Introduction to DOVs

Most DeFi users would have heard of yield farming. It was once beloved and embraced by investors. After all, the yields offered start from high double digits and can go up to astronomical Ponzi-like amounts when most farming in the early DeFi summer did not require a lock-up period, i.e., duration is zero. Compared to the TradFi fixed-income market, which offered negative real yields for tens of years of duration, it was easy to understand why many got excited over these opportunities.

However, the initial high yields quickly dissipated as protocols mainly subsidized them to attract users – still, remember Uber/Lyft/Grab free rides when the battle for ride-hailing market share was at its most intense? As protocols emulate this competitive spirit in the name of “user adoption”, we have seen projects stumbled and bowed out, much like Uber in Singapore. Though some end users reap the short-term benefits, some are bound to be left holding the bag when the funds dry up. Ultimately, these unsustainable returns in the DeFi yield farming have led to a natural pursuit of organic yield-generating from volatility or option selling in layman’s terms.

Options have been an integral part of the TradFi market. They can be used to express a directional view, profit from volatility, and LEGOed to form structured products. These vehicles, when implemented correctly, can offer superior risk-adjusted returns payoff that exceeds simply buying and holding spots. Furthermore, options selling had become an important yield-generating source in TradFi, especially in stocks/FX. Typically, yield-seeking investors are sellers of options against asset owners who buy options to hedge spot holdings. A liquid options market is critical to further adoption of crypto & DeFi as it opens up another dimension beyond spot price movement. Nonetheless, option strategies are highly complex, and not everyone has the time or the knowledge to execute these strategies in a timely manner. Enter, DeFi Options Vaults (DOVs).

DOVs provide easy access for users to deposit funds and earn yields based on the predefined option strategy, which is made up of a single or multiple leg structure. Prior to the creation of DOVs, option strategies were only available to accredited investors through over-the-counter (OTC) trading or by self-execution on options exchanges like Deribit or Opyn. Similar to yearn, DOVs allow investors to simply deposit their assets in the vaults, which will then execute yield-generating strategies on behalf of the investors.

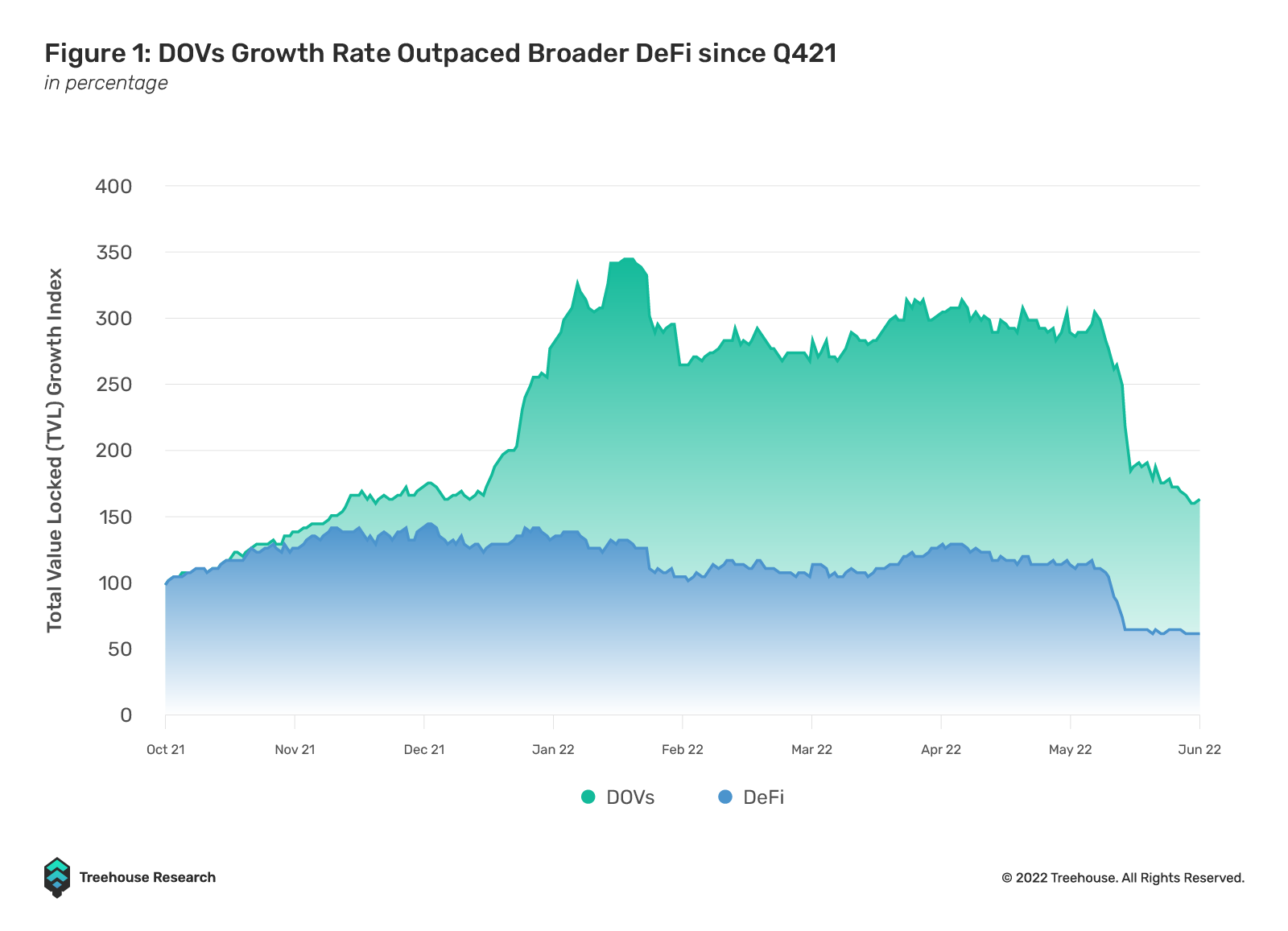

At the start of Q421, DOVs were growing at a similar pace to the broader DeFi market but began to explode by December 2021, when it was significantly outgrowing the entire DeFi sector. Within 3 months, TVL managed to expand by ~3x its size and showed its resilience despite the bear market conditions seen at the turn of the year.

There are a few reasons why DOVs have been popular lately and will continue to be in the DeFi landscape. Firstly, DOVs can generate organic yield by monetizing the volatility of underlying assets. Crypto options can be a great source of yield, and implied volatility tends to be higher than realized volatility, also known as the variance risk premium.

Secondly, DOVs allow for scalable trading of non-linear instruments on DeFi. Centralized exchange offering options are having a hard time scaling their option offering due to fragmented liquidity on limit order books. DOVs solve this problem by concentrating option liquidity on specific or a range of strike prices at predetermined tenors. This greatly improves liquidity, allowing a wider variety of options to be traded on DOVs. The improved liquidity will inevitably spread in CeFi as exchanges will confidently list altcoin order books knowing that demand already exists in the DOV space.

In this article, we will look at the intricacies of DOVs, evaluate the different types of DOVs, and provide our outlook on the landscape.

The Inner Workings of DOVs

The most common structured product DOVs implement are covered call selling or cash-margined put selling strategies. By selling call options with a higher strike price than the current token price, covered calls generate yield for a token (out-of-the-money call options). Option buyers pay a premium for the options contract, which is then returned to the vault as yield for depositors. Cash-margined puts are identical to token-margined calls but in the opposite direction. Refer to the appendix for a more in-depth breakdown of a covered call and put selling strategy.

How Does the Vault Execute the Strategy?

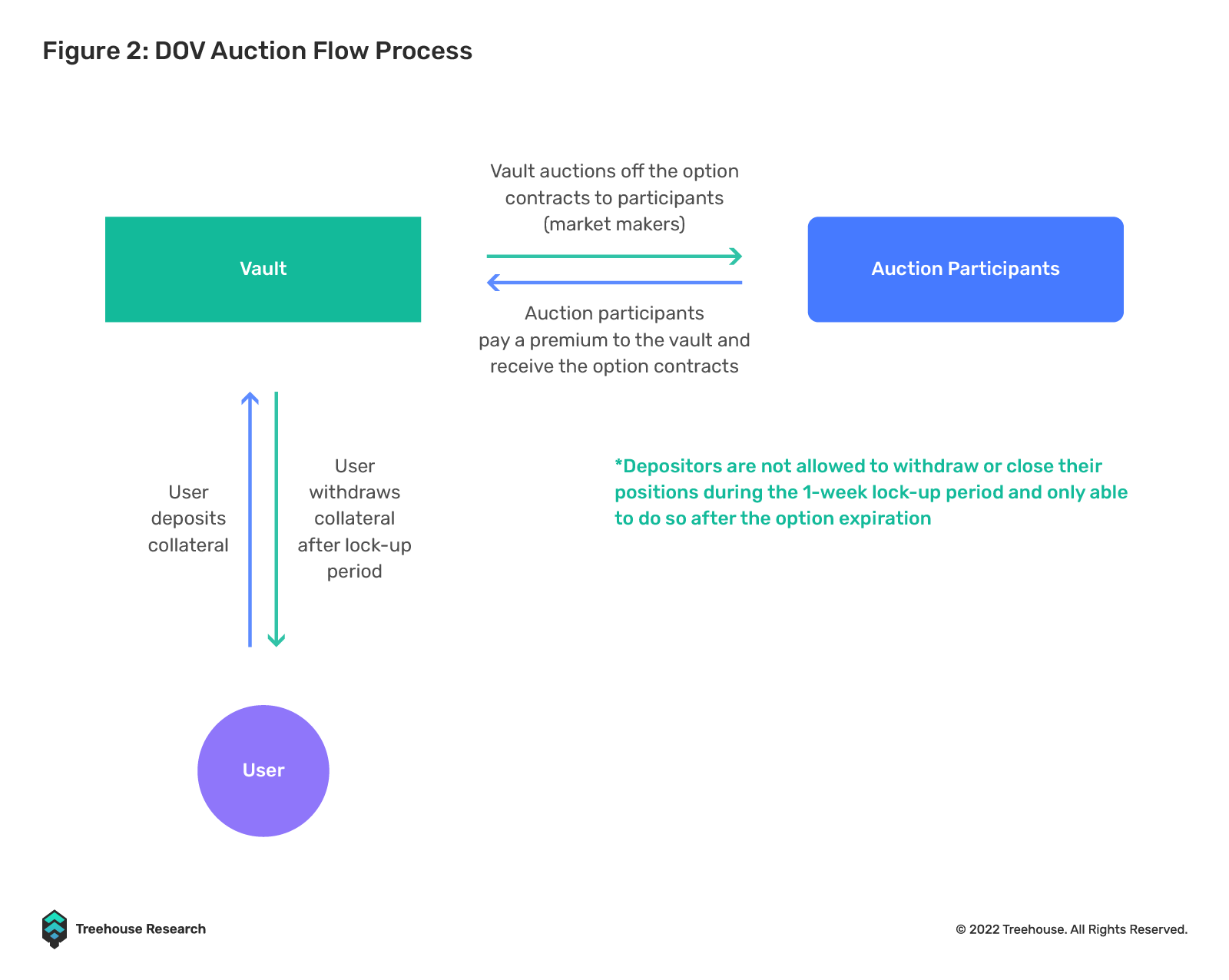

Vaults open for traders to deposit their collateral into the respective strategy that they wish to engage in. Traders deposit underlying tokens for call selling vaults and stablecoin for put selling vaults. The vaults will write the options weekly and auction them to market participants on a predetermined day and time. Note that different protocols have their own mechanism for minting and selling the options to authorized participants. Investors are advised to understand how each protocol functions before investing in the vaults. The protocols decide option parameters such as strikes and tenors based on backtested results to yield the highest risk-adjusted returns for depositors.

After auctions, the vault receives the premium. On expiry, vault depositors can either withdraw their deposit with the premiums or keep it in the vault to participate in the next auction. Depending on the strategy performance, the balance in the vault may either be higher or lower than the previous week.

Existing DOV Protocols

Many existing DOV protocols are deployed on various blockchains with the same goal: to generate yields for investors. However, not all of them operate similarly, and some have devised previously unthinkable strategies to increase the variety of ways to generate yield via vanilla derivatives. Despite most of them having similar strategies (covered call or cash-secured puts), performance across DOV protocols may differ due to the different execution mechanisms, micro-strategies, and additional yield overlays.

Ribbon Finance

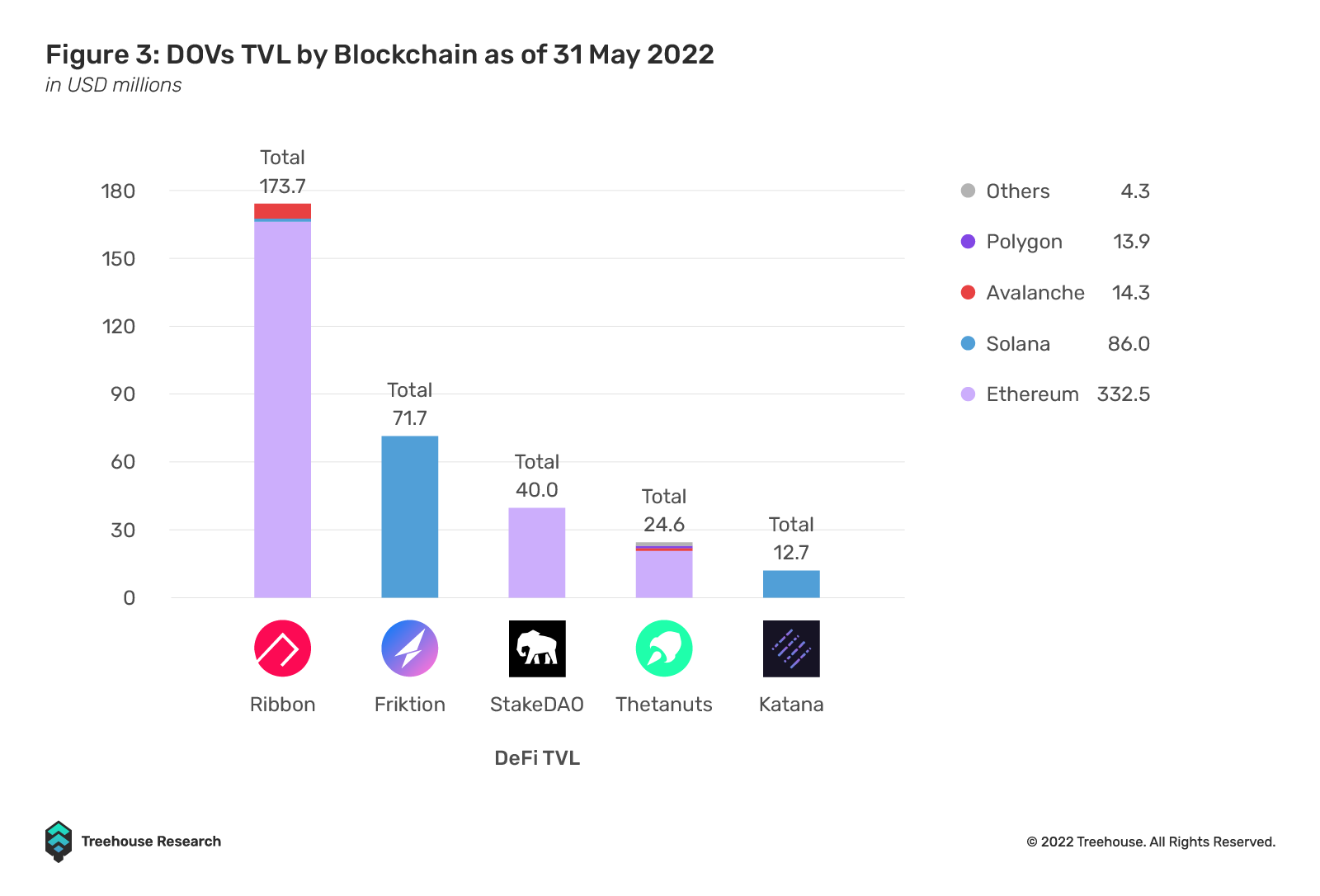

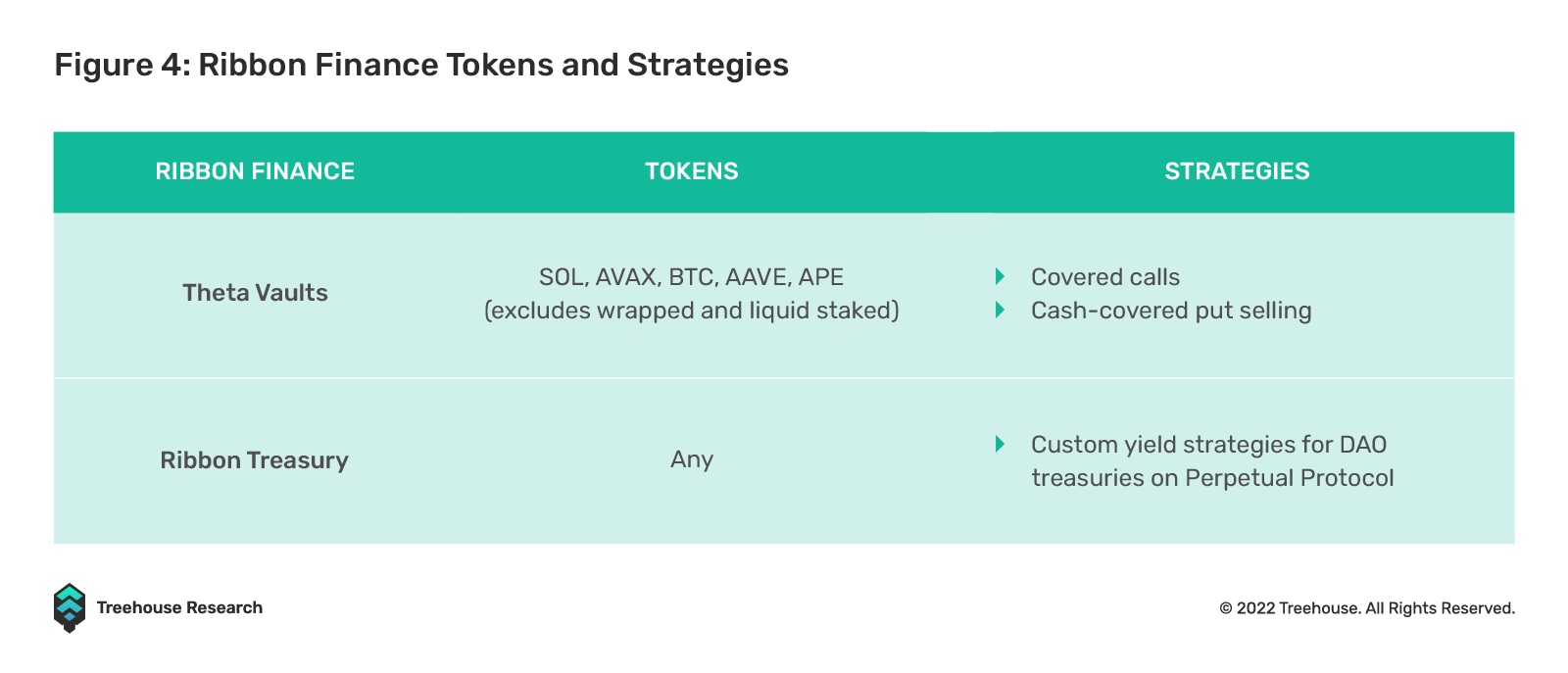

Ribbon Finance is a pioneer in the space of DOVs, allowing users to access crypto-structured products for DeFi. Ribbon Finance’s flagship product, Theta Vault, lets users deposit assets and earn yield through various options strategies. As of today, Ribbon Finance offers 11 different vaults spanning five different tokens for both put selling and covered call strategies. Ribbon Finance went live on the Ethereum network on 12 April 2021. Since its inception, Ribbon Finance has generated over $38M1 in revenue from its vaults. Recently, Ribbon Finance has undergone several architectural changes to its vault design and structure. Its recent V2 upgrade features more decentralization of its vaults. Some highlights include algorithmic strike selection, governable vault parameters, and revamping their fee model.

Ribbon Finance has raised a seed round of funding from Dragonfly Capital, Nascent, and Coinbase Ventures, among others. Ribbon Finance’s peak TVL was over $300M, making it the leading DOV protocol in terms of TVL among its peers.

Aside from participating in yield-generating strategy vaults, supporters can also purchase the RBN token, which is the protocol’s native governance token. Token holders gain voting power to decide on protocol parameters and receive weekly emissions from revenue generated by the protocol. Holders of RBN can also lock their tokens on the governance portal to maximize their veRBN (vote-escrowed RBN) voting power.

StakeDAO

StakeDAO started as a yield aggregator similar to Yearn Finance but has since expanded into other yield offerings such as arbitrage vaults, staking-as-a-service, and DOVs. While yield aggregation vaults continue to account for a considerable portion of the protocol’s TVL, it has witnessed tremendous growth in its options vaults during Q4. Launching its first option vault on 19 August 2021, it has three vaults centered mainly around BTC and ETH. These three vaults operate similarly to Ribbon vaults. Both protocols use Opyn as an options marketplace to underwrite their options.

StakeDAO distinguishes itself primarily by aggregating yields from its yield aggregation vaults and options vaults. Assets put in StakeDAO option vaults are immediately transferred to the platform’s passive yield vaults, generating an additional yield on top of the option premium earned. StakeDAO also allows users to stake the LP tokens received from the option vaults to earn SDT tokens, juicing up the yields. While Ribbon has shifted to an active fund management fee model, StakeDAO charges zero platform fees on assets or profits but charges a 0.50% withdrawal fee. StakeDAO recently has been actively building on the Curve ecosystem, supporting several Curve-based assets and strategies.

Thetanuts

Thetanuts is a cross-chain structured products protocol designed for everyday investors, radically simplifying the yield earning process and providing exposure to options. Thetanuts officially launched on 1 December 2021 and is now available on the Ethereum, Avalanche, Binance Smart Chain, Polygon, Fantom, Aurora, and Boba networks. It has aggressively deployed onto new chains, securing over $24M in TVL.

Thetanuts does not charge fees for its vaults and utilizes off-chain auctions to option trading firms such as QCP Capital and Paradigm. This allows them to offer options on differentiated underlying as they are not constrained by on-chain collateral availability.

Thetanuts recently concluded an $18M seed round led by Three Arrows Capital, Deribit, QCP Capital, and Jump Crypto.

Thetanuts stands out from other DOVs protocols via its Thetanuts Stronghold Strategy. Stronghold is the aggregation of multiple Thetanuts basic vaults to create an index token representing the pro-rata fair value of the constituent vaults. By exchanging tokens for Stronghold indexed tokens, investors are essentially investing in a pool of strategies that the protocol has optimized based on backtesting and periodic adjustment of parameters. This is similar to a volatility risk premia harvesting hedge fund but on-chain and without fees.

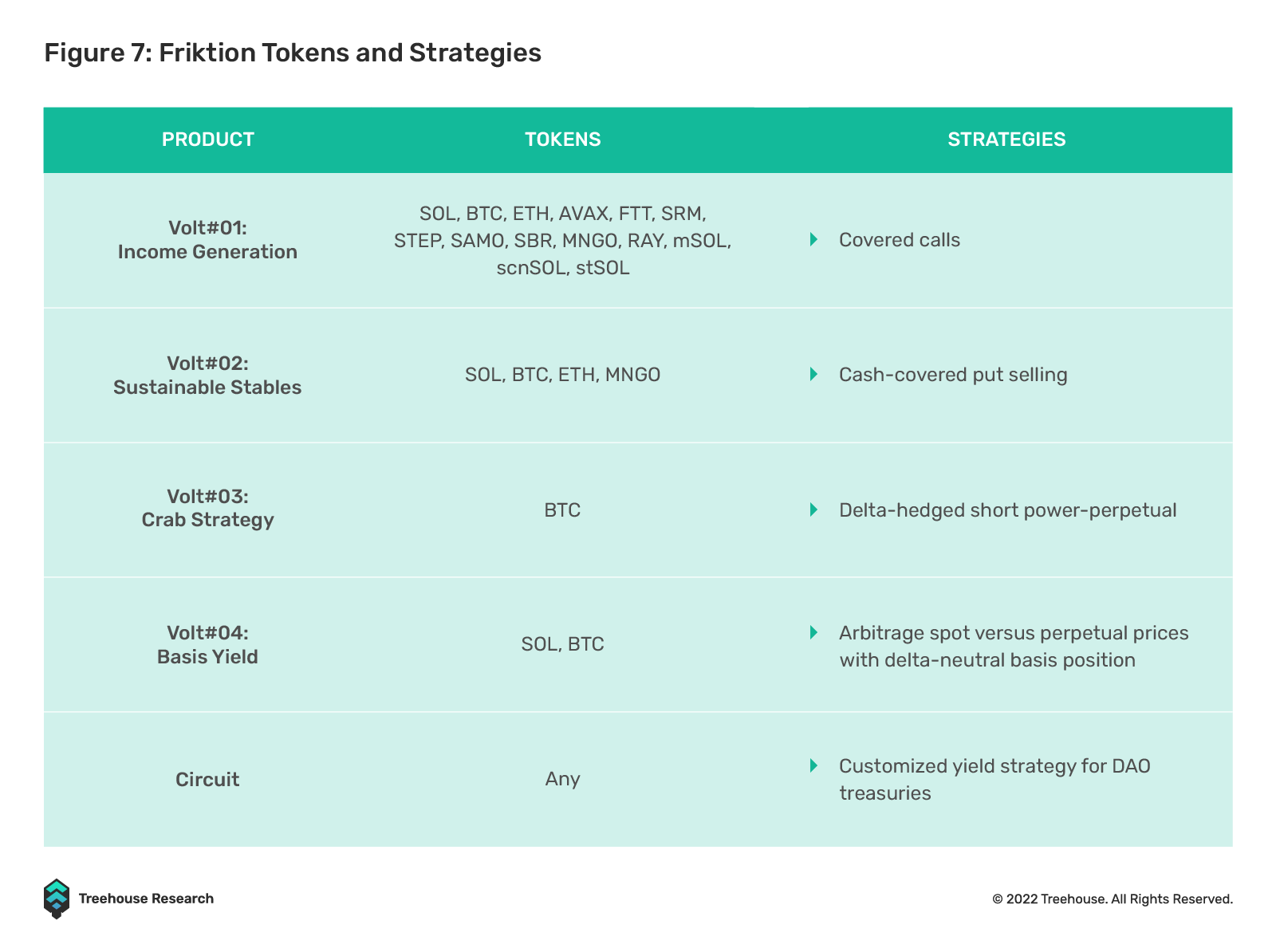

Friktion

Friktion is a DeFi portfolio management product protocol currently on the Solana network, which provides DAOs, individuals, and traditional institutions with risk-adjusted return generation strategies. Friktion’s native portfolio strategy, “Volts”, a play on the word “Vaults”, allows investors to access yield through derivatives arbitrage and volatility strategies. Launched on 17 December 2021, Friktion has traded $2.2 billion in volume and offers the largest options markets in DeFi – covering 35 assets. This is made possible through Gradual Dutch Auctions held on-chain via Channel RFQ, a Request-for-Quote protocol similar to Airswap or Hashflow on Ethereum. Friktion uses Inertia (Euro cash-settled options) and Entropy (exotic perpetual DEX) for their on-chain settlement. Recently, Friktion added support for cross-chain deposits for Ethereum and Avalanche users, allowing users to access Friktion Volts with Portals/Wormhole behind the scenes. In addition, Friktion has built an Institutional Analytics platform for all users to analyze the performance of each vault and their respective strategies.

Friktion raised $5.5M in December from firms including Jump Crypto and DeFiance Capital. Friktion has grown to become Solana’s largest structured products protocol, with a little more than $70M in TVL at the time of writing.

Friktion’s product offering extends beyond yield-generating vaults to a holistic portfolio management service. Friktion’s focus is on risk management products: such as the upcoming Volt#05, which will assist pool providers in hedging against impermanent loss while reaping the benefits of high yield opportunities. Friktion also offers delta-neutral strategies that are automatically delta-hedged through their systems in addition to directional strategies such as covered calls and put selling that carries delta.

Friktion recently completed a deep security audit together with Kudelski Security. Friktion plans to launch its governance token in the near future.

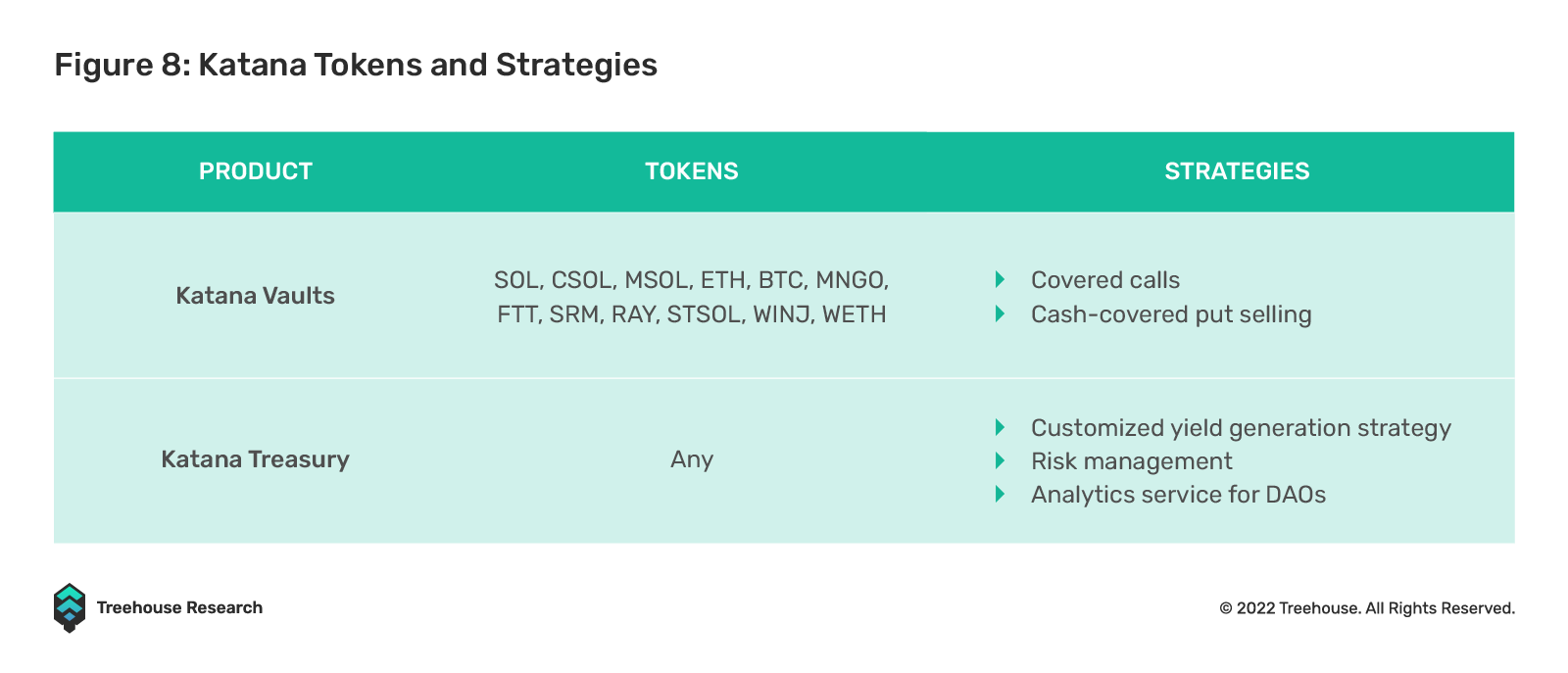

Katana

Having won the 2021 Solana IGNITION hackathon, Katana officially launched on 30 December 2021. It has managed to build 14 different vaults that support similar assets to Friktion. Katana vaults mints tokenized out-of-the-money options on Zeta and sells them to market makers through a competitive request-for-quote (RFQ) auction process. Katana’s TVL currently stands at $11M.

Recently, Katana announced a $5M seed round led by Framework. The raise will go towards helping the protocol scale up to become the de facto yield generation layer in DeFi.

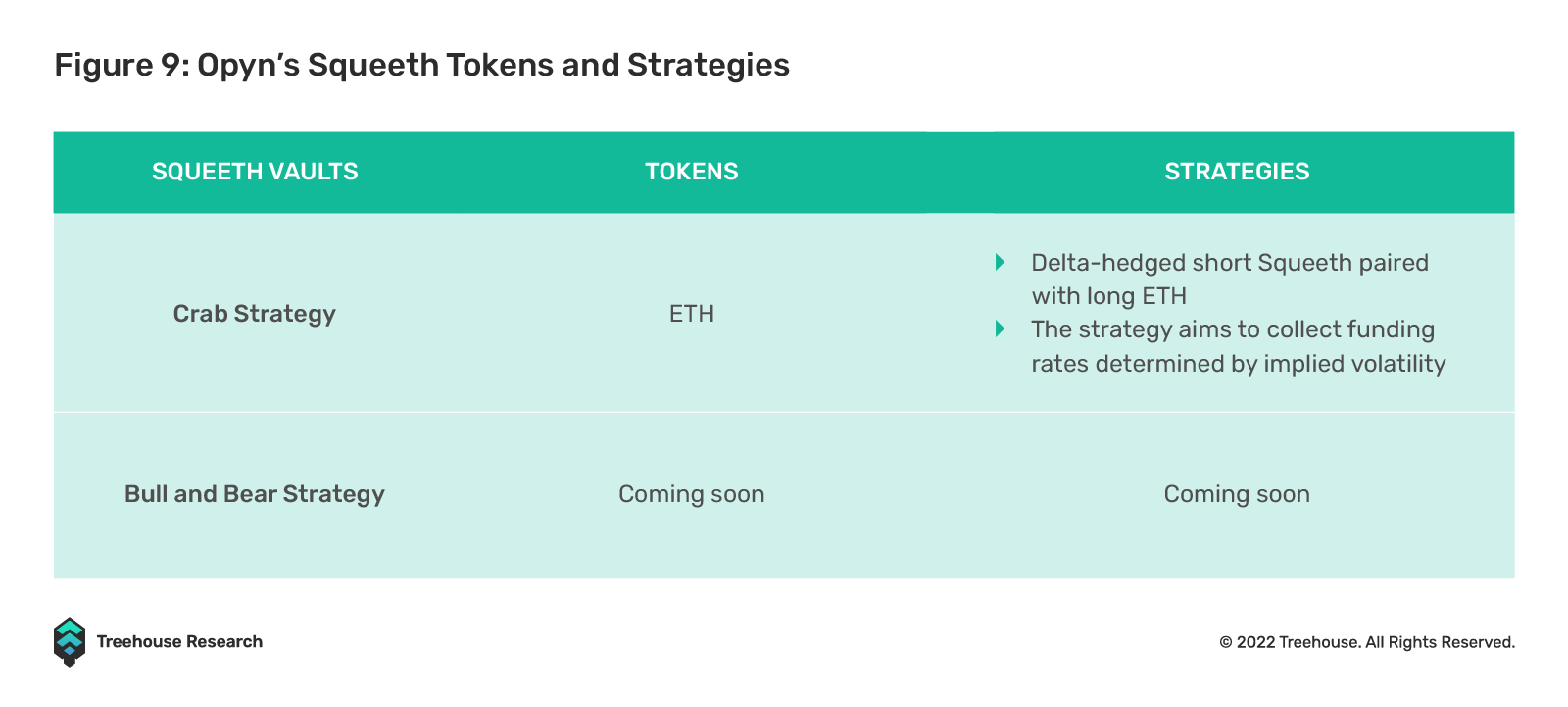

Squeeth by Opyn

Squeeth is a new financial derivative developed by the Research Team at Opyn. Squeeth is the first power perpetual that provides traders with perpetual access to ETH2. Squeeth functions similarly to a perpetual swap but with the embedded convexity and Gamma that an option has. In short, Squeeth makes options perpetual and can be an effective hedge for LPs, all ETH/USD options, and anything with a convex payoff.

Squeeth was released on the Opyn platform on 11 January 2021. Opyn is currently the largest structured product protocol offering options trading. Opyn’s TVL is $206M at the time of writing.

Opyn’s recently launched crab vaults function similarly to basis trading strategies. The vault’s strategy combines a short Squeeth position with a long ETH position to earn yields on funding rates while remaining approximately delta-neutral. The crab strategy is most effective in a sideways market with low volatility in either direction, allowing the investor to collect the funding rate or Theta, as it is known in options.

The crab strategy is similar to selling a continuous at-the-money straddle that regularly resets to be at-the-money. The vault rebalances positions daily to ensure that the amount of ETH is sufficient to cancel out the ETH exposure from the short Squeeth position, resulting in an approximate delta of 0 to the ETH price. Specifically, the vault expects the volatility between daily rebalances to be less than the implied volatility of ETH. Thus, if ETH moves less than the amount of implied volatility in a single day, the strategy is profitable. If the implied volatility is realized prior to the next rebalance in either direction, the strategy loses money.

Potential Issues Surrounding DOVs

While DOVs have the potential to revolutionize yield farming and liberalize structured products to the masses, they also have potential drawbacks. DOVs and systematic volatility selling strategies in the equity space of TradFi may resemble each other. The latter had witnessed several blowups to option sellers, particularly when volatility eventually mean-reverted aggressively higher after an extended period of low volatility from 2016 to 2018, during which an overcrowded market of participants ran the same volatility selling strategy. The DOVs space may potentially face the same issue as it grows bigger. Aside from that, capital inefficiency and front-running issues may be the next hurdles for DOVs to solve before they can attract more TVL.

Capital Inefficiency

Volatility selling has come a long way since the heydays of modern finance, but it has also seen its fair share of meltdowns. Fortunately, most decentralized option vaults today require full collateralization. An ETH-covered call vault, for example, would require investors to deposit the underlying ETH into the vault and write options with notional amounts lower than the deposited collateral. This requirement is intended to prevent naked selling and protect investors from losing more than they own as the strategy is not leveraged. However, increased security may come at a cost in the form of lower returns.

Compared to selling options directly, DOVs do not allow holders to unwind their position before expiry. This means that the investor must put on an offsetting trade if he wishes to take profit before expiry. For the retail investor who does not mind the delta exposure, the locked ETH is an opportunity cost as it could be generating yields elsewhere to stack returns.

Improvements are being made toward addressing the capital inefficiency issue of DOVs. Ribbon Finance, for example, is considering lowering the collateral required for option vaults. Furthermore, Ribbon Finance has already integrated with Lido Finance’s Liquid Staking feature, allowing vault depositors to earn both ETH staking rewards and premiums on writing calls simultaneously. In addition, StakeDAO’s option vaults introduce an extra step in the process by depositing underlying assets into another yield earning strategy before writing the options to be sold. @LilyWrites4 also mentions the use case for a clearinghouse-like structure to allow sellers of options to put up margin and get liquidated by the clearinghouse when the margin falls short. This may be a plausible solution to address the issue of capital inefficiency too. Ultimately, a fine balance must be struck between capital efficiency and investor protection.

Front-Running of DOVs

Option prices, like any other assets, is determined by demand and supply, and a key component to option pricing is implied volatility. Options are volatility products that express a certain distribution of returns for the underlying asset. In simple terms, if implied volatility is high, option prices will be higher, and vice versa.

Here is an issue that most DOVs currently face. What happens when more than $100M of options are sold across platforms at the same target delta region every week at the same expiry and time? The result is compressed implied volatility leading to suppressed yields that are further depressed by opportunistic front-runners.

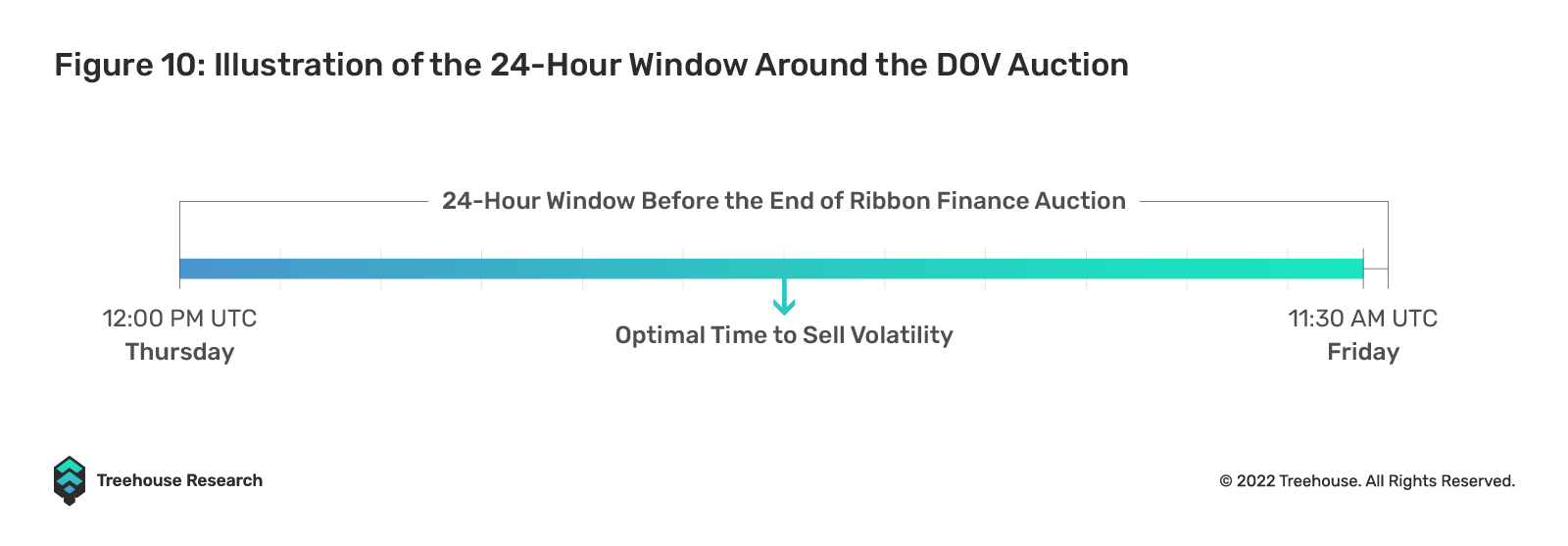

Currently, most DOVs auctions are held on Fridays as market makers can offload risk going into the weekend. Given that weekly options managed by Deribit expire on Friday as well, market makers can easily deal with the DOV flows. However, this makes it predictable for savvy volatility traders to front-run ahead of the DOVs auctions.

Every Friday, sometime between 2:00 AM and 11:00 AM UTC, the majority of the vaults will process the selling of options through auctions. The systematic selling of volatility will put pressure on options’ implied volatility during that window. Since auction information is made publicly available, volatility sellers across short-term tenors (usually 7-14 days expirations) can profit from short-selling volatility ahead of these auctions and close out their positions shortly after the auction event. This pushes down volatility, giving vault holders lower yields.

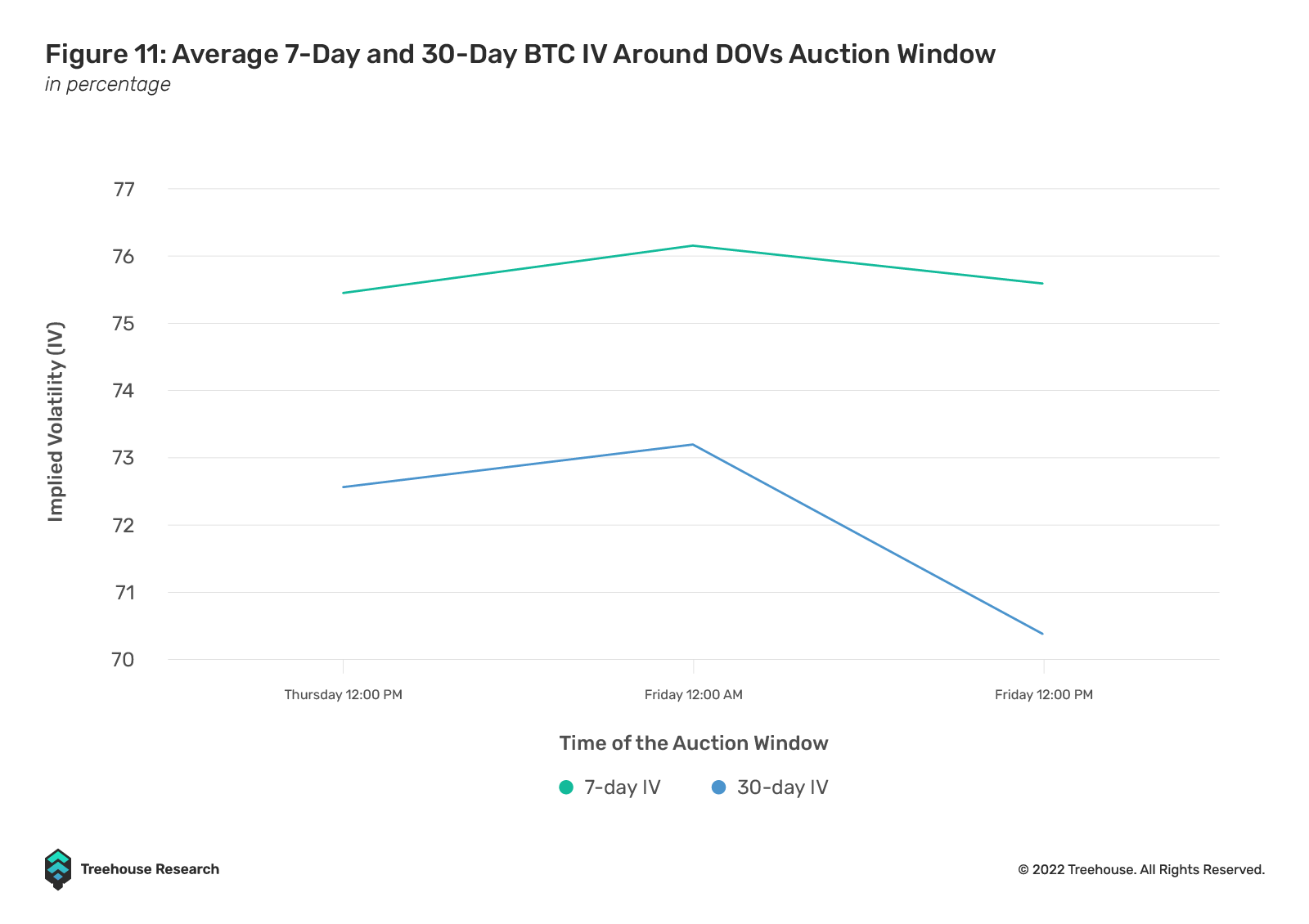

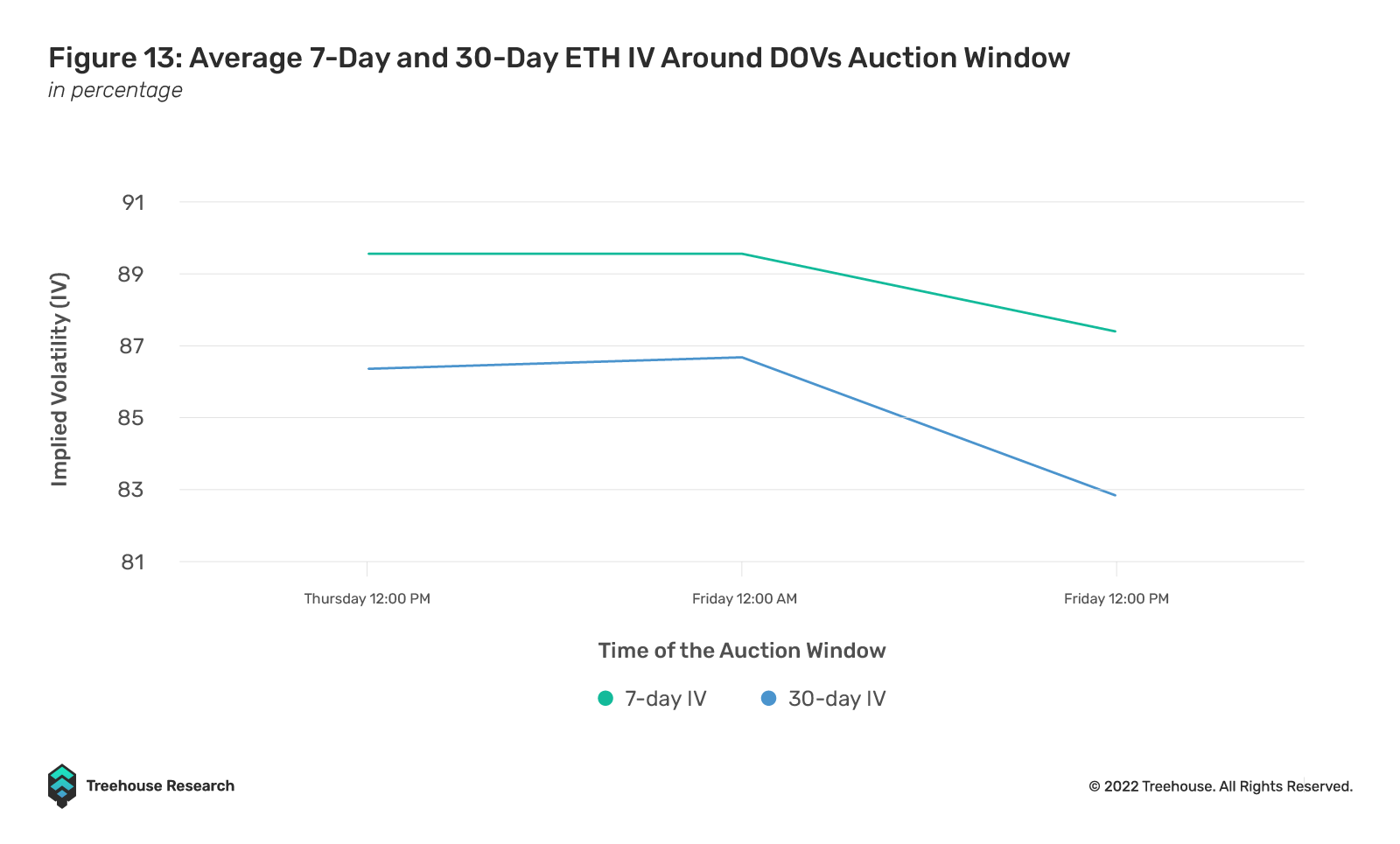

To illustrate this effect, we examine volatility movements within the 24-hour window where the DOVs auction takes place. We will use the auction timing for Ribbon Finance at 11:30 AM UTC. The dataset starts from 2 June 2021 to 2 June 2022. Figures 11 and 13 show the average 7-day and 30-day IV for BTC and ETH, respectively, during the window.

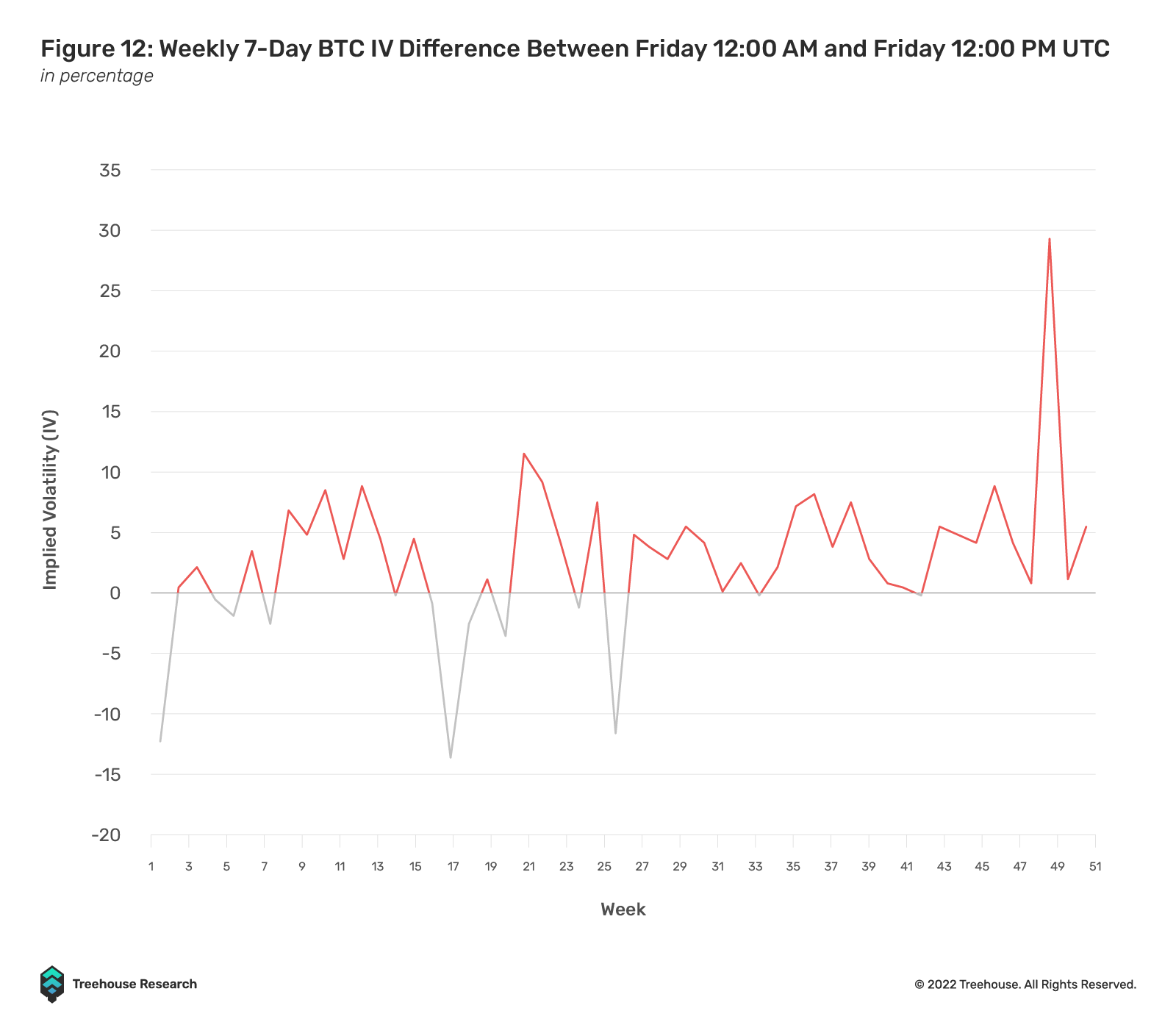

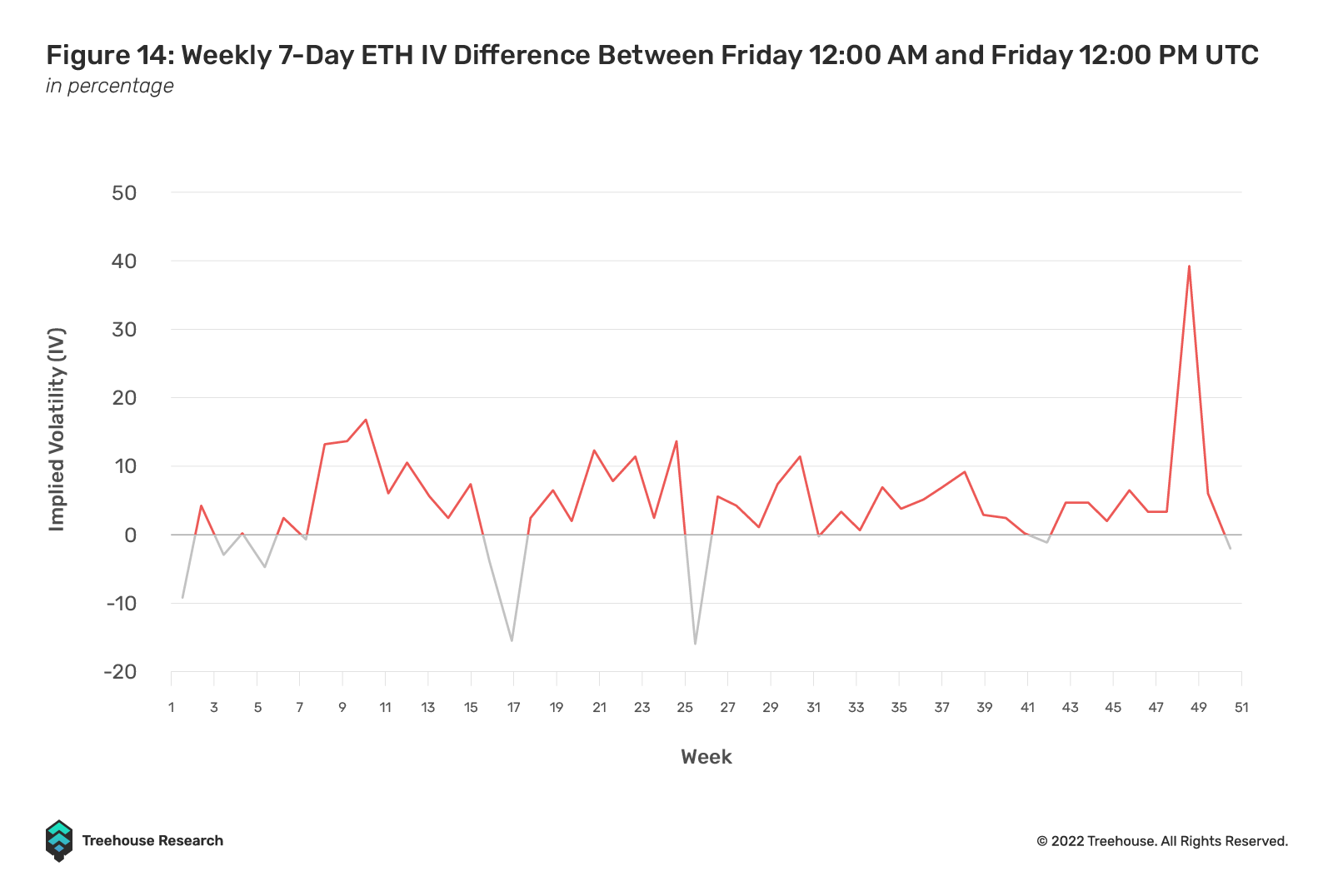

With reference to Figures 11 and 13, it can be seen that volatility falls 12 hours before the end of the auction. 7-day IV saw larger drops than 30-day IV for both BTC and ETH, which is obvious since options sold by the vaults are mostly weekly options. Figures 12 and 14 show the difference in 7-day IV for BTC and ETH, respectively, between Friday 12:00 AM and Friday 12:00 PM UTC. Anything above the zero line means that volatility fell excessively 12 hours before the auction. The dataset contains 52 weeks of data points starting from 2 June 2021. We can see that from the 25 to 27 week mark onwards, the effect of IV falling is much more persistent. This coincides with new DOV launches such as Katana and Thetanuts.

A recent study done by Friktion Labs concurred with the same findings as ours. Using an example of the 21 January 2022 expiry, implied volatilities on BTC dampened by more than 15 volatility points to 58% before the auctions and began recovering afterward. With implied volatilities at 58% on expiration, a 15 volatility point difference for a 10 delta call would shift yields from 21% to 52% APY. This highlights the huge impact on DOVs when many market participants look to sell their options at the same expiry at the same time every week.

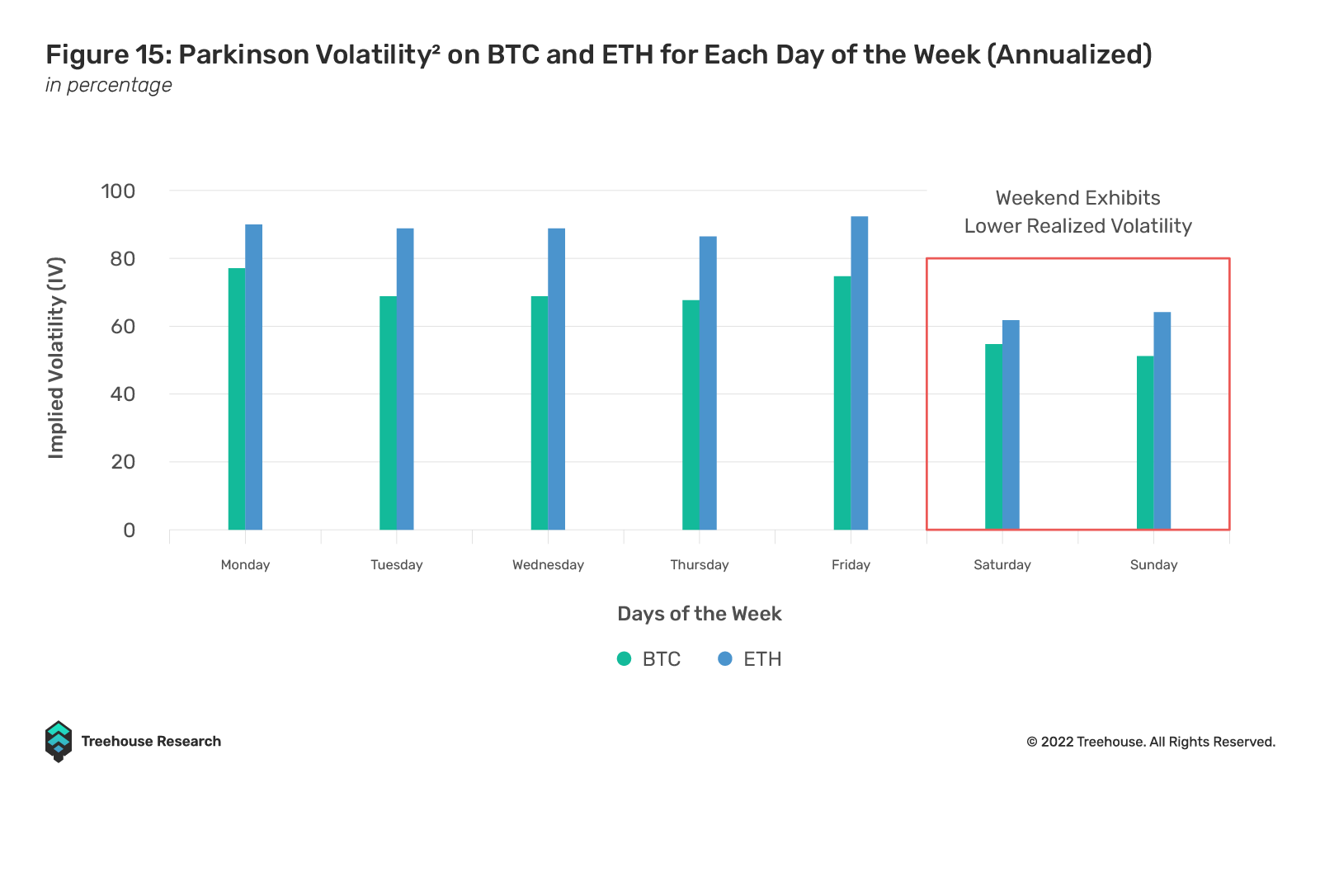

Furthermore, although weekends used to see more violent spot price moves, i.e., higher realized volatility, these kinks have been flattening out lately. Recent 1-year data shows that weekends exhibit lower realized volatility which translates to higher Theta risk for weekends (Figure 15 shows the Parkinson Volatility on BTC and ETH for each day of the week). According to @PelionCapital, market makers could fuel selling pressure ahead of DOVs to reduce inventory due to the high Theta risk on weekends. In addition, a possible reason could also be that traders are less willing to hold options over the weekend due to the low realized volatility, contributing to the low demand and selling pressure of options on Fridays. As a result, shorter-dated out-of-the-money options are drifting cheaper due to an imbalance of weekly sellers from DOVs alongside external market participants anticipating DOV flows and volatility traders preemptively selling before vault auctions.

Some protocols have tried to change the timing in the interest of vault depositors. For example, Friktion protocol adjusts execution timing throughout the day to capitalize on volatility market dynamics to enable higher risk-adjusted returns for users. Apart from that, Ribbon Finance was the first to decentralize and open up bids to non-market makers. However, current efforts have not meaningfully resolved the demand-supply imbalance as buyers cannot unwind their options pre-expiry, which means that they have to put up additional collateral on another centralized exchange to square off their positions, which brings us back to the point of capital inefficiency. Hence, there are few incentives for retail to participate in purchasing option flows from DOVs when they can do it directly on centralized exchanges.

Therefore, there needs to be more spreading and randomizing of DOV selling over weekdays instead of only on Fridays to avoid excessive front-running. Nevertheless, structural changes are required to the existing auction mechanism to prevent front-runners or, at the very least, mitigate the effects of concentrated volatility selling around a specific time window.

Overcrowding and Underperforming

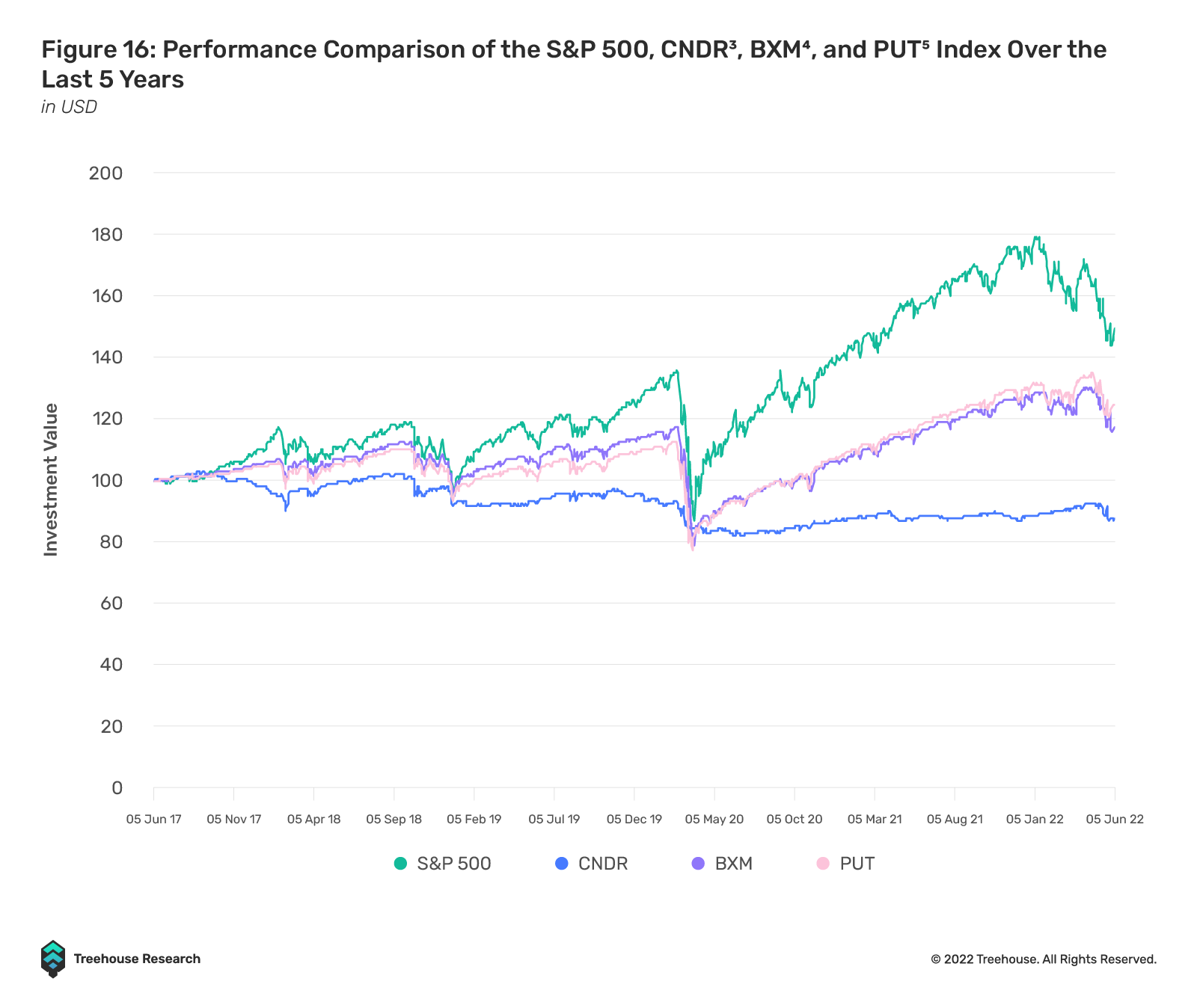

As more investors pile into option selling strategies, two things happen. First, option sellers outweigh buyers within a certain time interval around DOV auctions. As a result, the premium received on selling options becomes lower. This is evident in the TradFi space as index volatility harvesting strategies have consistently underperformed the simple buy-and-hold strategy for the last 5-years (Figure 16 shows the performance of CNDR3, BXM4, PUT5).

This is no exception for the DOV space as well. To begin, most DOVs participants are non-sophisticated retail who are price-insensitive and primarily seeking yield. Second, protocol designers are trying to design a “set-and-forget” approach to DOVs where vault holders can enjoy a hands-free approach to option selling. These dynamics may push yields further down as vault holders are indiscriminately and systematically selling volatility even when market conditions indicate poor risk-adjusted returns of volatility-selling. We saw this happen when crypto volatilities were meandering between 50% and 60% for the first quarter of 2022, which could partially be attributed to the rise in interest for DOVs protocols.

Back to the TradFi space, in light of this massive influx of option selling strategies causing the variance risk premium to fall, option sellers have to either increase their selling volume through leverage or choose strike prices that are much more aggressive to meet their return benchmarks. Doing so will accumulate negative Gamma6 and Vega7 risks, which invites self-reflexivity, as lower volatility feeds into lower volatility. When volatility unwinds, it will trigger a positive feedback loop, increasing volatility as short positions rush for the exits all at once. Hence, the option sellers will perform poorly if the markets move dramatically in either direction.

One example is the popular hedge fund Long-Term Capital Management8 (LTCM) selling longer-dated options totaling nearly $50 million in Vega exposure. Furthermore, LTCM was leveraged at 1:27. LTCM’s short equity index volatility strategy lost more than $1.3 billion in total during the Asian Financial Crisis, causing the fund to incur massive losses which at that time posed a potential systemic threat to the entire financial industry.

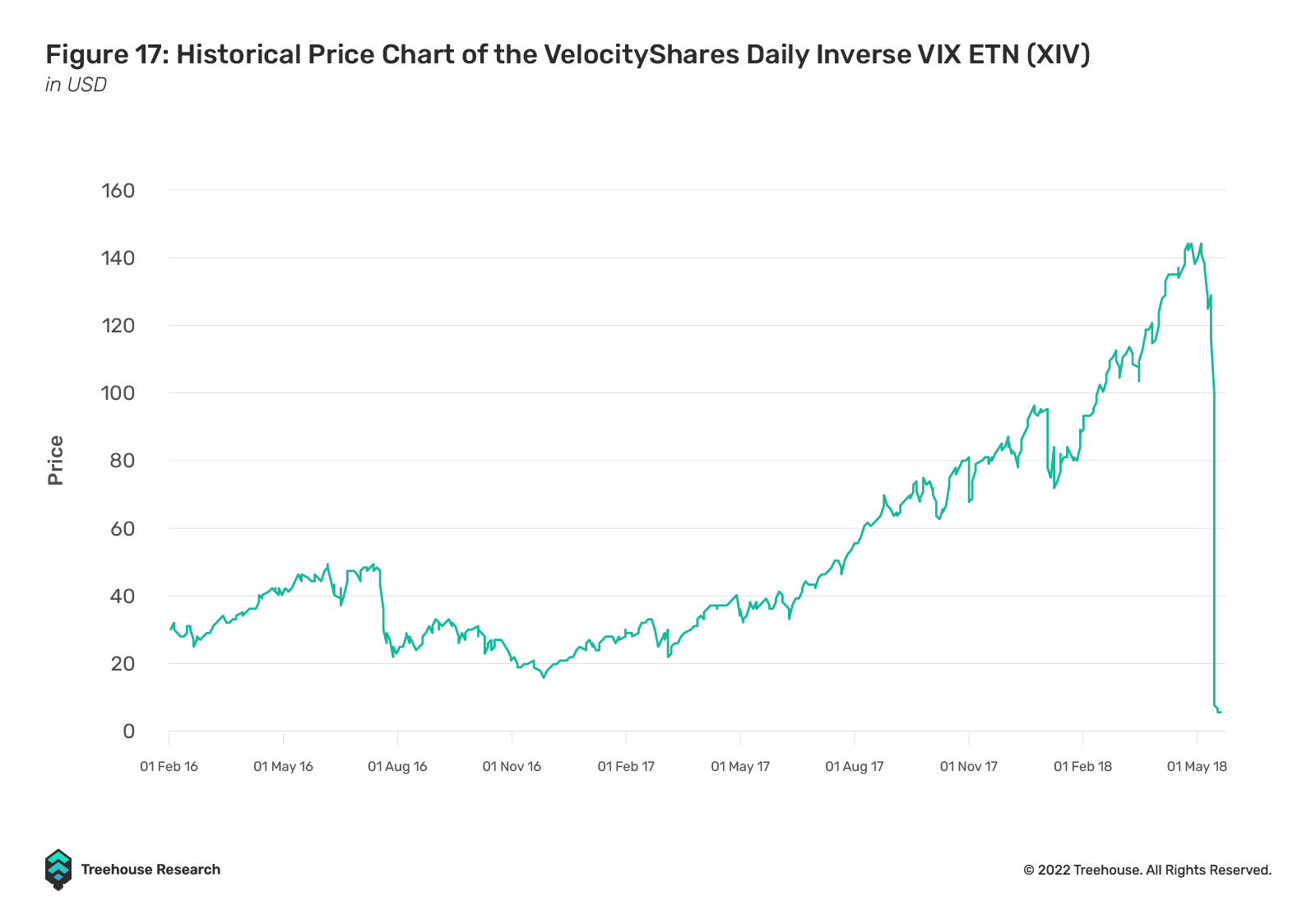

Another recent example is the XIV implosion, dubbed “Volmaggedon,” which occurred in early 2018. XIV was a leveraged inverse exchange-traded note that tracked the VIX, an S&P 500 volatility index. Due to concentrated selling of volatility, VIX was massively suppressed for a prolonged period. However, on 5 February 2018, the S&P 500 fell by 5.4%, causing VIX to skyrocket by 117%. In theory, an inverse product tracking VIX would fall to zero if VIX doubles. XIV lost over $2 billion in net asset value in a single day, causing massive losses to unwitting retail investors as the ETN suspended trading due to a force majeure clause following the debacle (Figure 17). Selling volatility is like picking up pennies in front of a steamroller. The strategy may perform well for a while, but all it takes is one bad trade to derail it. Researchers from Ledger Prime have done an exceptional study on the historical performance of DOVs, showing that infrequent major shocks can erode the strategy’s profitability.

Volatility selling can also have second-order effects on the spot market as a whole. The crypto options market currently accounts for less than 1% of the total crypto market. If this proportion increases, the market structure may change, giving the options market more influence. As options trading becomes more popular in crypto, dealers who make those markets will hedge more frequently as they take on more Gamma risk, long or short. The March COVID-19-induced market rout was evidence of the “tail wagging the dog”. As traditional markets began to crack in March 2020, the continued selling was exacerbated by dealer hedging in a self-reinforcing manner due to negative Gamma exposure. There is no doubt that COVID-19 was an exogenous event, but the endogenous effects of micro-market structure should be something to be wary of.

With such dynamics in play, investors should be cognizant of the risks they take when investing with option vaults. At least for covered calls, there is a limit on the overall collateral as it will still increase in USD value if the option gets exercised in-the-money. Selling puts is a dangerous endeavor that will experience drawdowns in value should the options expire in-the-money.

Future of DOVs

Despite the cautionary tales mentioned in the preceding section, we believe that DOVs will revolutionize the DeFi landscape by providing organic yields and democratizing options to the masses. Here is our opinion on how DOV should progress from here.

Innovations, Innovations, and More Innovations

Thus far, the DOV space has seen phenomenal innovation. The fact that DOVs are still in their infancy is perhaps the most exciting aspect. DOVs have barely scratched the surface of options strategies by currently offering only covered calls and puts. Because options are so versatile, it allows investors to express specific views. Structures with enticing payoffs such as butterflies and spreads could be made available for investors in the future. DOVs can also look into physical settlement for vault holders, so they do not have to buy or sell the underlying on another exchange if the options are exercised.

Protocol developers can consider improving their execution methods in addition to expanding their offerings in the space. Instead of focusing on a single day, execution can occur every day of the week. Ribbon Finance has recently announced its planned V3 upgrade allowing auction execution to be done at random times and sizes. As for Thetanuts, its Stronghold addresses the above by selling across the entire term structure and picking spots where other option vaults are not selling. For Friktion, it utilizes a flexible auction timing, especially when IVs have compressed meaningfully below realized volatility.

Paradigm, an institutional crypto liquidity network, has also recently partnered with several DOV protocols to improve on-demand liquidity for traders and investors to tailor their options exposure to expiry, risk profile, and settlement preferences. The collaboration will improve liquidity significantly throughout the DOV auction process, bringing more benefits to all parties involved.

Lastly, DOVs can look toward tokenizing vault positions to address the issue of capital inefficiency. For example, Thetanuts will soon convert its vaults into tokenized positions, allowing users to swap in and out ahead of time. The token value will reflect the option price of the vault.

Self-Regulation and Retail Education

In addition to the usual smart-contract and protocol risks, there are risks that may be unfamiliar to investors who are venturing into options for the first time. There is plenty of education available, such as Deribit and GenesisVolatility, which publish useful options content whether you are a beginner or an expert. Recently, Katana announced that they will launch Katana Dojo, an educational initiative to equip investors with essential knowledge of options.

Instead of solely focusing on yields, investors should consider the strikes, tenors, and whether they are willing to be exercised if the option expires in-the-money. Investors must also be aware of these vaults’ management and performance fees. Instead of simply selling systematically, investors should be made aware of the current volatility environment. In a risk-off environment, for example, where realized volatility can outpace implied volatility, investors should be cautious before engaging in volatility-selling strategies. Investors are also strongly advised to take a hybrid approach to sell volatility. If they believe they are inadequately compensated for taking on that risk, they can choose to sit out for that week. Once again, Ribbon Finance V3 will feature a “pause” function for investors to sit out instead of having to withdraw their funds from the vaults to improve user experience. Education and self-regulation are key to protecting investors.

Conclusion

While options trading is reserved for the more sophisticated investors in traditional finance, DOVs are available to all types of investors. It represents an important step toward democratizing finance for the masses. DOVs also play a significant role in increasing demand for organic yield, thereby addressing the issue of the unsustainable and circular yields that DeFi currently faces. DOVs have a promising future.

Appendix

Covered Call Strategy

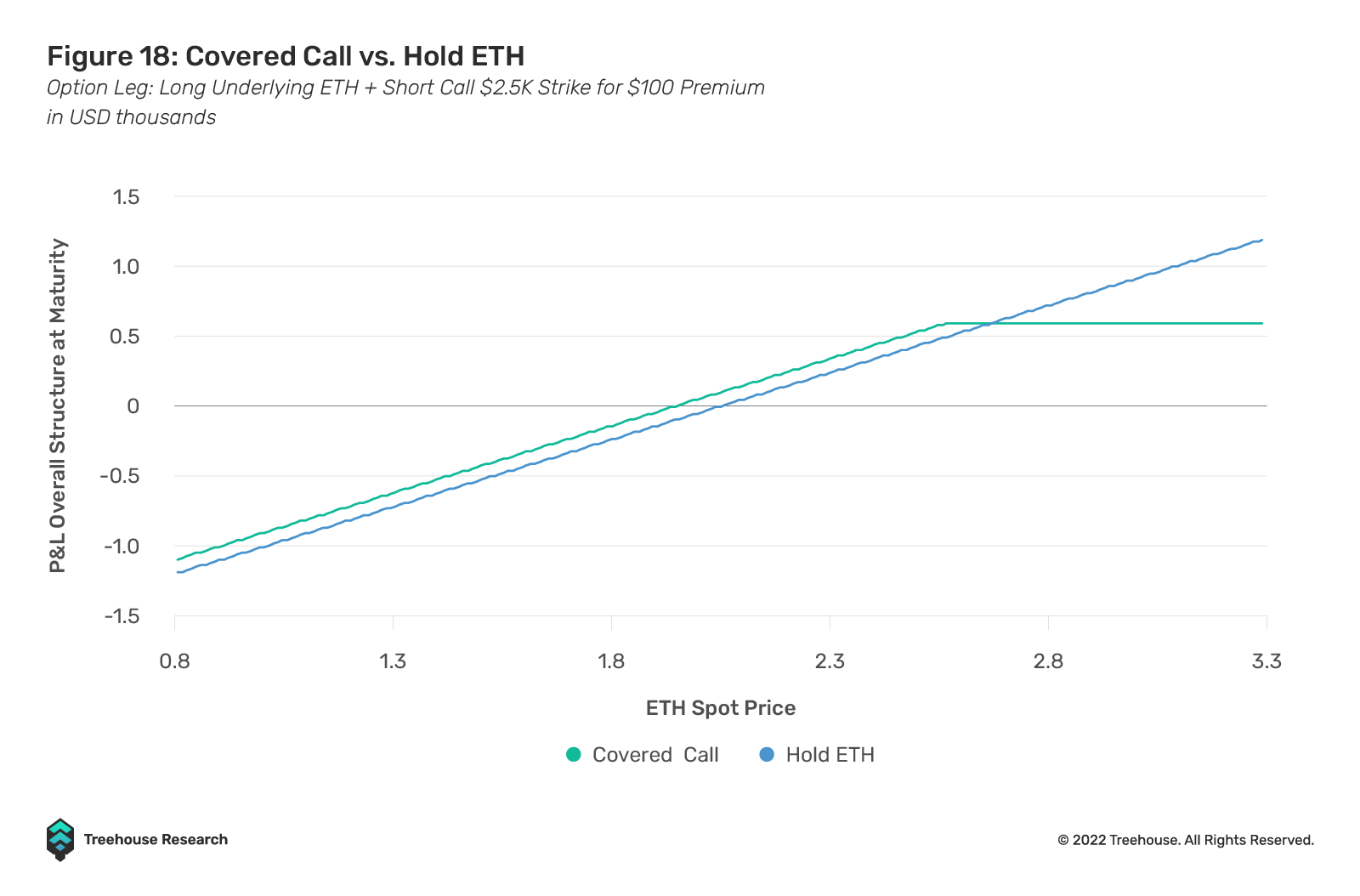

The chart below (Figure 18) depicts a covered call strategy on ETH. Assuming the underlying is trading at $2K, the trader writes a $2.5K call and receives $100 in premium. As we can see from the blue line representing the covered call payoff, the trader’s profit is capped after the $2.5K price levels for ETH. This is because the delta offsets one another from both the underlying and short call positions. By giving up that upside return, the trader receives $100 in premiums for selling the options. This is a good strategy during sideways markets or if implied volatility is high enough to warrant the trader to sell options to trade the excess volatility premium.

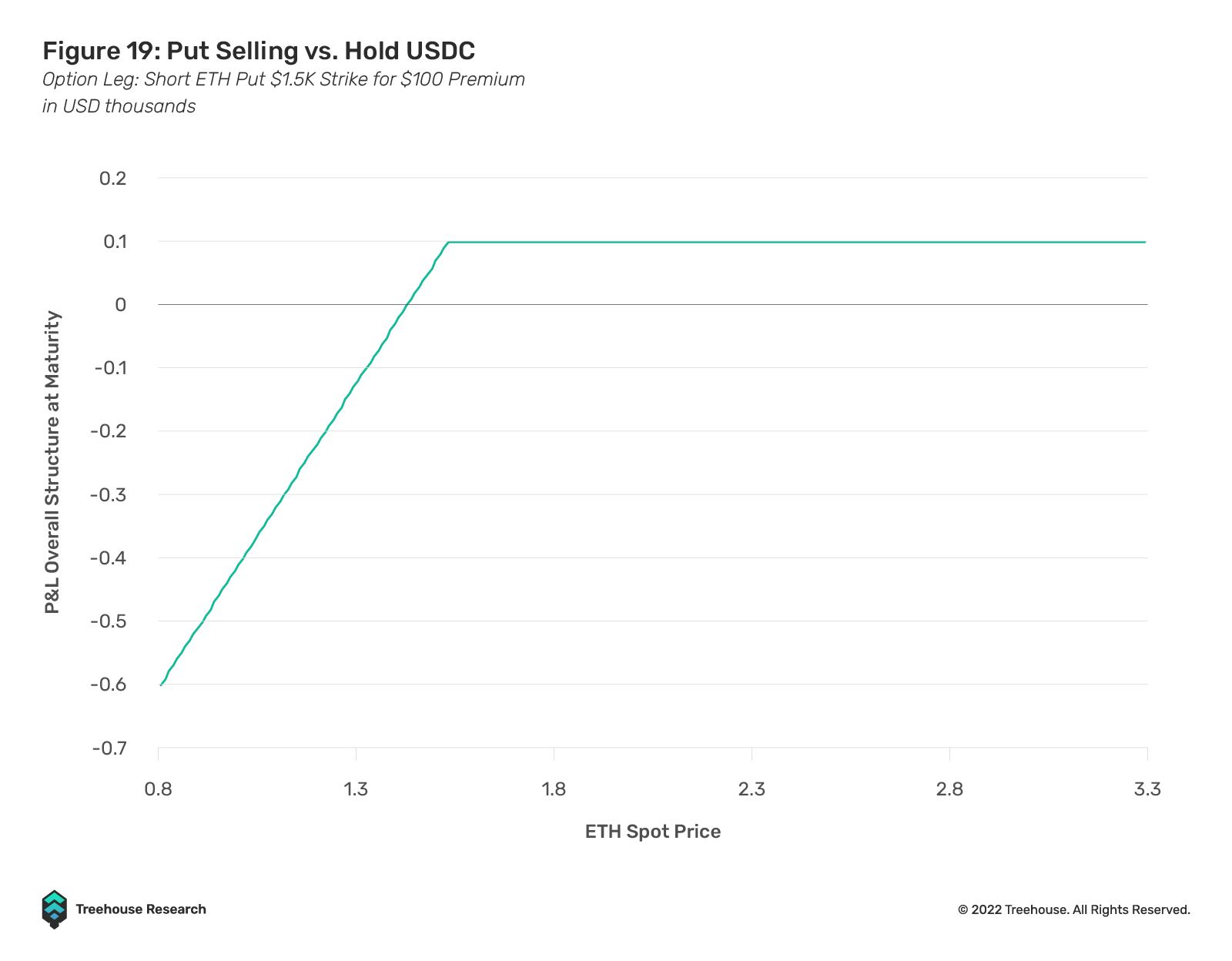

Put Selling Strategy

The chart below (Figure 19) depicts a put selling strategy on ETH. Assuming the underlying is trading at $2K, the trader writes a $1.5K put and receives $100 in premium. As we can see from the blue line representing the put selling payoff, the trader’s profit is capped at the premium they received, while the overall risk is still to the downside. Notice how both covered call and put selling strategies have the same payoff structure. This is because both strategies are inherently net long-delta. On the other hand, if the trader were to hold onto their USDC, should ETH fall precipitously to extremely low levels e.g., $1K, a separate trader can buy in at that price, compared to the trader who got exercised at the $1.5K strike price. Put selling is a valuable equity replacement strategy for long-term investors seeking to accumulate assets at prices they are willing to buy in. For speculators, put selling can be beneficial after a steep drawdown in prices causes volatility to rise while increasing the chance for a relief bounceback.

Footnote

1 Source: Token Terminal

2 Parkinson volatility is a volatility measure that uses the stock’s high and low price of the day.

3 CNDR refers to S&P 500 Condor Index.

4 BXM refers to S&P 500 BuyWrite Index.

5 PUT refers to S&P 500 PutWrite Index.

6 Gamma refers to the rate of change of an option price per 1-point move in the option’s delta.

7 Vega refers to the rate of change of an option price per 1-point move in the option’s implied volatility.

8 On top of equity volatility selling, LTCM engaged in other strategies such as merger arbitrage and bond arbitrage which also led to the fund’s demise during the Asian Financial Crisis and the Russian Rubble blowup.

Disclaimer

This publication is provided for informational and entertainment purposes only. Nothing contained in this publication constitutes financial advice, trading advice, or any other advice, nor does it constitute an offer to buy or sell securities or any other assets or participate in any particular trading strategy. This publication does not take into account your personal investment objectives, financial situation, or needs. Treehouse does not warrant that the information provided in this publication is up-to-date or accurate.

Hyperion by Treehouse reimagines workflows for digital asset traders and investors looking for actionable market and portfolio data. Contact us if you are interested! Otherwise, check out Treehouse Academy, Insights, and Treehouse Daily for in-depth research.