to co-locate around large validators and best-performing block builders. In fact, some block builders may offer colocation as a service to searchers.

In the past PoW model, miners were responsible for the two roles of an executing client (bundling transactions) and a consensus client (validates/verifies the transactions after execution and puts them into blocks). With the merge, there is now a separation of the execution and consensus clients, as node validators now only take on the responsibility over the consensus. However, this does not stop validators (consensus) from still taking up the roles of the builders (execution).

PoS Ethereum prides itself on allowing anyone to spin up a node and become a validator given that they meet the 32 ETH stake requirement. This means that anyone who meets this requirement is technically able to participate in MEV opportunities. However, not many are familiar with conducting MEV as it is a specialized skill usually done by searchers and builders.

This separation at the client level has brought about the Proposer-Builder Separation (PBS) in MEV.

Introduction to Proposer-Builder Separation (PBS)

Proposer-Builder Separation (PBS) is a potential solution to the blockchain censorship and MEV attack problem where block building and block proposing are assigned to different roles in the network.

Under the previous PoW design, miners (both validators and builders) were able to capture a large portion of MEV by choosing which transactions to include in a block. This allowed them to front-run other users or conduct MEV attacks freely.

PBS mitigates this problem by separating the block construction process from the block proposal process. Builders would be selected by the highest fee they are willing to pay and proposers would simply select the exec header with the highest fee.

At this time of writing, PBS is simply a research idea and it is not being used natively by Ethereum or any other blockchain.

Current State of PBS

As mentioned, PBS is currently not implemented at the protocol level. This means that proposers (validators) are able to build their own blocks if they choose to do so. Down the line, the Ethereum network will look to implement this at its protocol level, which would change the way consensus is achieved.

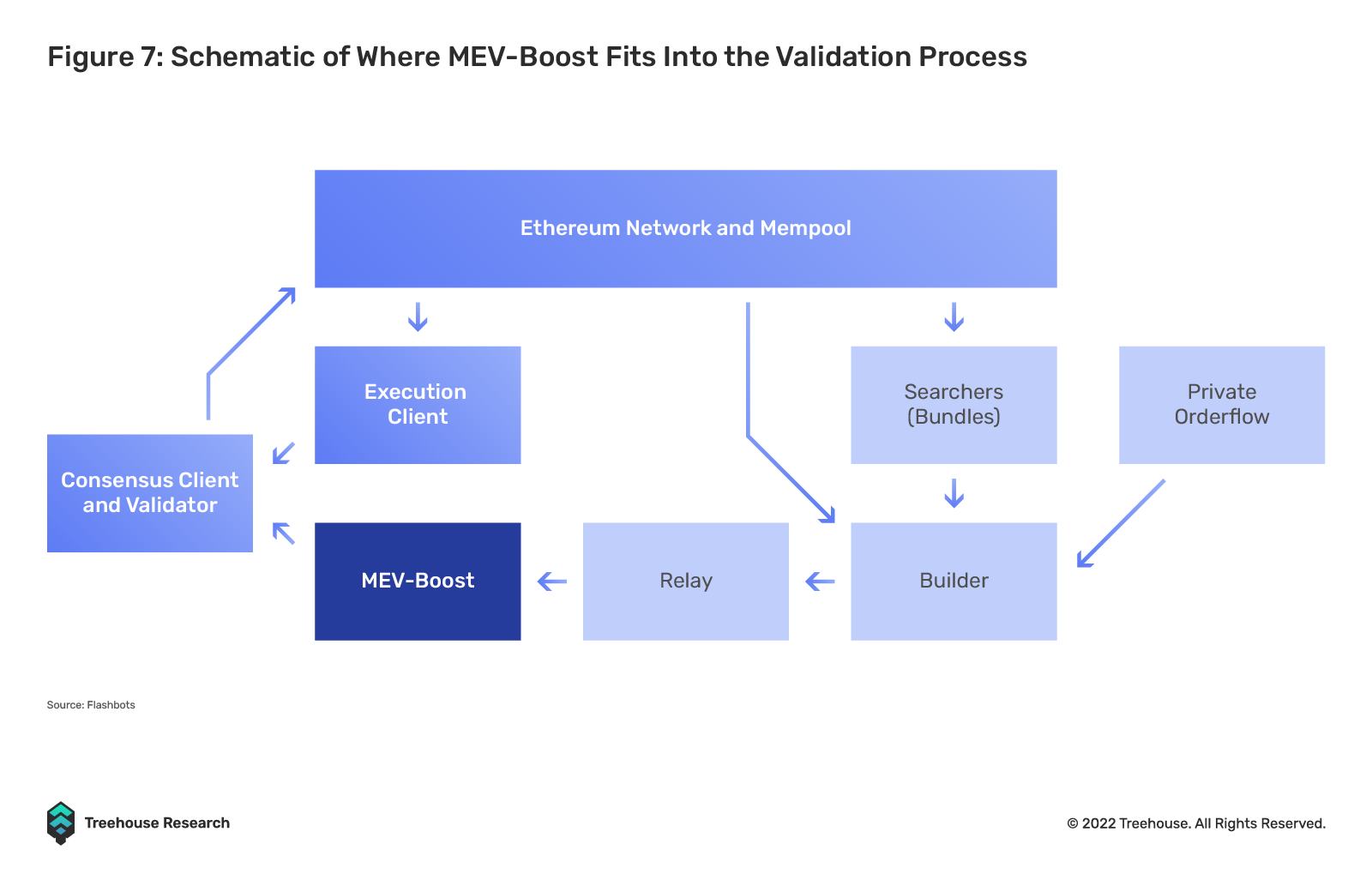

If a validator decides not to build their own blocks (due to opportunity cost reasons), they can opt into the MEV marketplace that we mentioned above by using a relayer, the most popular now being MEV-Boost developed by Flashbots. Flashbots previously attempted basic PBS in PoW Ethereum through mev-relay, mentioned in the previous section.

Relayers are, thus, the current implementation of PBS and they facilitate blocks between the “firewall” that separates builders and proposers.

Flashbots’ MEV-Boost

An implementation of PBS, called MEV-Boost, is currently used and is still under development in post-merge Ethereum. Validators who opt to run MEV-Boost can maximize their staking rewards.

This is how it works:

Since anyone can become a validator with the basic requirements, the prior MEV-Geth design does not work. If transactions are sent to solo validators, they can be incentivized to steal high-value MEV transactions for themselves. Furthermore, as mentioned earlier, if validators take on the roles of both builders and proposers, they can act as a centralizing force and most of the time, solo operators will not be as efficient as institutional ones.

Thus, the concept of “builders” came about in the introduction of MEV-Boost, Flashbots’ post Merge solution. Once again, builders solely focus on receiving transactions and building optimized blocks in which they will forward their blocks to proposers through a relay. Essentially, MEV-Boost acts as a relay aggregator, identifying the most profitable block and submitting it to the block proposer to validate its consensus to the rest of the network.

Effects of MEV: The Good, the Bad and the Ugly

There are many reasons to support MEV and its role in the blockchain ecosystem. Here, we will dive into the benefits and challenges it brings.

The Good Side

The proponents of MEV argue that MEV ensures the relevance of DeFi projects such as lending/borrowing protocols, enabling them to achieve quick and smooth liquidation processes. The argument here is that MEV extractors are rational actors that are fixing economic inefficiencies of DeFi protocols, making them more robust in return for an extractable reward.

Flashbots belong to this camp and they are working on mitigating the negative externalities of current MEV extraction techniques. Flashbot’s products enable a permissionless, transparent and fair ecosystem for MEV extraction. The goal is to lower the barriers to entry while allowing all validators to extract MEV at the equivalent rate. The MEV derived can also be redistributed to public goods funding, thus improving economic security.

The Bad

On the other hand, there are obvious reasons MEV leads to a worse user experience. Particularly, it results in costlier transactions fees, eating in your profit margin. Front-running and sandwich attacks, for example, cost users millions of dollars in lost arbitrage opportunities and increased price slippage at the application/user/wallet layer.

Because of the existence of front-running bots, arbitrage trading is an unwinnable game for inexperienced traders. This negatively impacts the proposed functionality of DeFi protocols that rely on third-party arbitrage to function properly. The presence of MEV bots makes it difficult for real arbitrageurs to participate in such protocols, which harms the protocol’s security.

Furthermore, generalized front-runners compete against each other at the network level by raising gas prices. These actions frequently leads to network congestion and high transaction fees, making it inefficient and expensive. This caused network users to suffer as a consequence.

The Ugly

There are arguments claiming that MEV worsens the network at a protocol level. For example, for any given block, if MEV rewards are larger than block rewards for any given block, this might entice validators and miners to reorganize blocks and destabilize the network’s consensus.

Depending on who you ask, allowing validators or miners to reorganize and reorder transactions in blocks for profit may be viewed as violating the entire premise of blockchains being a secure, immutable and permissionless technology. It also makes these actors take an active role in influencing transactions and balances, as opposed to neutral parties competing for different benefits. This threat has already manifested itself on other networks. Before the Apricot Phase Four upgrade on Avalanche, any validators could propose a block. When one validator proposed a block with meaningful MEV rewards, other validators could “ steal” the MEV by publishing a longer chain of blocks. As a result, a race to reorganize and reorder transactions emerged.

Other Players

Apart from Flashbots, many other players have entered the MEV space, partly due to Flashbots’ open-source technology stack and the submission of blocks to other relays.

MEV Relay

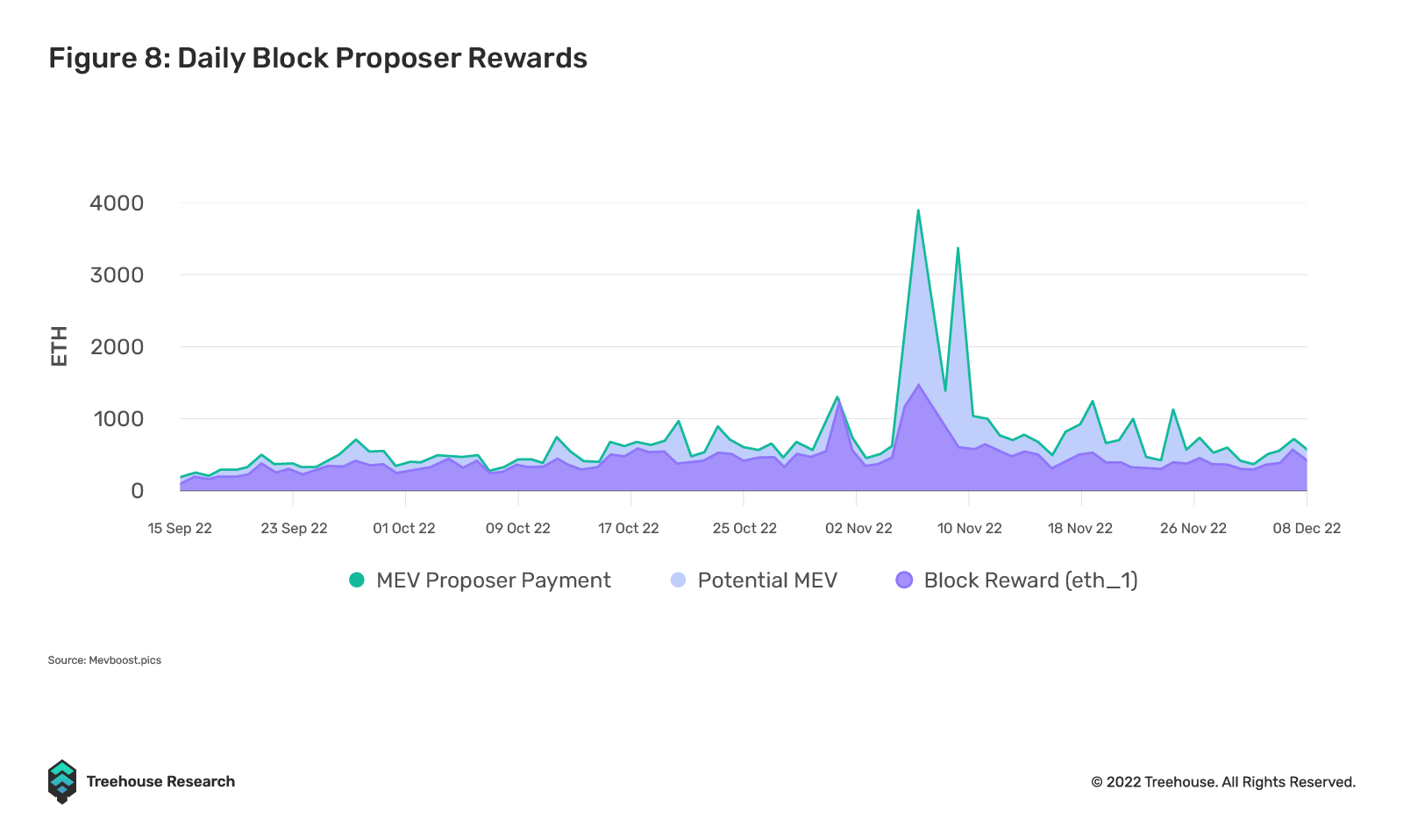

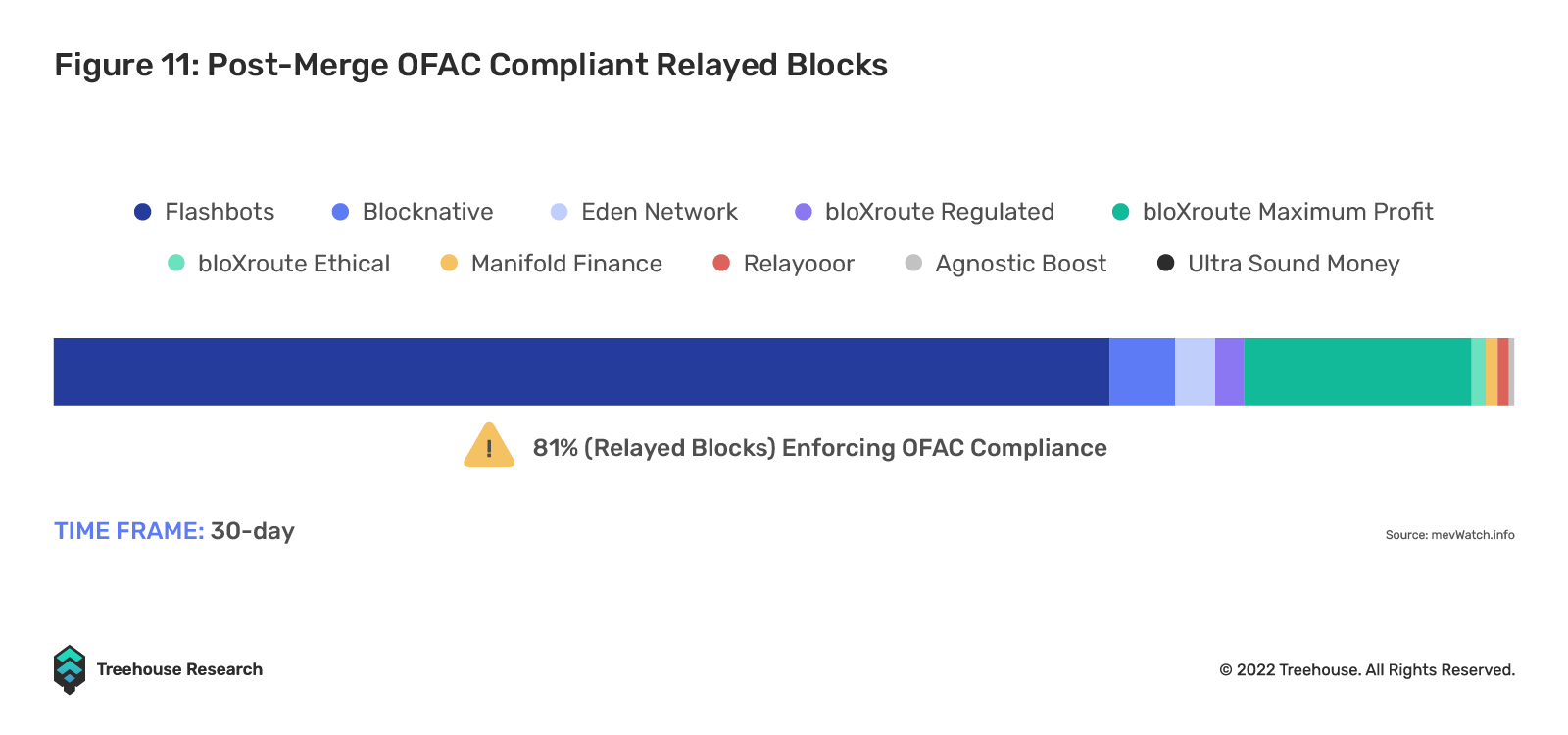

It is clear for all to see the impact of MEV relays on the Ethereum chain. As MEV-Boost helps extract MEV for validators to earn extra income, MEV relays are increasingly relied upon in block building. Validators who opt-in to MEV-Boost see an average of 37% increase in rewards with more than 60% of validators choosing to run MEV-Boost over producing their own blocks.

Flashbots is undeniably the most dominant player in this space. It has relayed the largest percentage of MEV-Boost blocks at around 70% (in the past 14 days) at the time of writing, with MEV-Boost blocks accounting for 80% of the total block market. This is followed by bloXroute (Max Profit) at around 18%. The discrepancy between the two highlights how dependent the market is on Flashbots.

Beyond Flashbots, there are four other relays for block building: bloXroute, Eden Network, Manifold and Blocknative. They each run their own relays and other MEV-related products such as private remote procedure call (RPC) services. Most of them also run their own block builders and may even capitalize on orderflow sent to their builder via their private RPC. These protocols provide an alternative for validators to rely upon for the most profitable block header before finalizing the chosen block on-chain.

Relayers have strong network effects as many entities rely on them for the most productive and efficient block production. As more block builders submit their blocks to a relayer, more validators are incentivized to rely on the relay for the most profitable blocks. As more validators utilize the relay to finalize the block, block builders and MEV searchers (sometimes they are the same party) will submit their bundles and blocks to the same relay. This is why Flashbots still dominates the marketplace despite other players entering the space.

Flashbots’ dominance is not as apparent in the builder market. Flashbots’ builders have also contributed to about 21% of MEV-boosted blocks (in the past 14 days) where the space is much more fragmented as compared to relays. This could be due to other relays isolating themselves from Flashbots builders as this will adversely impact their bottom line. Relays are able to generate more income by relaying the blocks they created rather than relaying blocks they did not create.

Drawbacks: Censorship

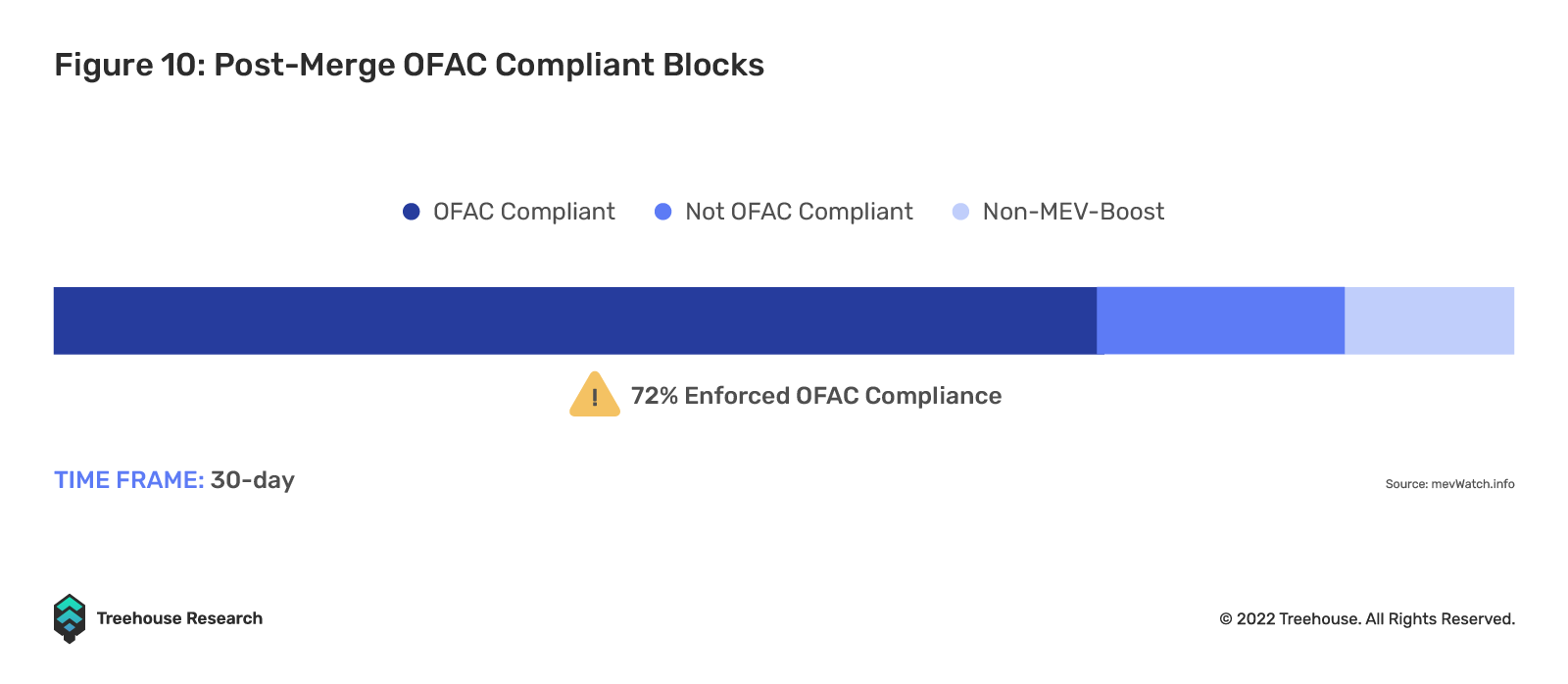

As the space evolves, a new looming issue now plagues the block-building vertical: censorship. This surfaced when the US Treasury Department’s Office of Foreign Asset Control (OFAC) banned US citizens from using Tornado Cash, a service that anonymized transactions. Tornado Cash has come under the spotlight because it has been used for laundering of money obtained through hacks and bugs.

Flashbots has sparked controversy due to its decision to censor the default relay. The relay will exclude transactions involving addresses linked to Tornado Cash and other OFAC-sanctioned addresses as the team aims to be OFAC-compliant.

Currently (at the time of writing), 64% of all blocks have stopped attesting to non-censorship blocks with all of the blocks created by Flashbots, Eden Network and Blocknative to censor Tornado Cash transactions. Only 4% of blocks proposed by relayers remain uncensored.

However, PoS block production remains more censorship-resistant than the data suggests as the censorship risks are limited to block builders excluding transactions at the moment. Fears of a chain split are unfounded as validators continue to build on top of previous blocks containing transactions from blacklisted wallets. About 36% of blocks will continue to include Tornado Cash transactions and the rest will continue to build on top of it.

In addition, validators who are concerned about the issue of censorship can opt for non-censorship solutions such as bloXroute. Validators can always connect to multiple relays to bypass the issue of censorship. As such, censorship risks are overblown as validators themselves are not incentivized to switch relayers from boycotting Tornado Cash transactions.

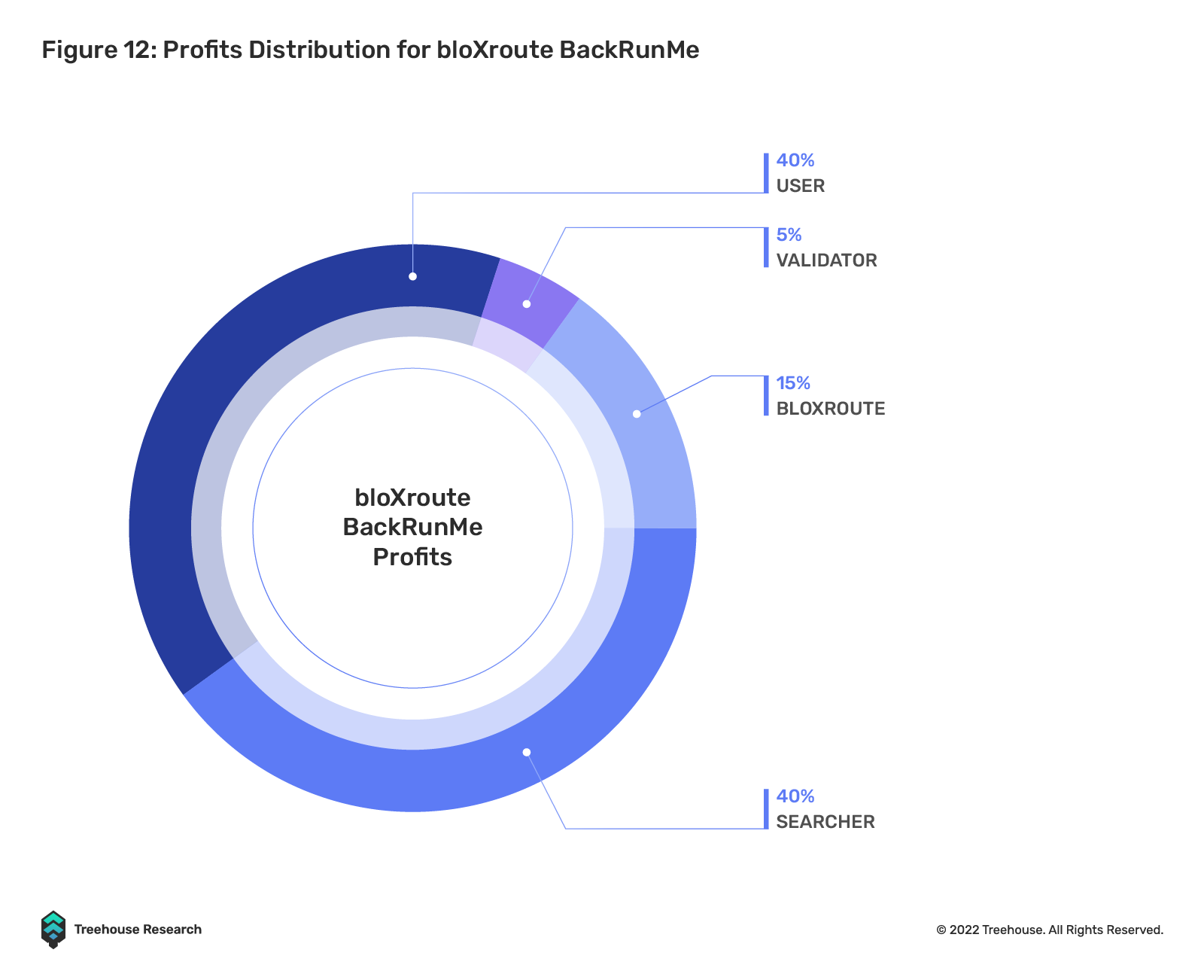

Back-running Service – bloXroute

bloXroute BackRunMe is a service that allows users to dodge front-running and sandwich attacks by safely submitting private transactions while authorizing searchers to extract positive MEV value from their transactions if the transaction creates an arbitrage opportunity. The most important part of BackRunMe is that a large portion of this additional profit captured by the searchers will be rewarded to the users. If a backrun transaction occurs, the profits (after the deduction of block base fee) from the backrun transaction are split among the participants in the following manner:

Matching Coincidences of Wants – CoWSwap

CoWSwap’s approach to tackling MEV is to build a matching engine. It seeks to facilitate user transactions by matching Coincidences of Wants (CoWs). This is essentially an order book mechanism where two parties each have what the counterparty wants. The protocol facilitates this transaction through an off-chain order book where entities, known as solvers, match these orders. If there are no matches, the orders will then be routed to an on-chain DEX to be executed. By matching orders directly against each other off-chain, the threat of sandwich attacks is now eliminated.

Exclusive Order Flow – Manifold and Rook

The teams at Manifold and Rook have decided to tackle of MEV issue through the principles of exclusive orderflow (EOF). Much of the MEV opportunities originate from the user’s intent and transaction orderflow. The orderflow is then routed to the public mempool or through a private RPC endpoint. EOF refers to the latter, which public mempool searchers and builders are not privy to. In TradFi, there is a similar concept known as payment for order flow (PFOF) where retail orderflow are sold to market makers. This is how Robinhood earns revenue, instead of charging transaction fees. Robinhood sells users’ orders to market makers while offering some rebates back to users.

Manifold has partnered up with Sushi for this very reason. All of Sushiswap orders are exclusively routed through the Manifold private RPC relay, known as SecureRPC. Manifold proceeds to extract as much MEV as possible from its OpenMEV strategy and redistributes the profits back to $FOLD stakers and Sushiswap in equal proportions. This is accomplished through back-running on orders. While Manifold mainly derives its EOF from dApps, users are also able to send transactions through its private relay SecureRPC for protection against searchers.

As for Rook, the project targets users and dApps alike for EOF. Users are able to submit their transactions through Rook, which also has a private relay to shut off public searchers. Rook’s assigned “keepers”, who are essentially searchers on Rook, bid for the right to execute your transaction. A portion of the bid returns to the user while the keepers use proprietary methods to build profitable bundles, preventing MEV from being extracted by the block producer when the transaction is settled.

EOF has gotten more attention with the implementation of MEV-Boost. This is because EoF has huge market potential and could potentially threaten MEV decentralization through vertical integration. Block builders are most concerned with building the most lucrative block and EOF allows certain builders to gain an unfair advantage over the rest with exclusive orderflow. The ones who control orderflow control the Ethereum block production. Currently, majority of the relays accept blocks permissionlessly and have no plans to enter the builder space. Transactions sent sent through relays can be settled by any block builders. This is beneficial to both the users (higher chance of transaction inclusion) and the network.

Fair Sequencing – Arbitrum and Chainlink

Arbitrum has a different view on tackling MEV. They have been vocal against MEV Auction1 and have designed different modules and evaluated each of their potential impacts on L2 MEV.

Currently in their mainnet beta, the initial release involves a single sequencer, an entity given special privilege to reorder the latest transactions within a narrow window of 15 minutes. There is still inherent trust that the sequencer will not front-run. In the next phase, Arbitrum aims to have a distributed set of independent parties controlling the sequencer. The parties involved will collectively propose state updates through an algorithm that enforces fair ordering (Aequitas). MEV can only be possible if there is more than one-third of the sequencing parties colluding.

In order to execute this vision, Arbitrum is collaborating with Chainlink to implement order fairness. Chainlink has been developing a solution since 2020 called Fair Sequencing Services (FSS). FSS will result in the user transactions being encrypted to hide transaction details, ordered by a decentralized oracle network (DON) and then decrypted by the Arbitrum protocol. The transaction payload will not be visible to nodes before the ordering process, thus eliminating MEV. By implementing Aequitas ordering (consensus) protocols into FSS, the transactions are not only encrypted but also enforce a “first-in, first-out” mechanism that will help to facilitate fair user transactions.

This approach is not without its limitations as the same MEV vulnerabilities now lie within the decentralized oracle network. The sequencer would become a network of observers and there are no watchers to prove that the network nodes have actually arranged the transactions in the order that was presented to them. As noted by Arbitrum, the sequencer inevitably has stronger MEV capabilities than the L1 validators. In order to limit L2 MEV capabilities, there need to be sufficiently large entities controlling the sequencer to prevent collusion.

Ongoing and Future Developments of MEV

Traditional Cross-Chain MEV

Let’s say there is a discrepancy in the price of an asset on Uniswap Ethereum and Uniswap Arbitrum. For example, if the price of ETH is $1,800 on Ethereum, but $1,780 on Arbitrum, there would be an arbitrage opportunity here. But how could one do so?

- Bridges: Purchase ETH on Arbitrum and use a bridge like Stargate or Across Protocol to move ETH to its L1.

- CEX: Some exchanges accept deposits directly from Arbitrum.

- Proprietary Balance Sheet: Hold a mix of ETH and USDC on two different chains and conduct arbitrage whenever the opportunity arises. Rebalance when needed to ensure sufficient inventory on both chains.

These options are viable ways to conduct and extract MEV, however, they are time intensive as using bridges and depositing to CEXs usually take some time (around 5 to 20 minutes regardless of the chain). Option 3 will capture the opportunity virtually all the time, but do note that it is also capital intensive, where it favors professional market makers and institutions.

This dynamic is special because it incentivizes collusion between multiple chains. Since executing cross-chain MEV is probabilistic, an institution could set up validators across different chains to reduce risks and more efficiently capture MEV.

The Cosmos AppChain

An AppChain is a blockchain that dedicates its blockspace to a specific application. Applications that build AppChains can customize multiple layers of their stack, such as their security model, fee token and write permissions, among others. Having precise control over the entire stack: execution, consensus, blocksize, timing, state and mempool logic, validator requirements and any other area of blockchain structure and operations which are customizable.

Because they are interoperable, AppChains can freely and composably interact with each other over their Inter-Blockchain Communication Protocol (IBC). Moreover, AppChains are also excellent at handling MEV: the profits are available to whoever can decide transaction ordering and block inclusion. MEV has plagued DeFi users not just on Ethereum, but on many other ecosystems. AppChains are able to quickly develop on-chain solutions that could reduce the negative externalities and redirect healthy arbitrage profits from third parties to themselves.

Osmosis, for example, is working on a private mempool with threshold decryption (an experiment of Ethereum too). Because these private transactions are hidden from nodes until they are executed, front-running becomes more difficult. Similarly, AppChains can set aside the first slot in their blocks for protocol-controlled arbitrage and liquidations – a necessity for the health of trading and lending protocols. Ultimately, Osmosis strives to direct these healthy, non-user-harming arbitrarge profits back to the DAO.

The remaining (heavily reduced) MEV can also be partially captured in-app by auctioning off the second slot in the block on-chain, to MEV searchers like Flashbots. Alternatively, it sounds logical for chains to aggregate all the second-slot auctions in one venue, as the Cosmos Hub proposes to do, such that the cross-chain MEV marketplace is transparent and not a “dark forest”.

Enshrined PBS

With MEV-Boost, “relayers” receive blocks from block builders and submit them to validators for inclusion. Once Ethereum introduces PBS at the protocol level, there will not be a need for relayers since the mechanism of “relaying” data will be in-built.

With centralization risks, come censorship risks. However, relayers do not have the incentive to censor transactions since they would leave money on the table if they did so. However, relayers can be coerced into transaction censorship by governments as we are seeing the number of censored blocks increasing tremendously now. In an ideal situation, there should be enough relayer diversity such that relayers not operating in that nation-state can still pick up those transactions, being incentivized to do so by capturing a larger share of profits.

Enshrined PBS has a solution called censorship-resistant lists (crLists). Enshrined PBS could use crLists to replace relayers. This scheme gets block proposers to create a list of transactions called the crList that have the correct nonce, sufficient balance and sufficient priority fee.

Conclusion

The MEV landscape has changed considerably since the Merge and the introduction of Flashbots’ MEV-Boost relay. The issues surrounding MEV are everchanging as development in the space continues. There are still those who profit from MEVs by exploiting them, though various solutions have surfaced to negate these exploitations. Drawing references from TradFi, MEV is likely unavoidable but there are ways to mitigate or prevent predatory behaviors from spiraling out of control.

Footnote

1 MEV Auction refers to auctioning off the right to decide the order of transactions and letting the auction winner extract all the MEV. https://ethresear.ch/t/mev-auction-auctioning-transaction-ordering-rights-as-a-solution-to-miner-extractable-value/6788

Acknowledgement

Special thanks to Flashbots, bloXroute, Manifold Finance and Rook for their feedback on this article.

Disclaimer

This publication is provided for informational and entertainment purposes only. Nothing contained in this publication constitutes financial advice, trading advice, or any other advice, nor does it constitute an offer to buy or sell securities or any other assets or participate in any particular trading strategy. This publication does not take into account your personal investment objectives, financial situation, or needs. Treehouse does not warrant that the information provided in this publication is up-to-date or accurate.

Hyperion by Treehouse reimagines workflows for digital asset traders and investors looking for actionable market and portfolio data. Contact us if you are interested! Otherwise, check out Treehouse Academy, Insights, and Treehouse Daily for in-depth research.