What Are Perps?

Introduced by BitMEX in 2016, perpetual futures contracts, or perps, are derivative futures contracts that allow users to buy or sell the value of an underlying asset. Perps are similar to futures contracts, as the name suggests. However, the two have a few differences, as illustrated in the table below.

| Futures | |

| No expiry date | Contracts have an expiry date tied to them |

| Specifically for cryptocurrencies | Present across multiple asset types (Stocks, crypto, etc.) |

| Funding rate involved | No funding rate |

The first difference between perps and futures is that perps can be held indefinitely while futures contracts have a settlement date; the specific contract can no longer be traded after the specified date. Another main difference is that perps mainly exist for cryptocurrencies, while futures contracts are present across multiple asset classes, such as equities and crypto. Lastly, perps have a funding rate attached to them while futures do not.

So What Exactly Are Funding Rates?

Funding rates are periodic payments exchanged between long perp traders and short perp traders. This concept is designed to peg the perp price to spot price, as perps do not have traditional futures’ roll-down/pull-to-par feature. This feature serves to align futures and spot prices at expiry. If the perp funding rate is positive, long perp traders pay short perp traders; vice versa if the funding rate is negative.

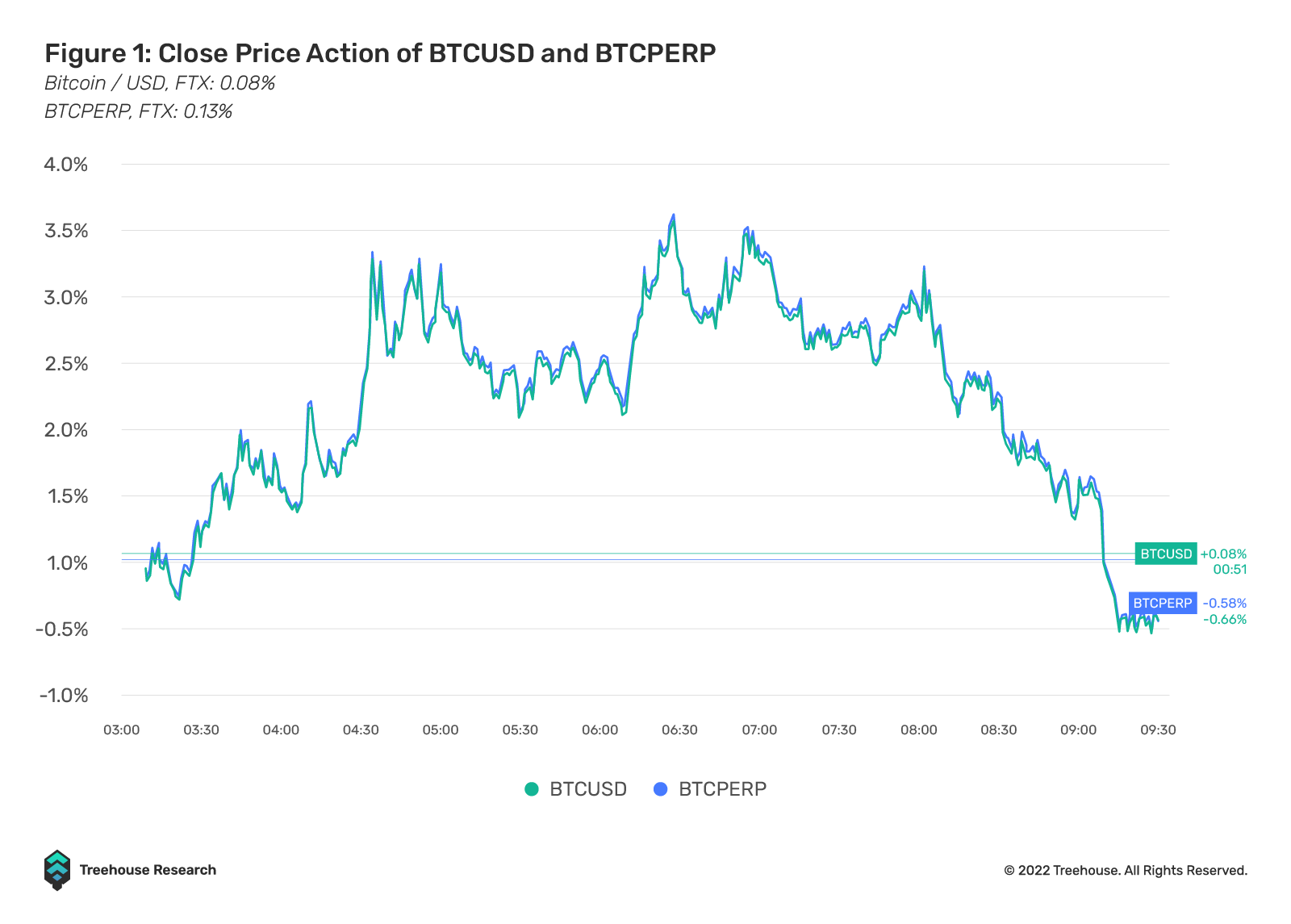

We can see the workings of this mechanism in the figure below, where the BTC perp price is trading at close to the same price as spot BTC.

Funding cycles last 1 to 8 hours depending on the CEX. For example, both BitMEX and Binance use 8-hour funding cycles for their funding rates calculation, while FTX recalculates hourly. This means that, after every funding cycle, the funding rate can change and even flip from positive to negative and vice versa, depending on the price of the perp and its underlying asset.

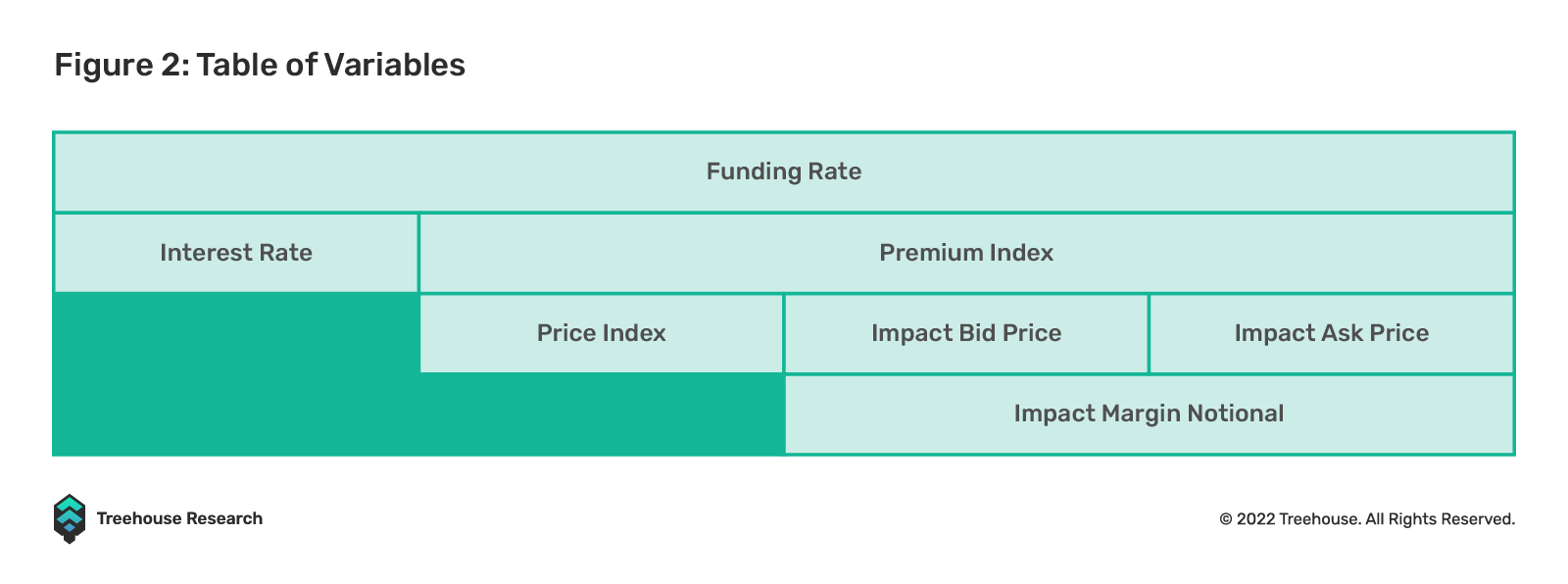

The funding rate calculation comprises two components: borrowing interest rate and premium. The premium is the primary reason the perpetual contract price converges with the underlying asset price.

Interest Rate

Binance, for example, uses a flat interest rate. This is based on the assumption that holding fiat would return higher interest than the BTC equivalent. The difference is stipulated to be 0.01% every 8 hours, meaning 0.03% a day by default, since funding occurs every 8 hours. However, this may change according to market conditions.

Premium Index

If there is a significant difference in price between the perpetual contract and the underlying asset’s price, a premium index is used to ensure the prices between the two markets converge. The premium index is calculated separately for every contract, using the price index, impact bid price, and impact ask price.

Price Index

The price index is a basket of prices from major spot exchanges weighted by their relative trade volume.

Impact Bid Price and Impact Ask Price

The impact bid and ask prices refer to the average fill price to execute the impact margin notional on the bid and ask prices, respectively.

Impact Margin Notional

The impact margin notional (IMN) is dependent on the initial margin rate at the maximum leverage level for a particular contract (IMN = 200 USDT ÷ Initial margin rate at maximum leverage level). For example, if the maximum leverage for a BTCUSDT perpetual contract is 125x and its initial margin rate is 0.8%, the IMN is 25,000 USDT (200 USDT ÷ 0.8%). The system will take an IMN of 25,000 USDT every minute in the order book to measure the average impact of bid and ask prices.

Mythbusted

While perpetual futures have become a relatively common tool for investors, there are still a couple of misconceptions about how they actually work. These misconceptions can be broken down into risk and funding rates.

Risk

Due to the close correlation between perpetual contracts and the underlying asset, some might think that perpetual contracts share the same risks as the underlying asset. However, this is not true. For one, perpetual contracts have a funding rate associated with them, which will impact one’s overall profit and loss (P&L) at the end of the trade. Furthermore, perpetual contracts allow one to use leverage, which can be extremely risky due to the high chance of liquidation.

While various exchanges allow users to use exorbitant amounts of leverage, such as Binance with 125x, it is important to note that a small change in the contract’s price can lead to one’s account getting liquidated. For example, taking on a 100x leveraged position while going long on a perpetual contract would mean that the contract’s price would only have to fall 1% for one’s position to be liquidated. As such, it is important to note that trading perpetual contracts can be very risky.

Funding Rate

The next common misconception is that the funding rate is a fee paid to exchanges. However, this is not the case, as the funding rate is simply a fee between market participants. Exchanges do not take a cut of the funding fees paid. It is important to understand the mechanism behind the funding rate and how it is impacted by market conditions, as funding rates impact one’s P&L at the end of the trade.

Use Cases of Perps

Why Perps vs. Spot

Pros

- Ability to take significantly higher leverage

Buying spot assets means you are effectively longing with 1x leverage. However, you could leverage up to the maximum permitted multiples depending on the CEX and take on more exposure when using perps.

- No custody requirements

When you trade perps, the underlying asset is never settled physically, enabling you to gain exposure to its price movements without holding the asset. This eliminates the need for custody solutions to store and secure crypto assets.

Cons

- Funding Rates

Under some circumstances, a trade can be implemented with perps such that the position makes money on underlying movement as well as paid funding. However, the funding rate mechanism does not favor the consensus trade direction. For example, if the perp composition comprises 70% longs and 30% shorts, investors who are long the perp will most likely pay a funding rate to shorts. Therefore, opportunistic switching between spot and perp is needed to maximize funding benefits.

- Liquidation

Depending on the maintenance margin requirement, a perp position can be liquidated before the theoretical wipe-out movement happens. For example, a 10x leveraged perp contract on a CEX might get liquidated before a 10% spot move as the CEX protects itself from a margin shortfall and liquidates risky margin positions earlier.

Why Perps vs. Other Derivatives

Pros

- Deeper Liquidity Compared to DeFi Options

The daily trading volume of perps is significantly higher than that of the DeFi options market. The linear, delta-one nature of perpetual contracts also makes it more convenient for hedging/speculation purposes, attracting more market participants than the options market.

- Price of Perps is More In Line with Spot Compared to Futures

Unlike traditional futures contracts, where the price can deviate from the spot price (also known as the basis), the price of perps usually stays closely in line with the spot price due to the funding rate mechanism.

Cons

- Uncapped Downside/Liquidation

Compared to options trading where there is a capped downside (i.e., losing the “premium” which was paid upfront should you choose not to exercise your right in the future), a perp trader could incur significant losses if the market price were to gap up/down. However, max risk can be limited before a trade is put on by disabling cross-margin and using a segregated account – in such a case, a position’s max loss will be the segregated margin amount.

- Funding Rates

During periods of extreme market volatility or concentrated bets on one side of the market, the funding rate can be extremely high. For example, during the LUNC (then LUNA) selloff, the perp funding rate shot up to a whopping 2% per hour, or 17,520% per annum (that trade would still have made money because LUNC inflated at an even higher rate).

Where Can Users Trade Perps?

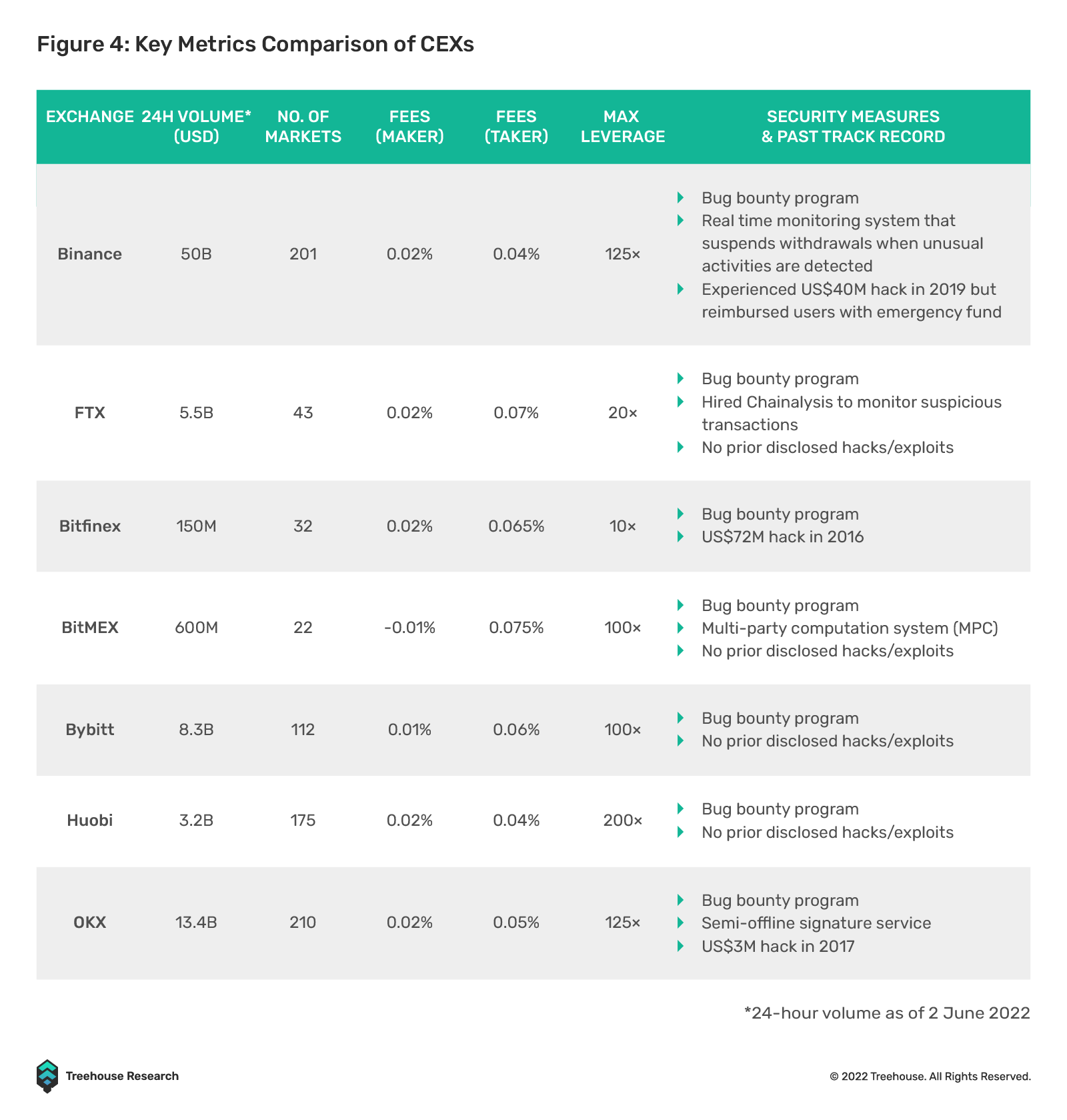

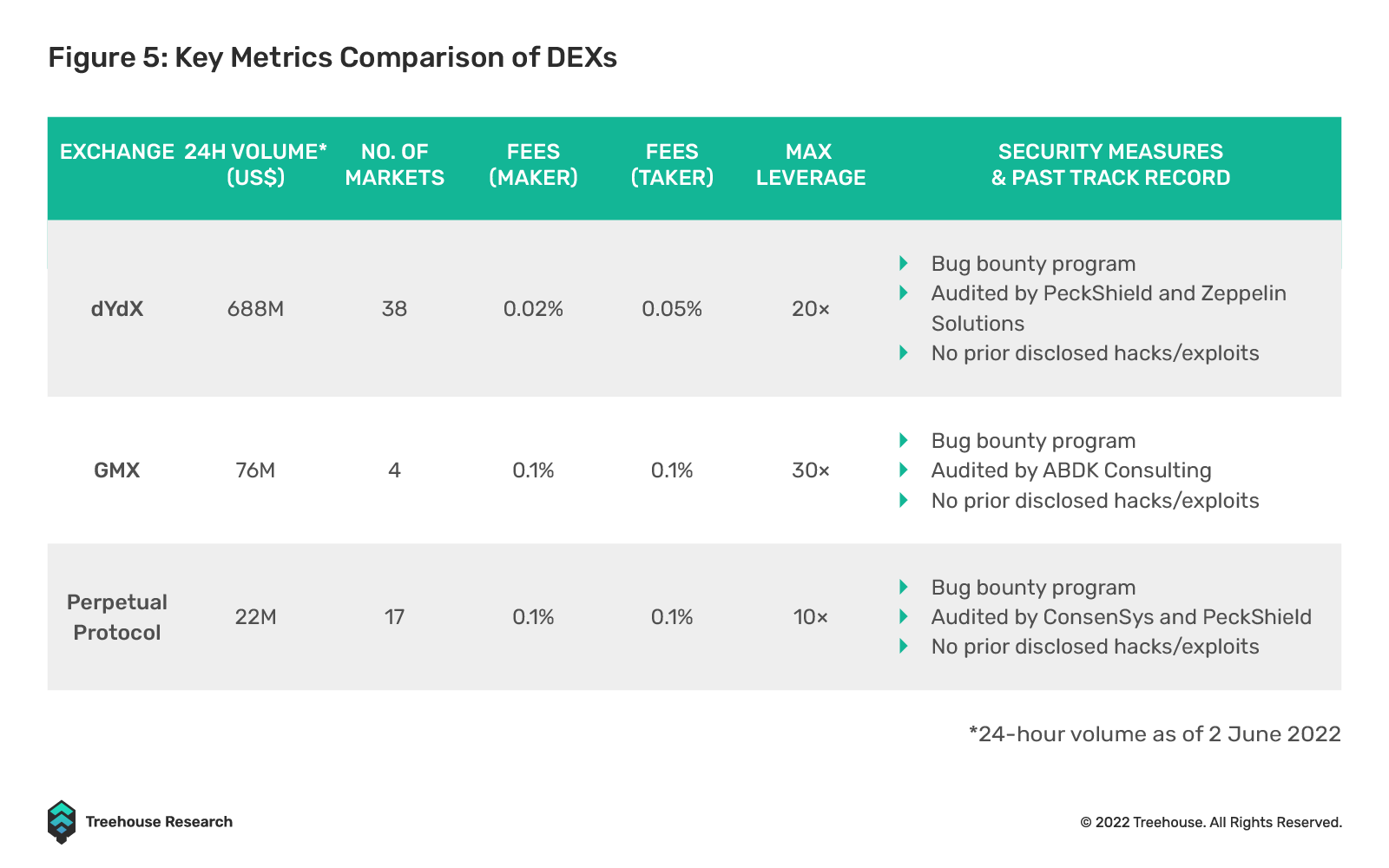

Users have a plethora of choices to choose from because most centralized exchanges (CEXs) offer perpetual futures trading. Some popular CEXs include Binance, FTX, Bybit, and Bitfinex. For users who wish to use decentralized exchanges, the more established decentralized exchanges offering perpetual futures trading include GMX, dYdX and Perpetual Protocol. We will compare some key metrics across the different exchanges so that a user can better understand which exchange is best for their needs. These key metrics are as follows:

The comparison across all the popular CEXs are as follows:

We show the same comparison across all the popular decentralized exchanges below:

Ultimately, the choice of exchange depends on the user’s personal preferences and trading styles. For instance, if a user prefers a CEX with diverse token assets, they may favor Binance or Huobi. If a user prefers a DEX with low fees, they may go with dYdX since it offers the lowest fees among the 3 DEXs above.

How Users Can Trade Perps on DEXs vs. CEXs

There are primarily two types of perpetual contract exchanges: those using the order book model, and those using the automated market maker (AMM) model.

Order Book-Based (Peer-To-Peer)

Most, if not all, CEXs belong to this category. Every trader can place an order on a centralized order book, and transactions will occur between traders when there are matching buy and sell orders.

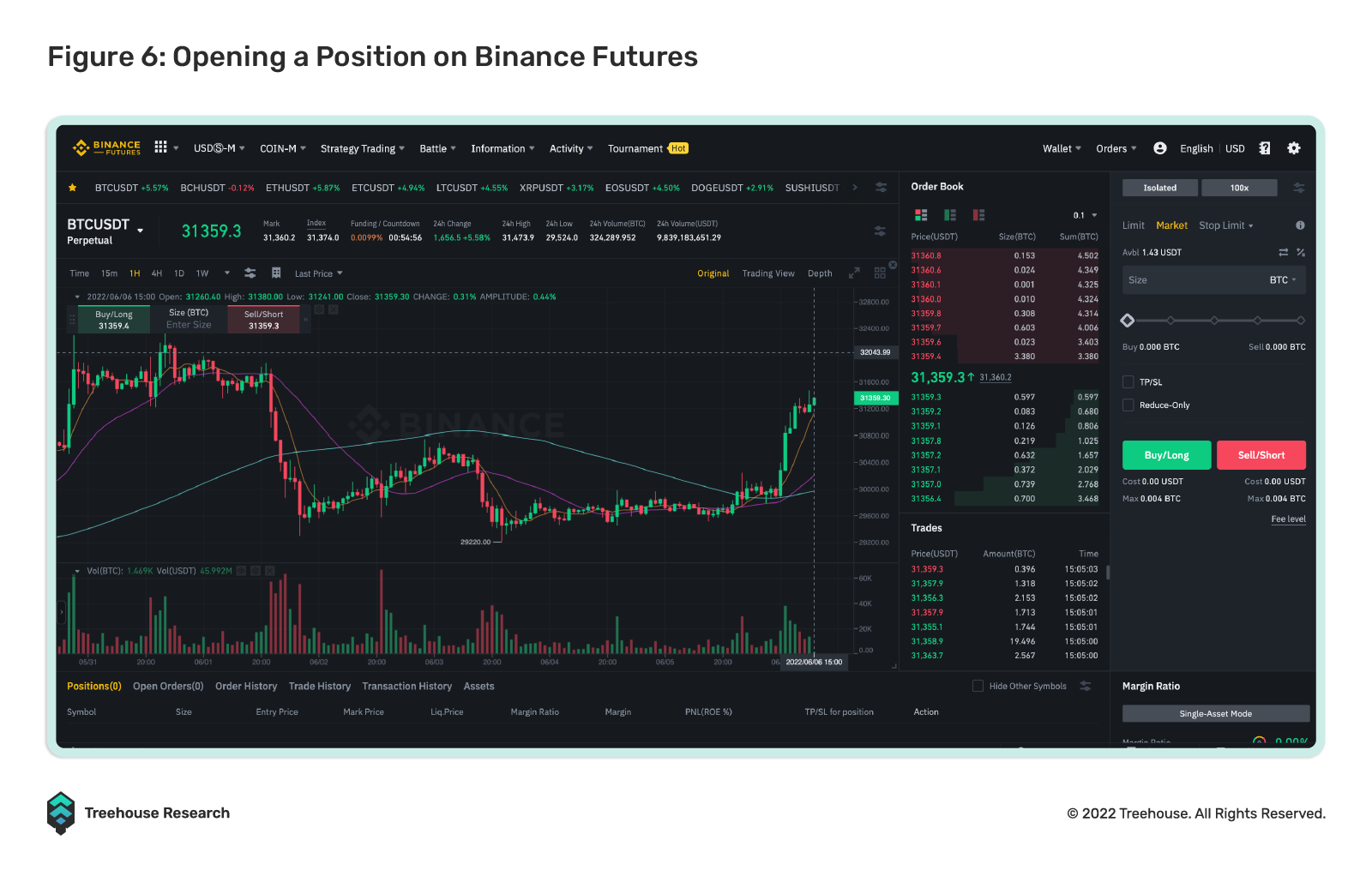

Opening a Position on an Order Book-Based Exchange

If a user thinks that the BTC price will go up, this is how they can open a perp position:

- Deposit margins into a perpetual futures trading account as collateral

- Choose the leverage ratio

- Key in the price you are willing to buy/sell as well as the position size

- Click Buy/Long or Sell/Short depending on the position you wish to open

- Your order will be filled if an order on the other side of the trade matches yours.

Let’s say a trader, Alice, thinks the current BTC price of 31K is too low and expects it to go to 34K. She then deposits 5K USDT into her Binance Futures trading account as collateral. Next, she decides she wants to go long on 2 BTC with 2K USDT as her margin, then the leverage she has to employ is 31x. (Leverage = Notional size of position ÷ margin). Since Binance’s maker fee is 0.02%, Alice must pay $0.40 as the transaction fee.

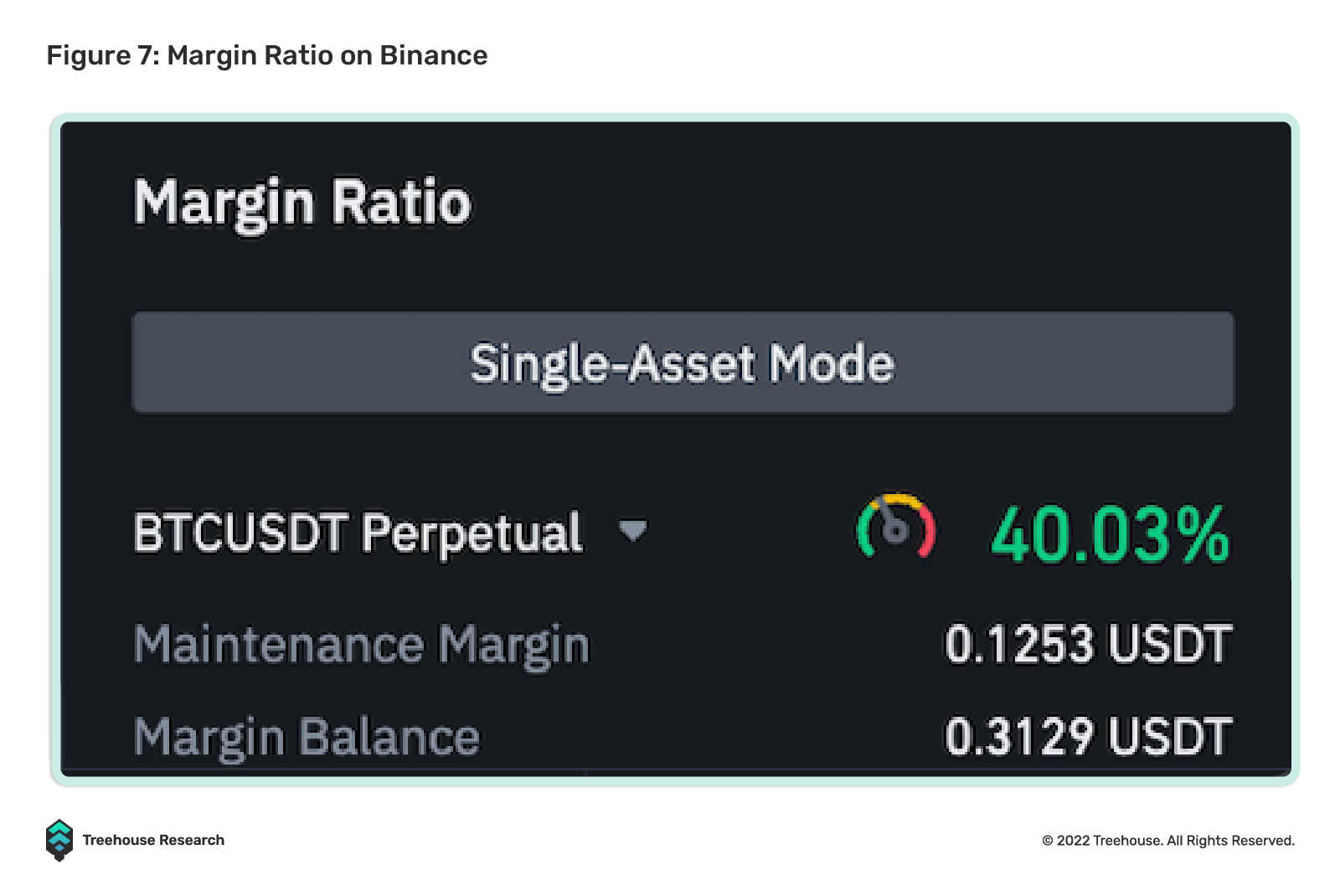

Leverage and Margin Ratio

Since leverage allows Alice to borrow and go long with more assets than she owns, the position would have a liquidation price determined by the exchange to prevent the exchange from losing money if the price goes against her position. The exchange also requires Alice to maintain a healthy ratio between the maintenance margin and the margin balance – this ratio is called the “margin ratio”. The maintenance margin is the minimum amount of margin she must hold to keep the position open, while the margin balance is the margin available after subtracting the unrealized P&L.

Liquidation

If the margin ratio is greater than or equal to 100%, which usually occurs when the liquidation price is hit, the exchange will liquidate Alice’s position and she may lose all or part of her margin depending on the specific liquidation engine. She would have to post more margin beforehand to increase her margin balance to avoid getting liquidated as price moves towards her liquidation price.

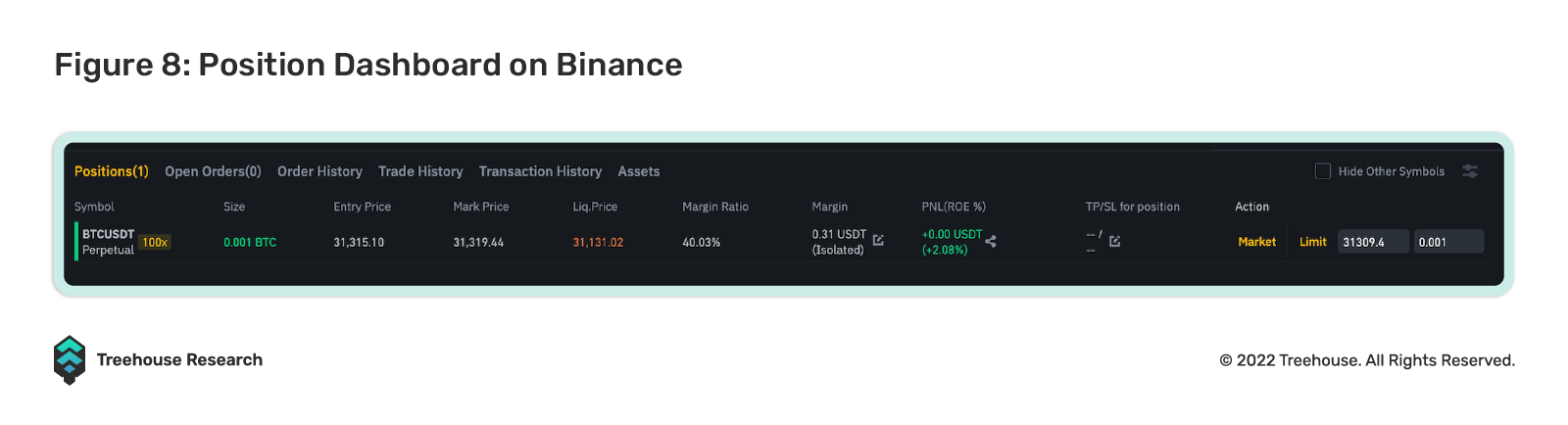

Managing a Position

Every exchange has a dashboard where users can track certain position metrics, including their liquidation price, entry price, margin ratio, and unrealized P&L. Users can also manage their positions, e.g., Close position, add/remove margin, etc. In the earlier example, if Alice’s liquidation price is close to the market price, Alice could add more margin to her position from her original collateral to move her liquidation price away from the market price, possibly avoiding liquidation. On the other hand, if her position was profitable, and she wished to close it, she could have easily done so by setting a limit/market order to sell.

AMM-Based (Peer-To-Pool)

Some decentralized exchanges, such as Perpetual Protocol, on the other hand, employ an automated market-making (AMM) mechanism for trading. The AMM model works such that the counterparty on each trade is a liquidity pool of assets. Unlike order book-based exchanges, where the price is determined by matching buy and sell orders, prices on an AMM-based exchange are determined by a pre-defined formula.

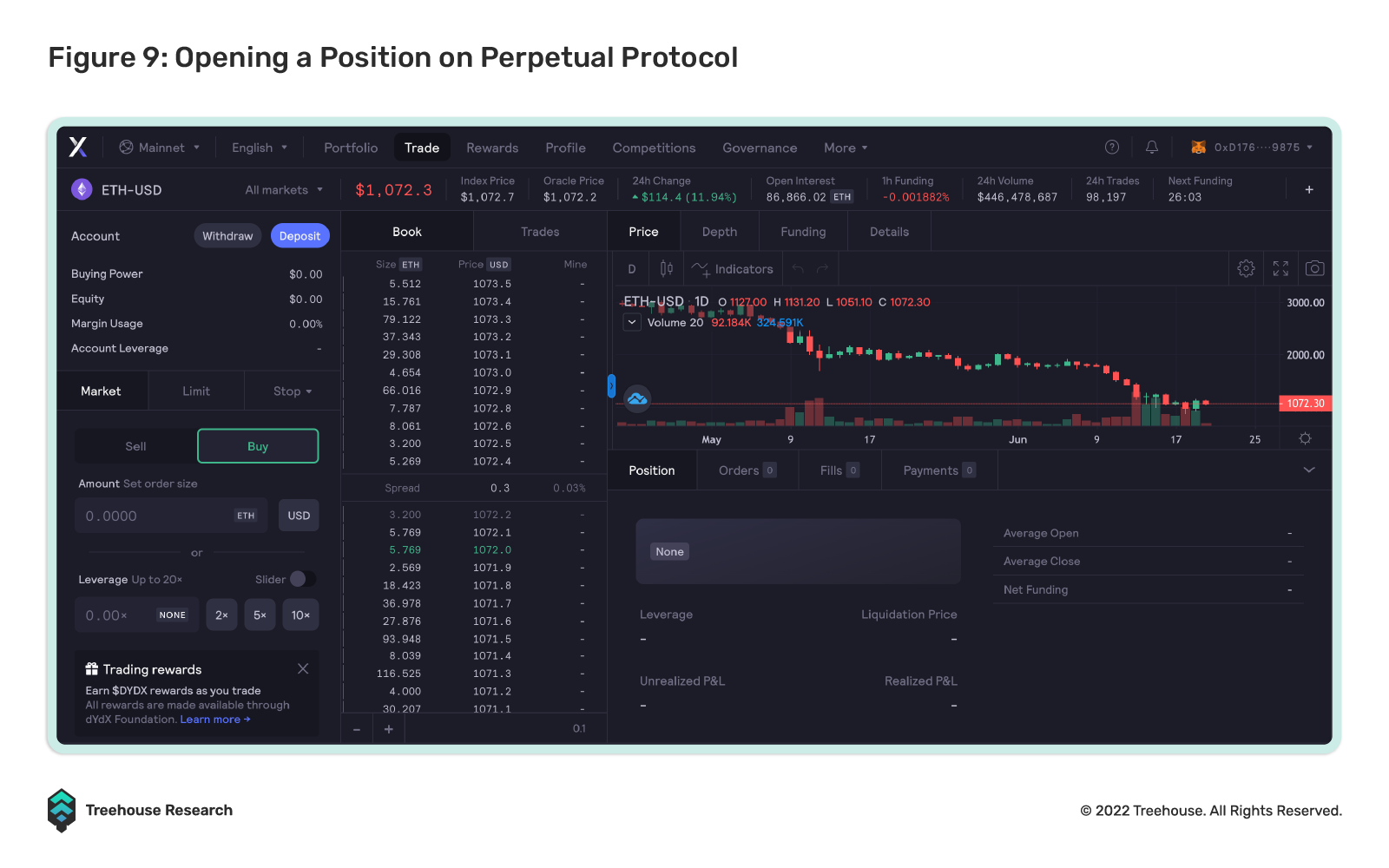

Opening a position on an AMM-based exchange

The steps to make a trade on an AMM-based exchange are slightly different because there is no order book for traders to reference and a pre-defined AMM formula determines the price. If a user thinks that the current ETH price is too high, this is how anyone can open a short position using a market order:

- Connect your on-chain wallet to the protocol

- Deposit margin in the exchange as collateral

- Choose Long/Short depending on the position you wish to open

- Choose leverage to be used and key in the position size

- Select the slippage tolerance, i.e., the spread you are willing to pay for your position

- Proceed with the trade, accept the transaction on your on-chain wallet, and pay the transaction fee accordingly

- The entry price would be determined by the predefined formula of the protocol

When it comes to managing positions, it is mostly similar to centralized order book exchanges, where a dashboard is provided to visualize the position risk metrics outlined earlier.

Conclusion

In essence, perpetual futures are non-expiring crypto-specific derivatives that allow users to indefinitely go long or short on an asset. They are widely available on many centralized and decentralized exchanges, as previously outlined, and do not cost users much to trade them. The costs mainly comprise the maker/taker’s transaction fee as well as the funding fee. When users trade perpetual futures, they incur a funding fee, which is the mechanism to bring the spot and perpetual futures prices as close to one another as possible.

Across most crypto exchanges, the perpetual futures trading volume is at least five times higher than that of spot volume. It is likely because of its deeper liquidity, convenience, and the possibility of asymmetric returns that have led to significantly higher interest in perpetual futures over spot trading. However, before users trade perpetual futures, they should be aware of its high risks.

If a user still decides to trade perpetual futures, most centralized and decentralized exchanges we have outlined provide that avenue. To choose an exchange out of the many exchanges, the user should consider the different metrics of an exchange to compare between exchanges and decide accordingly.

Despite centralized exchanges reigning supreme over the entire crypto space for the past few years, users are visibly gaining interest in decentralized exchanges that offer perpetual futures trading. One that has been gaining popularity and consistently onboarding new users despite Bitcoin’s unfavorable price action is GMX, which we will outline in another Insights piece. Stay tuned for that!